Hiring a Public Adjuster for Roof Claim A Texas Homeowner Guide

After a big Texas storm rolls through and damages your roof, the last thing you want is a frustrating, drawn-out battle with your insurance company. This is where a public adjuster for a roof claim comes in. They are licensed professionals who work only for you—the homeowner—to manage and negotiate your insurance claim from start to finish.

Essentially, they become your personal advocate, dedicated to making sure you get the maximum settlement you're entitled to for all the damage your property sustained.

Your Ally in Navigating Complex Roof Claims

Let's say your home just got hammered by hail. You file a claim, and your insurance carrier sends out their own adjuster. It’s critical to understand that this person works for the insurance company. Their job is to protect the company's bottom line, which often means minimizing what they pay out on your claim.

A public adjuster completely flips that dynamic. They are on your side, not the insurance corporation's. Their mission is to level the playing field by:

- Performing a deep-dive inspection to document all storm damage, catching things the insurer's adjuster might have missed or ignored.

- Digging into the fine print of your insurance policy to make sure you get every benefit you've been paying for.

- Building a powerful, evidence-backed claim that clearly justifies a fair and complete settlement.

- Taking over the negotiation process and handling all the back-and-forth with the insurance company for you.

Why This Matters in Texas

This kind of expert advocacy is more important than ever for homeowners in storm-prone areas like Dallas-Fort Worth. The damage from severe weather here has exploded. Convective storm damage—that's hail and high winds—shot up from $30 billion in 2022 to an incredible $60 billion in 2023. Texas consistently leads the nation in these expensive claims.

With so much money on the line, insurance companies are tightening their belts. It’s become common for them to offer lowball initial settlements that won’t even come close to covering the cost of quality materials and skilled labor, leaving you to foot the rest of the bill. To get a better handle on this, it's helpful to understand the wider world of navigating home insurance claims.

A public adjuster makes sure your claim is handled correctly from the very beginning. They fight to get you the money needed for proper, code-compliant repairs—not just a cheap patch job.

At the end of the day, hiring a public adjuster is an investment in your home's future and your own peace of mind. They bring a level of expertise and negotiating power most homeowners just don’t have, turning a stressful fight into a professionally managed process aimed at getting you the best possible outcome.

Understanding Who Is on Your Side

After you file a roof damage claim, you’ll suddenly have a lot of people showing up, and many of them will have "adjuster" in their title. This is where most homeowners get tripped up. It's easy to assume everyone is there to help you, but that’s rarely the case.

Knowing who works for whom is the single most important part of getting a fair settlement. The adjuster your insurance company sends out works for them, not you. Their job is to protect the company's bottom line. Think of them as the opposing team's coach—their goal is to limit the score, which in this case, is your payout.

The Key Players and Their Loyalties

The claims process can feel like a confusing game with players you've never met. It's crucial to know who's on your team and who's playing for the other side. Your roofer is your expert for the actual repairs, but the adjuster your insurance company sends has an entirely different agenda.

A public adjuster is the only type of adjuster licensed by the state to work exclusively for you, the policyholder. They are your dedicated advocate, with a legal and ethical obligation to protect your interests, not the insurance company’s.

Their entire job is to dig deep into your policy, meticulously document every bit of damage, and negotiate relentlessly on your behalf to get you the maximum settlement you're entitled to. This is precisely why hiring a public adjuster for a roof claim can be such a game-changer.

Who's Who in Your Roof Claim Key Player Comparison

To make it crystal clear, let's break down the different roles you'll encounter. The differences in who they work for and what they're trying to achieve are night and day.

| Key Player | Who They Work For | Primary Goal | Licensed to Negotiate Claim? |

|---|---|---|---|

| Insurance Adjuster | The Insurance Company | Minimize the claim payout to save the company money. | Yes |

| Roofing Contractor | You (for repairs) | Assess damage and provide an estimate for repairs. | No |

| Public Adjuster | You (the policyholder) | Maximize your settlement to ensure full and fair coverage. | Yes |

As you can see, your roofer is an essential partner for getting the work done right, but they can't legally step in and negotiate your claim settlement. A public adjuster is the missing piece of the puzzle, serving as your professional representative in every conversation and negotiation with your insurer.

This kind of expert advocacy is valuable across all types of property damage. For example, the complexities of navigating fire insurance claims show just how critical specialized knowledge is. A public adjuster brings that same level of focused expertise to your roof claim, ensuring nothing gets overlooked.

When to Hire a Public Adjuster for a Roof Claim

Let's be practical. You don't need to call in a professional for every minor roof leak. But knowing the right time to hire a public adjuster for a roof claim can be the single most important decision you make, turning a potential disaster into a financial recovery.

