Roof Financing Options: A Texas Homeowner’s Guide

A lot of Texas homeowners find out they need a roof on the worst possible day. A hailstorm rolls through Dallas, Fort Worth, Tyler, or Longview. The next morning you see bruised shingles, granules in the gutters, a water stain on the ceiling, and suddenly you're not asking whether the roof can wait. You're asking how you're going to pay for it.

I've seen that moment plenty of times. People aren't usually confused about whether a roof matters. They're confused because the payment side gets messy fast. Insurance might cover part of it. A bank might offer one thing. A credit card company offers another. The roofer mentions financing. Everyone uses different terms, and none of that helps when rain is in the forecast.

The good news is that you usually have more roof financing options than you think. The right move depends on why the roof failed, how fast you need work done, how much equity you have, and whether you want a fixed payment, flexible access to funds, or the least paperwork possible.

Navigating the Cost of a New Roof in Texas

The roof problems that hit Texas homeowners don't wait for a convenient month. A family in Arlington gets hammered by hail and learns the shingles are compromised across multiple slopes. A homeowner in McKinney spots a leak after high wind drives rain under lifted tabs. Someone in San Antonio notices water around a vent flashing after a thunderstorm. Different homes, same feeling. Urgency, frustration, and the sinking realization that roofing work isn't cheap.

That's when people start making bad money decisions. They reach for the first offer, put too much on a high-interest card, or delay the work and hope the next storm misses them. Hope is not a payment strategy, and in Texas weather, delay usually makes the repair bill worse.

Storm damage changes the timeline

A worn-out roof gives you some room to plan. Storm damage often doesn't. If your roof has hail impact, exposed underlayment, torn ridge cap, or active leaks, the question becomes speed. You need a contractor to inspect it, document it, and tell you whether you're dealing with a repair, a partial replacement, or a full replacement.

That's also when homeowners start searching for real pricing context. If you want a better sense of what drives material, labor, and scope, this breakdown of the cost of a new roof in Texas is a useful starting point.

Practical rule: If storm damage caused the problem, don't shop financing first. Check insurance first, then fill the gap with financing only if you need to.

Most people don't need to write one giant check

You've got several ways to handle a roofing bill. Some use your home equity. Some don't. Some move fast. Some take longer but can lower the cost of borrowing. Some make sense for emergency roof replacement after hail damage. Others fit planned upgrades like impact-resistant shingles or a metal roof.

The smartest homeowners stay calm and separate the problem into two parts:

- Coverage first: Is insurance paying for storm damage?

- Funding second: If there's a gap, what's the cheapest and cleanest way to cover it?

That order matters.

Your First Step Insurance Claims for Storm Damage

If a storm caused the damage, your insurance claim is usually the first payment path to pursue. A lot of homeowners treat financing and insurance like two separate lanes. In practice, they overlap. Insurance may handle a large share of the cost, and financing may only need to cover your deductible, upgrades, or items the policy doesn't include.

Start with documentation, not guesses

Right after hail, wind, or heavy rain, document what you can safely see from the ground. Take photos of fallen shingles, dented metal, damaged gutters, interior stains, and any debris around the property. Then get a roofing contractor out for a proper inspection.

From there, the process is usually straightforward:

- Confirm the damage with a roof inspection.

- File the claim with your carrier if the damage appears storm-related.

- Meet the adjuster at the property.

- Compare the scope of insurance findings with actual roofing needs.

- Approve the work once the numbers and scope line up.

If you've never gone through it before, this guide to the storm damage insurance claim process lays out the sequence clearly.

A contractor's role matters more than people think

A storm restoration contractor doesn't replace your insurer, and shouldn't act like they do. But a good roofer absolutely helps the process go smoother. They inspect the roof thoroughly, identify collateral damage, explain what's cosmetic versus functional, and show up prepared when the adjuster visits.

That matters because storm claims can miss items if nobody is speaking up for the actual repair scope. Flashings, ridge ventilation, starter material, code-related components, and steep or multi-facet roof details can all affect the final scope of work.

A sloppy inspection creates expensive surprises later. A detailed inspection usually prevents them.

