Unpacking Insurance Claim Denial Reasons for Your Roof

Getting a denial letter for your roof claim can feel like a slap in the face. It feels final, but trust me, it’s often just the insurance company's opening move in a long negotiation. The most common insurance claim denial reasons I see are things like not enough proof of damage, blaming it on old "wear and tear," or pointing to some fine print in your policy.

Your first job is to figure out exactly why they said no. That’s your key to unlocking a successful appeal.

Why Was My Roof Claim Denied

So, you got the letter. It’s easy to feel defeated, but don't let that initial shock paralyze you. Think of this as the start of a new conversation, not the end of one. The insurance company has laid out its argument for the denial, and now it’s your turn to understand their angle and build a solid counter-argument.

We're going to walk through the most common reasons these claims get rejected. The goal is to help you see what that denial letter really means so you can start building a winning strategy.

Translating Your Denial Letter

That denial letter is packed with industry jargon and carefully chosen phrases. It's designed to be confusing. But each one of those reasons points directly to the kind of evidence you need to gather to fight back effectively.

Here's a quick reference table to help you decode what they're actually saying and what you'll need to prove them wrong.

| Denial Reason | What It Really Means | Key Evidence Needed |

|---|---|---|

| Wear and Tear / Age | "Your roof was old and failing before the storm, so we aren't paying to replace it." | Date-stamped photos showing the roof's condition before the storm, maintenance records, and a professional inspection report that isolates new storm damage from old wear. |

| Improper Installation | "The roof wasn't installed to code or manufacturer specs, which caused the failure, not the storm." | The original installation contract, photos of the damage showing specific installation flaws are not the cause, and an inspection report from a certified roofer confirming the storm is the primary cause. |

| Cosmetic Exclusions | "The hail only caused dents and dings, which don't affect the roof's function, so we won't pay." | A detailed report from a roofing expert explaining how the "cosmetic" damage has compromised the shingle's integrity and shortened the roof's lifespan, alongside manufacturer data sheets. |

| Insufficient Proof | "You haven't proven that a covered event (like this specific hailstorm) caused this specific damage." | Local weather data for the storm date, "before" and "after" photos of the roof, and a detailed, itemized report from a qualified contractor linking the damage directly to the storm event. |

Seeing it laid out like this makes it clearer, right? Your insurer is making a specific claim about your roof's history or the damage itself. Your job, with the help of a pro, is to dismantle their argument with hard evidence.

The Role of Missing or Inaccurate Data

Sometimes, a denial has nothing to do with your roof and everything to do with a simple data error. Many insurers use automated claims processing systems that can instantly flag a claim for tiny inconsistencies or a single missing document. A small typo can trigger an automatic rejection before a human ever lays eyes on it.

This isn't just a homeowner problem. In the healthcare world, a massive 41% of providers see denial rates of 10% or higher, and a full 50% of those denials come down to missing or wrong information. The frustration is the same whether it’s a medical bill or a roof claim after a hailstorm.

The takeaway is clear: getting your documentation perfectly organized from the very beginning is one of the most important things you can do.

The Missing Proof Problem

When an insurance company denies a roof claim, there's one reason I see more than any other, and it’s a tough one to overcome: not enough proof. Your insurer won’t just take your word that a storm rolled through and wrecked your shingles. They need hard, undeniable evidence that a specific, covered event—like that hailstorm last Tuesday—is the direct cause of the damage you're reporting.

Think of yourself as the lead prosecutor in a court case. The insurance adjuster is the jury, and your job is to present a case so solid that there’s no other possible conclusion. A few blurry photos and a vague description of "storm damage" just won't cut it. That's an easy case for them to dismiss.

What you need is an airtight file of evidence that leaves no room for doubt. This is how you transform a simple request for payment into a fact-based demand for the coverage you've been paying for all along.

Building Your Evidence File

So, what does this kind of bulletproof evidence actually consist of? It's all about gathering different documents and data points that, when woven together, paint a clear and convincing picture of what happened. You’re essentially creating a timeline that connects the "before" (your healthy roof) and the "after" (the damage) with a specific weather event.

I know this sounds like a lot, but if you break it down into a simple checklist, it's completely manageable. Every piece of evidence you collect strengthens your position and helps you preemptively counter any reason the insurer might use to deny your claim. For a detailed look at what a professional inspector documents, our roof inspection checklist template is a great resource.