Certain situations should be immediate red flags, signaling it’s time to get a professional advocate in your corner. Think of it this way: you wouldn't represent yourself in a complex legal case, so why go head-to-head with a massive insurance corporation alone when thousands of dollars are on the line? Hiring a public adjuster is a strategic move for when the odds feel stacked against you.

Key Triggers That Signal You Need an Expert

So, what are the big warning signs? If you run into any of these common scenarios, it's a strong sign you should at least have a conversation with a public adjuster. We see these tactics all the time, especially after major storms hit the Dallas-Fort Worth area.

Your claim is a great candidate for a public adjuster if:

- The Insurance Company Denies Your Claim: A flat-out denial is rarely the end of the story. It's often just the insurance company's opening move. A public adjuster knows exactly how to reopen denied claims and counter with compelling evidence.

- The Settlement Offer Is Too Low: If the insurer's offer is nowhere near your contractor's estimate for a quality repair, you're being lowballed. A public adjuster’s job is to step in and negotiate a payout that actually covers the full cost of the damage.

- The Damage Is Blamed on Pre-Existing Issues: This is a classic. Insurers love to claim that storm damage is just "wear and tear" or the result of "poor maintenance." An adjuster can bring in engineering reports and meteorological data to prove the damage is new and a direct result of the storm.

- The Claim Is Large or Complex: Has your home suffered widespread damage? We're talking a full roof replacement plus gutters, siding, windows, and even interior water damage. A public adjuster manages these complex claims to make sure nothing gets overlooked.

The Financial Argument for Hiring a Public Adjuster

It's completely normal to think about the cost. But instead of viewing an adjuster's fee as an expense, think of it as an investment in a much, much bigger payout. Their fee is simply a percentage of the settlement, so their goal is your goal: get the maximum amount possible. The financial upside can be staggering.

A landmark study revealed that policyholders who hired public adjusters for catastrophic claims (like major hail damage) received settlements that were an incredible 747% higher than those who handled the claim themselves. Even for everyday, non-catastrophic claims, settlements were 574% higher.

These numbers don't lie. They show the real-world financial power a skilled expert brings to the table. When you’re facing a complicated or disputed claim, you're not just paying for an expert's time—you're paying for results.

It's also a good idea to get a handle on the entire claims timeline. You might find our guide on the storm damage insurance claim process helpful for a bird's-eye view.

Your Step-by-Step Guide to Working with a Public Adjuster

So, you’ve decided to bring an expert onto your team. You might be wondering, "Now what?" Hiring a public adjuster kicks off a clear process designed to lift the weight of a complex insurance claim right off your shoulders.

Think of it this way: if you were facing a tax audit, you’d want a CPA in your corner. A public adjuster is that same kind of advocate for your insurance claim. From the moment you sign the agreement, they take the reins, managing every detail with one goal in mind: getting you the full settlement you're entitled to.

Here’s a look at what you can expect when you partner with a public adjuster.

Step 1: Vetting and Hiring Your Advocate

Before you sign any contract, you need to do your homework. This isn't the time for a quick Google search; treat it like hiring any other key professional for a critical job. The first consultation is your chance to ask direct questions and get a real feel for their experience, especially with roof claims like yours.

A reputable public adjuster will be an open book. Be ready with these questions:

- Are you licensed in Texas? Don’t just take their word for it—ask for their license number.

- What’s your experience with hail and storm damage in the Dallas-Fort Worth area? Local knowledge is a massive plus.

- Can you share references from past clients who had similar roof claims?

- How exactly do your fees work? It should always be a contingency fee, meaning they only get paid if you do, and the percentage should be crystal clear.

Step 2: Inspection and Policy Deep Dive

Once they're on board, your public adjuster’s first job is to perform their own incredibly thorough inspection. This goes far beyond the quick walk-around the insurance company’s adjuster might do. They'll be documenting every single damaged shingle, dented gutter, and cracked window, using specialized tools to build a mountain of evidence.

At the same time, they’ll be digging deep into your insurance policy. They read every line, looking for specific clauses, endorsements, and coverage extensions that apply to your situation. This two-part approach ensures the claim they build is backed by both physical proof and the legal language of your contract. This is why getting a professional roof inspection is such a valuable starting point—it provides a strong foundation of evidence.

Your public adjuster’s mission is to build an ironclad case. They combine meticulous damage documentation with a mastery of policy language to leave no room for the insurer to unfairly deny or underpay your claim.

Step 3: Building and Submitting the Claim

With all the evidence in hand, your advocate gets to work constructing a complete claim package. This is much more than a simple form. It’s a detailed, professional portfolio proving the full extent of your loss.

This package will often include:

- High-resolution photos and drone footage showing the damage from every angle.

- Itemized repair estimates from trusted, local contractors.

- Expert reports, like meteorological data proving a hailstorm's severity.

- A formal "Proof of Loss" document that clearly states the total financial value of your claim.