When financing still comes into play

Even with an approved claim, some homeowners still finance part of the job. Common reasons include:

- Deductible management: You may need breathing room for the out-of-pocket share.

- Upgrade choices: You might want better shingles, improved ventilation, or related gutter work.

- Timing pressure: You don't want temporary repairs dragging on while paperwork moves through the system.

Insurance is the first lever to pull after storm damage roof repair needs show up. It's often the biggest one.

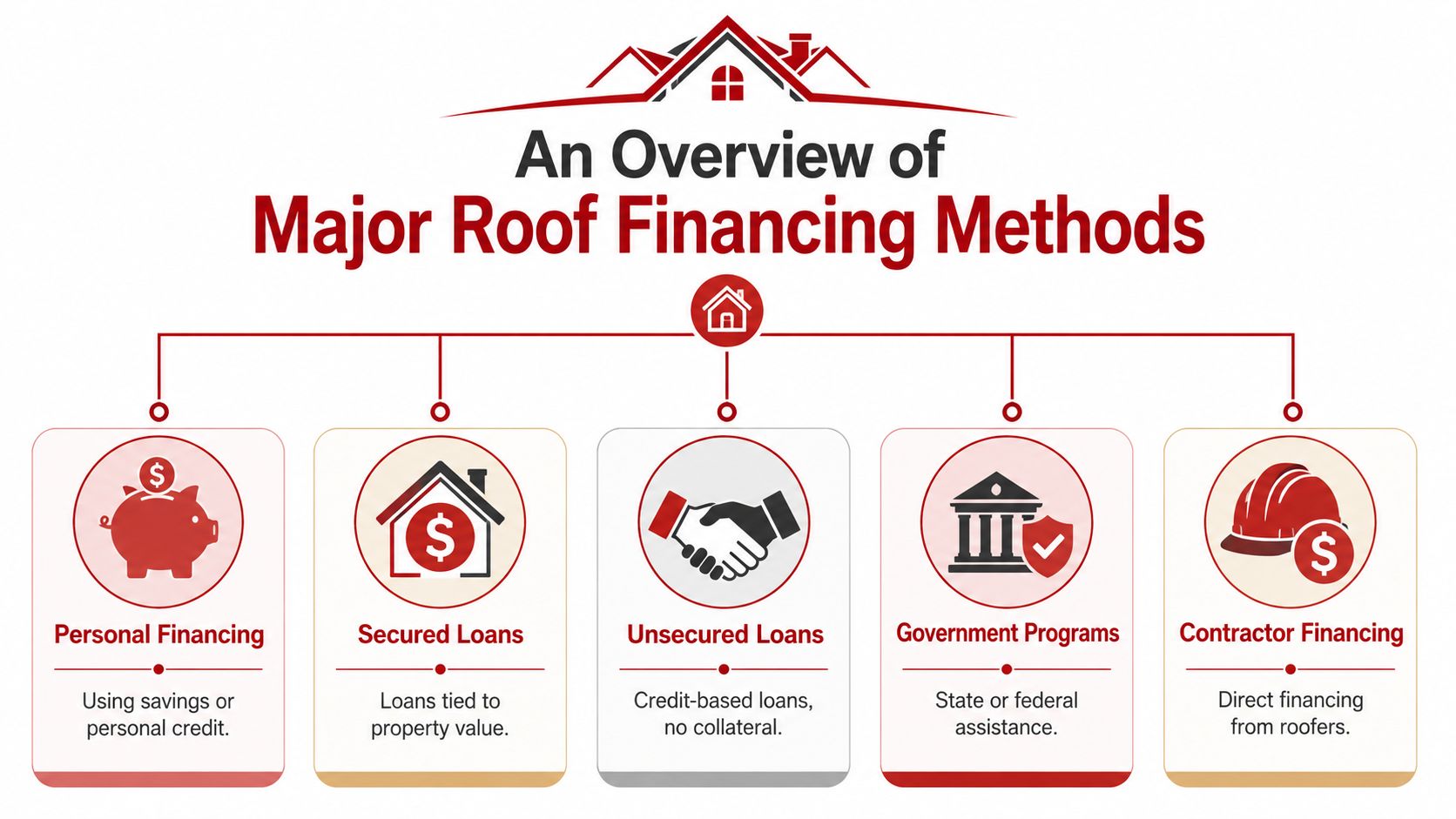

An Overview of Major Roof Financing Methods

Most roof financing options fall into a handful of buckets. Once you organize them that way, the decision gets easier.