Here’s the essential evidence you absolutely need to gather:

- Date-Stamped "Before" Photos: If you happen to have any pictures of your roof from before the storm, they are pure gold. These photos establish a baseline condition, making it extremely difficult for an insurer to argue the damage was already there.

- Comprehensive "After" Photos: As soon as it's safe, get outside and take plenty of clear, high-resolution pictures of the damage. You need shots from multiple angles and distances—get close-ups of hail impacts or wind-lifted shingles, but also take wider shots to show the overall pattern of damage.

- A Professional Inspection Report: This is the cornerstone of a strong claim. A detailed report from a reputable roofing contractor validates the extent of the damage, professionally links it to the storm, and serves as a credible third-party assessment.

- Local Weather Data: Don't forget to track down meteorological reports for your exact address on the date of the storm. This data confirms the storm's severity—including things like hail size and wind speeds—and provides objective proof that a covered event actually took place.

Why Documentation Is Non-Negotiable

In the world of insurance, meticulous documentation is your best and only defense. This has become even more critical as carriers tighten their review processes. Payer audits are on the rise, and while appeals can successfully overturn over 54% of denied claims, getting that initial approval is tougher than ever.

At the same time, the property and casualty sector is battling around $45 billion in annual fraud, which has led to intense scrutiny of any storm claim that lacks solid proof of "sudden and accidental" damage.

Your insurance policy is a contract, and that contract requires you to prove your loss. If you don't provide sufficient evidence, you haven't held up your end of the deal, giving the insurer a perfectly valid reason to deny your claim.

Ultimately, presenting a well-documented claim file shows the adjuster you're serious and have done your homework. It signals that you are prepared to advocate for yourself, which dramatically increases your odds of getting a fair and timely approval.

Navigating Policy Exclusions and Loopholes

Think of your insurance policy as the rulebook for a game you didn't know you were playing. When you file a claim, your insurance company doesn't just glance at the rules—they study them with a magnifying glass, looking for any clause that lets them sit this round out. This is where so many homeowners get tripped up, and it's one of the most maddening insurance claim denial reasons out there.

An adjuster’s decision often hinges on specific, carefully chosen words buried deep in your policy documents. These aren't just suggestions; they are legally binding definitions that can make or break your claim. Getting familiar with this language before you have a problem is your single best defense.

The Most Common Policy-Based Denials

When an adjuster walks your roof, they're not just looking for damage. They're on a mission to classify the type of damage and pinpoint its cause. Their real job is to see if what they find on your roof matches what your policy actually covers.

Unfortunately, some of the most common reasons for denial are built right into the contract you signed.

- Normal Wear and Tear: Insurers will argue that a roof has a limited lifespan and naturally deteriorates. If they can successfully claim your roof failed simply because it was old and brittle—not because a specific storm event pushed it over the edge—they’ll deny the claim. This is a go-to move, especially for roofs over 10-15 years old.

- Improper Maintenance: Have you had your roof inspected in the last few years? Are your gutters clogged with leaves? If you can't show that you've been taking care of your roof, the insurance company has an easy out. They can argue that your neglect, not the storm, is the real cause of the problem.

- Cosmetic vs. Functional Damage: After a hailstorm, this is the big one. Your insurer might send an adjuster who agrees that hail pelted your roof. But then comes the catch: they'll claim the dents and dings are merely "cosmetic" and don't actually compromise the roof's ability to keep water out. Many modern policies have clauses that specifically exclude this kind of damage.

It's easy to see how an insurer can stack these against you. Imagine you're a Texas homeowner with a 15-year-old roof after a big hailstorm. The denial letter might state the hail only caused cosmetic damage to a roof that was already compromised by age and wear. Just like that, your claim is closed.

ACV vs. RCV: A Critical Distinction

This next part is crucial, and it’s a loophole that can cost you thousands. You have to understand the difference between Actual Cash Value (ACV) and Replacement Cost Value (RCV) coverage.

Actual Cash Value (ACV) is the one you don't want. It pays you for the depreciated value of your roof. If you have a 20-year roof that's 10 years old, they'll only pay you for the 10 years of life it had left. You're stuck covering the rest of the replacement cost yourself.