This professionally prepared claim is then officially submitted to the insurance company. It immediately sets a new, authoritative tone for the entire process.

Step 4: The Negotiation Process

This is where your public adjuster truly shows their value. It’s almost a guarantee that the insurance company will come back with a lower offer. Your adjuster handles every phone call and email, methodically pushing back against lowball numbers with hard facts, photographic evidence, and direct policy quotes.

This negotiation can be a long, technical back-and-forth, but you won't have to deal with any of it. Your adjuster manages the entire conversation, keeping you in the loop on their progress. Their skill in negotiation is what closes the gap between the insurance company’s first offer and the fair settlement you actually deserve. And in the end, you always have the final say on accepting an offer.

Decoding Public Adjuster Fees and Contracts

When you're thinking about hiring a public adjuster for a roof claim, one of the first questions is always about the cost. It’s a fair question, and thankfully, the answer is straightforward and designed to protect you as the homeowner.

Public adjusters work on a contingency fee. This simply means they only get paid if they successfully recover money for you. There are no upfront charges or hourly bills to worry about, which takes the financial risk completely off your plate. Their success is tied directly to yours.

The fee is a set percentage of the final insurance settlement they secure on your behalf. While fees can sometimes be as high as 10% to 20% in other states, Texas law has a consumer-friendly cap. For most property claims, a public adjuster’s fee is legally capped at 10% of the settlement.

Reading the Fine Print of Your Contract

Before you commit to anything, it’s absolutely vital to sit down and read the contract. A professional, trustworthy adjuster will walk you through an agreement that’s clear and easy to follow. Don't ever hesitate to ask them to clarify every single point until you're 100% comfortable.

Your contract is your roadmap for the entire process. Make sure it clearly spells out these key details:

- The Exact Fee Percentage: This should be stated plainly, and in Texas, it shouldn't go over that 10% cap.

- Scope of Services: The agreement needs to outline exactly what the adjuster will be doing for you—inspecting the property, documenting all the damage, handling the claim paperwork, and negotiating directly with your insurance carrier.

- Cancellation Policy: You need to know the rules for ending the agreement. Texas law provides a specific window of time for you to cancel the contract without any penalty.

- Payment Terms: The contract should explain how the adjuster's fee gets paid out of the final settlement. Typically, the insurance company will make the check payable to both you and the public adjuster to ensure everything is handled properly.