Five buckets that cover most situations

Here's the simple map I use with homeowners in Dallas, Plano, Frisco, and beyond.

- Cash or personal savings: Cleanest option if the project is manageable and you want zero loan paperwork.

- Home equity borrowing: Usually the lowest borrowing cost if you've built enough equity and can tolerate a slower approval process.

- Unsecured personal loans: Faster than equity-based borrowing and doesn't put your house up as collateral.

- Government-backed renovation loans: Useful when the roof work is part of a purchase or bigger renovation plan.

- Contractor-arranged financing: Built for convenience, speed, and homeowners who want financing tied directly to the roofing project.

Which category fits which homeowner

Not every loan fits every roofing scenario.

A homeowner replacing an aging roof on a house with strong equity often leans toward a home equity product. Someone with active leaking after a windstorm may care more about approval speed and predictable monthly payments, which pushes personal loans or contractor financing higher on the list. A buyer closing on a home with a bad roof may get more mileage out of a renovation mortgage.

The right financing choice isn't about chasing the flashiest offer. It's about matching the money to the urgency of the roof.

That's the big mistake people make. They compare loans in the abstract. Roofing isn't abstract. A leak in Mesquite or hail damage in Garland creates a deadline.

A Detailed Comparison of Roof Financing Options

Texas homeowners usually narrow this decision fast once the actual problem is on the table. If a storm tore up the roof and rain is already finding its way in, speed matters. If the roof is old but stable, lower borrowing cost usually wins.

Here's how the main options compare in practice.

Home equity loans

A home equity loan gives you a lump sum with fixed payments. For a planned roof replacement, that structure is hard to beat. You know the payment, you know the term, and you are not guessing what the balance will look like six months from now.

Bankrate's home equity rate survey shows these loans commonly land in the mid-to-high single digits, depending on credit profile and lender terms, according to Bankrate's home equity loan rate overview.

Pros

- Fixed monthly payment

- Usually cheaper than unsecured borrowing

- Good fit for full roof replacement costs

Cons

- Your house secures the loan

- Closing can take time

- Not a great fit for urgent storm repairs

Best for

Homeowners with strong equity, steady income, and enough runway to let the bank process everything.

HELOCs

A HELOC gives you a credit line instead of one fixed lump sum. That can work well if the scope is still developing after tear-off, especially on Texas storm jobs where decking, flashing, or ventilation problems sometimes show up once the old roof comes off.

The Consumer Financial Protection Bureau explains that HELOCs usually have a draw period followed by a repayment period, and many carry variable rates that can rise over time, as outlined in the CFPB's HELOC guide.

Pros

- Flexible access to funds

- Useful if repair scope may grow

- Often lower cost than credit cards or many unsecured loans

Cons

- Rates are often variable

- Your home is collateral

- Easy to spend more than the roof requires

Best for

Owners with equity who want flexibility and can handle variable payment risk.

Unsecured personal loans

For storm-damage roofing, this is often the cleanest bank-style option. You can usually apply quickly, get a decision faster than with equity products, and keep the loan separate from the house.

Experian notes that unsecured personal loans commonly carry APRs from about 6% to 36%, with repayment terms often running two to seven years, depending on credit strength and lender standards, according to Experian's personal loan overview.

Pros

- Fast approval in many cases

- No home equity required

- Fixed payments are common

Cons

- Higher rates than many equity-backed loans

- Approval and pricing depend heavily on credit

- Some loan limits may fall short on large or premium roofing systems

Best for

Homeowners who need speed, want predictable payments, and do not want to pledge the house as collateral.