Replacement Cost Value (RCV) is what you hope you have. This coverage pays the full cost to replace your roof with brand-new, similar materials, minus your deductible. It’s designed to make you whole again.

Countless homeowners go years thinking they have full coverage, only to discover an ACV provision when they get their first check. It's one of the most painful insurance claim denial reasons because it turns an "approved" claim into a massive out-of-pocket expense. Dig out your policy today and find out which one you have.

Your Guide to Appealing a Denied Roof Claim

Getting that denial letter for your roof claim can feel like hitting a brick wall. But here's something most homeowners don't realize: an insurer's initial "no" is often just the opening move in a negotiation, not the final word.

Don't let the frustration get the best of you. The trick is to channel that energy into building a professional, evidence-backed appeal. You'd be surprised how often a solid challenge works, mainly because many first-round denials are based on a quick look, incomplete information, or just one adjuster's opinion.

First Steps in the Appeal Process

Before you fire off an angry email, your first step is to find out exactly why they denied the claim. Don't guess. You need to formally request a detailed explanation for the denial in writing, which your insurance company is required by law to provide.

Once you have that letter in hand, don't try to decipher the jargon alone. The language can be dense and confusing by design. Your next call should be to an expert—like a storm damage roofing contractor you trust—to go over the denial letter and your full policy. They live and breathe this stuff and can translate the insurance-speak into a clear action plan.

This deep dive is what sets the foundation for your entire appeal. It shows you exactly which arguments the insurer is using so you know what evidence you need to find to tear them down.

Gathering Targeted Evidence for Your Appeal

This is where you shift gears from reacting to taking control. Your mission is to gather fresh, compelling proof that directly contradicts the insurance claim denial reasons they gave you. If they said it was just "wear and tear," you need a report from an independent expert proving the damage came from a specific storm. If they pointed to a policy exclusion, you need to show why it doesn't apply to your situation.

Here's what that looks like in practice:

- Get a Second Opinion: Have a different, highly respected roofing contractor perform a new inspection. Their report needs to be a point-by-point rebuttal of the insurance adjuster's findings.

- Use the Manufacturer's Own Words: Find the technical data sheets for your specific shingles. These documents can prove that what the insurer calls "cosmetic" hail damage actually voids the shingle's warranty or compromises its ability to protect your home.

- Look Next Door: Did your neighbors with the same insurance carrier get their roofs approved for damage from the same storm? Document it with photos and addresses. This kind of evidence highlights an inconsistency that is very hard for an insurer to ignore.