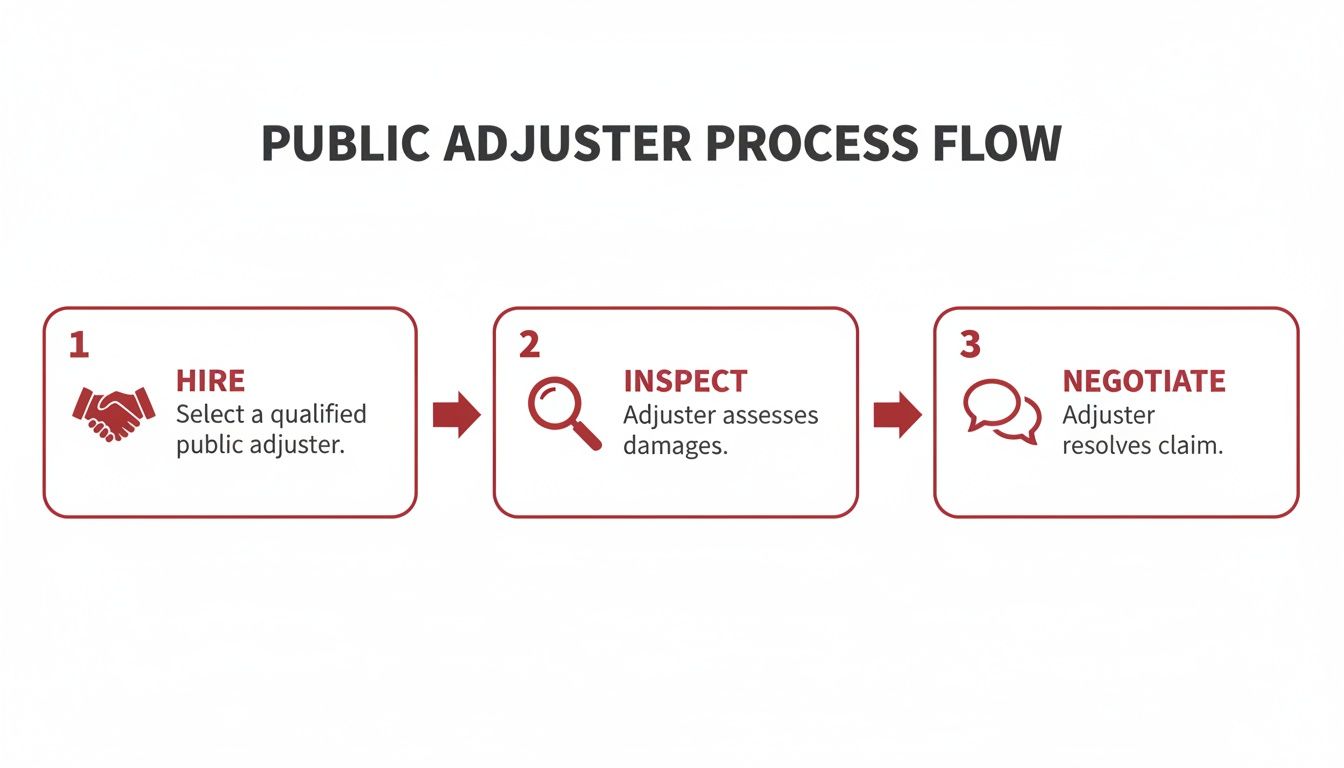

This infographic breaks down the simple, three-step journey you'll take with your adjuster after hiring them.

This process ensures a professional manages your claim from the initial inspection all the way to the final negotiation, lifting a huge weight off your shoulders. If you end up with a large settlement, you might also need to think about how you'll pay for the work. For more on managing those costs, check out our guide on how to finance a new roof.

By understanding the fee structure and carefully reviewing your contract, you can step into this partnership with total confidence.

Common Questions About Public Adjusters for Roof Claims

It's completely normal to have questions even after you get the basics of what a public adjuster does. When your home and finances are on the line, you should be thorough. Dealing with an insurance claim can feel like trying to navigate a foreign country without a map, but getting clear answers will give you the confidence you need.

Let’s walk through some of the most common questions we hear from homeowners about hiring a public adjuster for a roof claim.

Can I Hire a Public Adjuster After My Claim Was Denied?

Yes, absolutely. In fact, a denied claim is one of the most common reasons homeowners call a public adjuster in the first place. Think of that denial letter not as the final word, but as the insurance company's opening offer.

A good public adjuster knows exactly how to challenge these denials. They’ll reopen the claim, bring a fresh set of expert eyes to inspect the damage, and build a brand-new case file packed with compelling evidence. Their job is to systematically dismantle the insurer's reason for the denial and force them back to the negotiating table.

Will My Insurance Company Penalize Me for Hiring an Advocate?

No. This is a common worry, but you can put it to rest. It is illegal for an insurance company to penalize you for hiring professional representation. Your insurer can't hike your rates, threaten to cancel your policy, or refuse to communicate just because you brought in a licensed expert to advocate for you.

Public adjusters are licensed and regulated by the state's department of insurance. They are a recognized and legitimate part of the claims industry. Using one is a standard business practice for resolving disputes and ensuring policyholders are treated fairly.

It's no different than hiring a CPA to help with a complicated tax audit. You're simply bringing in a specialist to make sure your interests are protected and everything is handled by the book.

Why Not Just Let My Roofer Handle the Claim?

While your roofer is the expert you need for assessing damage and doing the repair work, they are legally prohibited from negotiating insurance claims in Texas. This is a critical distinction that many people miss. Only a licensed public adjuster or an attorney can legally negotiate a claim settlement on your behalf.

It helps to think of their roles this way:

- A Roofer's Job: To diagnose the physical damage, write a detailed scope of work for the repairs, and then restore your roof with quality craftsmanship.

- A Public Adjuster's Job: To interpret your dense insurance policy, document all the damage in a language the insurer understands, and negotiate to get you the full settlement you’re entitled to so you can afford those repairs.

A truly professional roofer understands and respects this boundary. They focus on what they do best—building—and allow the public adjuster to do what they do best: fighting for the money to get the job done right.

How Long Does the Process Take with a Public Adjuster?

The timeline really depends on the specifics of your claim. A few key things can affect how long it takes: the complexity of the damage, the total value of the claim, and, frankly, how cooperative your insurance company decides to be.

A relatively straightforward claim might get settled in a few weeks. However, a major dispute over a full denial on a high-value roof could easily take several months. The real advantage here is that your public adjuster manages that entire, often frustrating, process. They handle every phone call, email, and piece of paperwork, constantly pushing the claim forward so you don't have to.

Their goal isn't just a fast settlement, but a fair one. While it might take a bit longer, their expertise ensures you aren’t leaving thousands of dollars on the table just for the sake of closing the claim quickly.

If you're facing a challenging roof claim and believe you need an advocate on your side, the first step is a professional damage assessment. The team at Hail King Professionals provides free, comprehensive roof inspections across Dallas-Fort Worth to give you a clear, honest picture of your situation. Contact us today to ensure you have the evidence you need to secure a fair outcome. https://hailkingpros.com