Credit cards

I rarely recommend credit cards for a full roof. They are fine for a deductible, a temporary tarp, or a small gap you can wipe out quickly. They are a bad tool for a five-figure roofing invoice.

The Federal Reserve reports that interest rates on credit card accounts assessed interest remain far above typical secured borrowing costs, as shown in the Federal Reserve's consumer credit card interest rate data.

Pros

- Immediate access to funds

- Useful for small emergency charges

- May offer short intro promotions for qualified borrowers

Cons

- High interest cost if the balance sits

- Easy to turn a roof bill into long-term revolving debt

- Poor fit for full replacement financing

Best for

Small balances only.

If you have to use a card on a roof project, keep it limited to the amount you can pay off on a clear schedule.

Government-backed renovation loans

These loans make sense in a narrower set of situations. If you are buying a house with roof problems, or bundling the roof into a larger rehab plan, they can be a smart move. If hail just punched through your shingles and water is hitting the attic, they are usually too slow.

LendingTree's renovation loan overview explains that FHA 203(k) and Fannie Mae HomeStyle loans can roll eligible roof work into broader home financing, with credit and equity requirements that vary by program.

Pros

- Can fold roof costs into long-term home financing

- Helpful for purchases and major renovation plans

- May reduce upfront cash pressure

Cons

- More paperwork and oversight

- Slower approval process

- Poor fit for urgent replacement timelines

Best for

Homebuyers, major remodels, and planned projects where the roof is one piece of a larger financing package.

Contractor-arranged financing

This option exists for a reason. Roof work after a Texas storm does not always wait on a bank. Contractor-arranged financing is built around job timing, and the better programs keep the process simple enough that you can make a decision without getting buried in paperwork.

Terms vary a lot, so read the details. Ask whether the credit pull is soft or hard, whether the loan is unsecured, whether there is a prepayment penalty, and how quickly funding lines up with the install schedule. That last point matters more than homeowners realize.

For Texas storm claims, this is often where local roofing companies separate themselves. Hail King Professionals offers an efficient financing process with a soft credit check, which makes more sense than dragging a leaking roof through a long bank approval line.

Pros

- Fast application flow

- Financing is tied directly to the roofing project

- Often easier to coordinate with emergency timelines

Cons

- Rates and terms depend on the lending partner

- Convenience does not remove the need to compare total cost

- Some offers look better upfront than they do in the fine print

Best for

Homeowners who need a quick decision, want one process from estimate to funding, and need the roof handled on a Texas storm timeline.

How to Choose The Right Financing for Your Budget

The cleanest way to choose among roof financing options is to stop thinking like a borrower and start thinking like a project manager. A roof has a timeline, a funding gap, and a risk level. Match the financing to those three things.

Start with the decision filters

Use these questions before you sign anything:

- How urgent is the work: Active leaks and storm exposure push speed higher than rate shopping.

- How much equity do you have: If you have plenty, secured borrowing may cost less.

- Do you want fixed payments or flexibility: Some people want one monthly number they can plan around. Others want room if scope changes.

- Are you financing the whole job or just the gap: That answer often decides whether a personal loan, HELOC, or contractor financing makes more sense.

- Can you handle bank-style underwriting: If not, skip options that require the most paperwork.

Sample monthly payments for a $15,000 roof

The table below uses simple payment math to show how financing structure affects monthly cost. These are illustrative examples, not lender quotes.

| Financing Option | Example APR | Term | Est. Monthly Payment | Total Interest Paid |

|---|---|---|---|---|

| Personal loan | 9% | 5 years | About $311 | About $3,657 |

| HELOC-style repayment example | 7.5% | 5 years | About $301 | About $3,034 |

| Home equity loan | 7% | 10 years | About $174 | About $5,900 |

| Credit card balance example | 20% | 3 years | About $557 | About $5,057 |

What the table actually tells you

The cheapest monthly payment isn't automatically the cheapest loan. Stretch the term long enough and you lower the payment while increasing the total interest. That's why some homeowners in Round Rock or Georgetown choose a shorter unsecured loan even when the rate is higher. They want the debt gone faster.