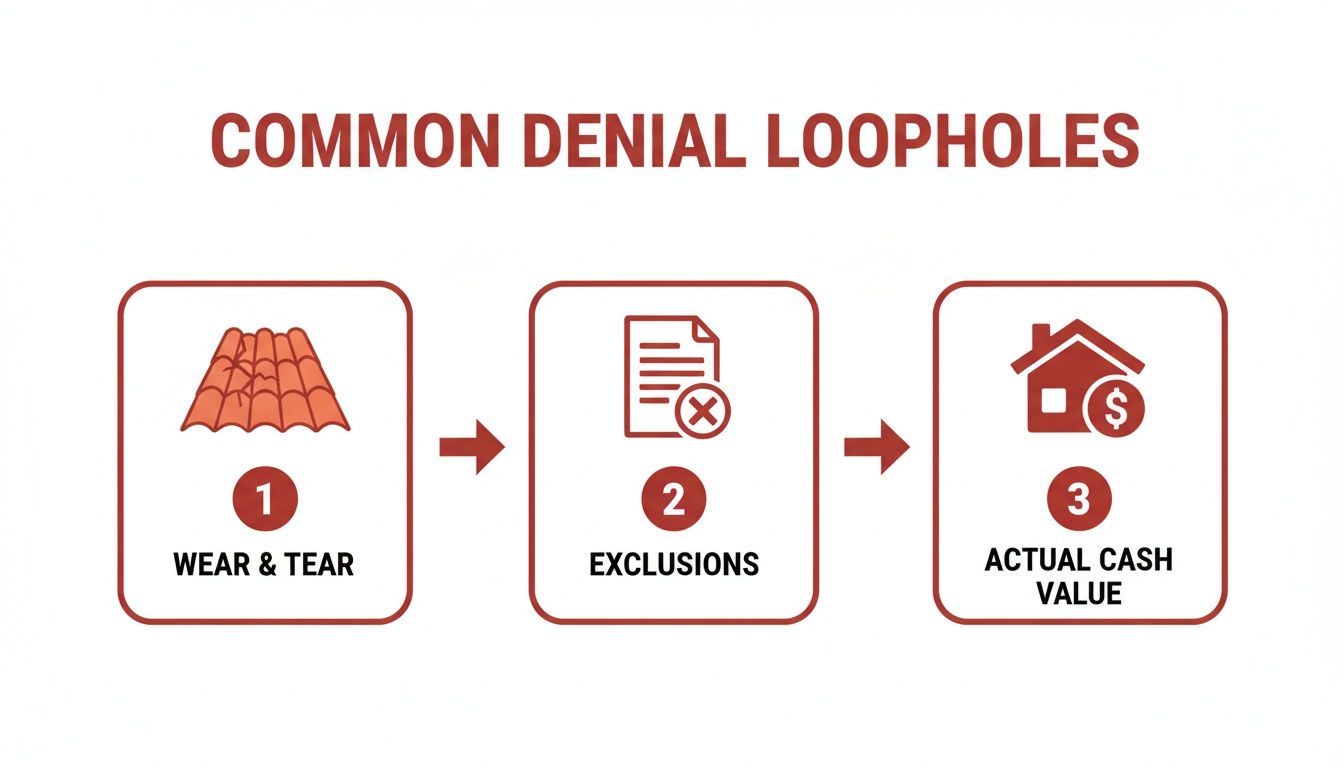

This infographic breaks down some of the most common justifications insurers use to deny a claim.

These three arguments—wear and tear, policy exclusions, and disagreements over value—are at the heart of most fights over property claims.

Drafting a Powerful Appeal Letter

With your new evidence organized, it's time to write your appeal letter. Keep your tone professional and stick to the facts; this isn't the place for emotion. You'll want to methodically present your case, referencing each piece of new evidence you've gathered.

Think of it this way: in the healthcare world, the average denial rate for ACA marketplace claims is a staggering 19%. But when patients appeal, an incredible 44% of those denials are overturned. The lesson here is that initial denials are often weak. For homeowners in places like Dallas-Fort Worth, fighting back is essential to avoiding a five-figure bill for a new roof.

A Simple Framework for Your Appeal Letter:

- The Basics: Start with your name, policy number, claim number, and the date the damage occurred. State clearly, "I am writing to formally appeal the denial of my claim."

- The Disagreement: Briefly mention the reason your insurer gave for the denial and state that you disagree with their assessment.

- The Proof: Lay out your counter-arguments one by one. Attach and refer to your new evidence (e.g., "As documented in the attached inspection report from [Contractor's Name]…").

- The Request: Be direct about what you expect. For example, "I am requesting full payment for the replacement of my roof, as detailed in the contractor's estimate provided."

- The Closing: End professionally, stating that you look forward to their prompt reconsideration of the claim.

When to Escalate Your Claim

If the insurance company still says no after your internal appeal, the fight isn't over. Your next step is to take it up a level. You can file a formal complaint with your state's Department of Insurance, which will trigger an official review of your case. Another smart move is to bring in an expert who works only for you. You can find out more about when it makes sense to https://hailkingpros.com/2026/03/08/public-adjuster-for-roof-claim/ in our detailed guide.

And if all else fails, it might be time to talk to a lawyer. When a roof claim appeal hits a dead end, understanding your legal recourse options for denied claims is a critical final step to getting what you're owed.

How a Roofing Pro Can Win Your Claim

Trying to fight your insurance company alone after a storm is a classic David-and-Goliath story, but without the guaranteed happy ending. It's just not a fair fight. They have teams of adjusters, legal experts, and underwriters who do this every single day. You? You just want your roof fixed so you can get back to normal.

This is exactly where a seasoned roofing contractor earns their stripes. A real pro does a lot more than just swing a hammer—they become your advocate, your technical expert, and your strategic guide through the claims maze. They are the equalizer, bringing the specific knowledge needed to push back against the most common insurance claim denial reasons.