Others care more about monthly breathing room. For them, a longer term or an equity-backed option may fit better, especially if the roof came at a bad time.

Budget check: Pick the payment you can handle in an ordinary month, not your best month.

If the roof was insurance-related, run the numbers only on the part you need to fund. That one step keeps people from overborrowing.

Simplified Roof Financing with Hail King Professionals

A Texas storm rolls through at 2 a.m. By breakfast, you have bruised shingles, a worried spouse, and an insurance deductible to figure out. That is when financing needs to be clear, fast, and practical, not buried under bank paperwork while your roof sits exposed.

Contractor-arranged financing works well for this kind of job because it keeps the payment conversation tied to the roofing project itself. You get inspection, scope, claim coordination if storm damage is involved, and financing options in one place instead of bouncing between a roofer, a lender, and your insurance carrier.

What simpler roof financing should look like

Keep your standards high. You should be able to review payment options quickly, avoid putting your home up as collateral, and pay the balance off early without a penalty.

Hail King Professionals offers financing with a soft credit check, no home-equity requirement, monthly payment options available within minutes, and no prepayment penalties. For Texas homeowners dealing with hail damage or searching for an urgent roof replacement, that kind of process cuts delays at the exact moment speed matters most.

That does not automatically make contractor financing the lowest-cost option. It does make it one of the most practical options after a storm, especially when you need to move from inspection to approval to installation without dragging the project through a separate lending process.

Why this matters for Texas homeowners

In Texas, storm jobs do not happen on a convenient timeline. They pile up after hail, high wind, and spring storm season, and good roofers book fast. If your claim is in motion and your roof needs replacement, a simpler approval process can keep the project from stalling.

It also fits homeowners who do not want to open a HELOC just to cover a deductible, upgrades, or the portion insurance does not pay. If the roof project expands to include drainage work, it helps to look at related gutter financing options at the same time so the exterior work is planned as one job instead of split into separate surprises.

For a closer look at the company and process, here's a brief overview:

What to ask before you sign

Ask these questions plainly, and expect plain answers:

- Is the credit check soft or hard

- Are there prepayment penalties

- Is the financing unsecured

- How soon can the roof be scheduled after approval

- How is the loan handled if insurance pays part of the project later

Clear answers usually mean the financing is usable. Vague answers usually mean trouble. In my experience, that is the simplest test there is.

Common Questions About Financing Your Roof Replacement

Can I finance my insurance deductible

You may be able to finance the out-of-pocket share of a roof project through a personal loan or contractor-arranged financing, depending on the lender and the structure of the job. What you should not do is expect a contractor to “absorb” or waive a deductible. Handle it directly and cleanly.

What if the final roofing cost is higher than the original loan amount

That can happen if hidden decking issues, ventilation corrections, or code-related items show up after tear-off. The fix depends on the financing structure. Some homeowners use savings for the difference. Others add a second payment source. If your project also includes drainage work, it helps to review related gutter financing options so the full exterior scope is planned together instead of pieced together at the last minute.

Does financing change my insurance payout

Not by itself. Insurance and financing are separate. Your insurer adjusts the claim based on policy terms and documented damage. Your loan determines how you cover any remaining balance, deductible, or upgrade cost.

Are there roof financing options if my credit is less than ideal

Yes. The strongest path depends on your situation. Some contractor financing programs are more flexible than traditional banks. Government-backed renovation loans can also help in the right scenario, especially when the roof work is part of a broader mortgage-based project.

Should I use a credit card for a roof replacement

Usually no. For a small emergency repair, maybe. For a full replacement, it's usually the wrong tool. Cards are convenient, but convenience gets expensive fast when a large balance sits there month after month.

What's the smartest first move if I need roof financing now

Start with an inspection. If a storm caused the damage, check the insurance angle first. If there's still a gap, compare the total monthly cost, the speed of funding, and whether you want to keep your home out of the loan entirely.

If your roof took hail, wind, or heavy rain damage and you need a clear payment plan, contact Hail King Professionals for an inspection and a straightforward discussion about repair, replacement, insurance, and financing paths that fit your budget.