Your contractor’s job is to take the damage on your roof and translate it into the precise language and hard evidence that insurance companies are required to act on. Without that expert translation, you’re starting out at a serious disadvantage.

The Power of an Expert Inspection

Here’s a piece of advice we give everyone: the moment you think you have storm damage, your first call shouldn't be to your insurance company. Call a local, reputable roofer and ask for a pre-claim inspection. This one move can completely change the game.

Think about it. The insurance adjuster is paid by the insurance company, and their primary job is to protect their employer's bottom line. A good roofer, on the other hand, works for you. Their focus is on finding every bit of legitimate damage and making sure your home is properly restored.

A professional contractor’s inspection is your first and best piece of leverage. It sets the factual foundation for your claim before the insurer has a chance to frame the narrative with their own assessment.

This initial inspection report acts as your baseline of truth. It's a detailed, photo-documented account of the damage that you can hold up against the insurance adjuster's findings. It's the single best tool for shutting down an adjuster’s attempt to blame everything on “pre-existing conditions” or "wear and tear." If you're not sure how to find a trustworthy partner, our guide on how to choose a roofing contractor is a great place to start.

Speaking the Language of Code and Materials

An experienced contractor doesn't just see a damaged shingle; they understand the physics and material science behind the failure. That deep knowledge of building codes, manufacturer installation specs, and how materials perform under stress is an incredibly powerful asset for your claim.

For example, an adjuster might wave their hand at hail impacts and call them “cosmetic.” A knowledgeable roofer will immediately counter that argument. They can pull up the shingle manufacturer's own technical sheet showing that those "cosmetic" hits have actually compromised the granule layer, which voids the warranty and drastically shortens the roof’s lifespan. Suddenly, a subjective opinion becomes an undeniable technical fact.

A true pro brings critical context to the table that you simply wouldn’t have on your own:

- Code Compliance: They are experts in local building codes. If your roof replacement requires bringing things up to current code—like adding new decking, ice shields, or proper ventilation—they can document it. This forces the insurer to cover these often expensive but non-negotiable items.

- Material Expertise: They know how different materials react to storm conditions. They understand the specific size of hail needed to damage an architectural shingle or the wind speeds required to break a shingle’s sealant strip.

- Weather Pattern Analysis: The best contractors will cross-reference the damage they find on your roof with hyper-local weather reports, creating a direct and provable link between a specific storm event and the damage found.

This level of granular detail elevates your claim from a simple "my roof is leaking" request to a comprehensive technical report that an insurance carrier finds much more difficult to argue with or underpay.

Ultimately, the right contractor levels the playing field. They match the insurance company's resources with their own specialized expertise, ensuring that every dented vent, lifted shingle, and damaged flashing is documented, accounted for, and paid for. It’s about having a champion in your corner who makes sure you get what you're owed.

Strengthening Your Home for Future Claims

The best way to win a claim is to prevent a denial in the first place. This means shifting your mindset from reactive repairs to proactive maintenance. It’s not just about fixing your house; it’s about building an ironclad case for any future claims before the storm even hits.

Think of it like this: you're building a file against your own insurance company. By methodically maintaining and documenting the condition of your roof, you take away their favorite excuses, like “wear and tear” or “pre-existing damage,” before they can ever use them.

Documenting a History of Care

One of the oldest tricks in the adjuster's book is to blame storm damage on your roof’s age or a supposed lack of maintenance. A solid documentation strategy shuts that argument down completely.

Get into the habit of scheduling a professional roof inspection every one to two years, and always after a major storm. Keep every single record from these inspections—who did it, what they found, and proof of any small repairs they made. This creates a powerful paper trail that shows you’ve been a responsible homeowner all along.

A well-kept maintenance log is your single best weapon against a "neglect" denial. It proves to the insurer that the damage is new, a direct result of the storm, and not some old issue you let fester.

This file is far more than a stack of receipts. It’s the story of your home's upkeep, and it's a story that's very difficult for an adjuster to argue with.

Upgrading for Resilience and Reward

Beyond regular check-ups, upgrading your roofing materials can be one of the smartest investments you make. Putting high-performance materials on your roof doesn't just give you better protection—it gives you a massive advantage when it's time to file a claim.

Look into upgrading to impact-resistant shingles. They’re built specifically to handle the kind of hail and debris that shreds standard roofing, and they pay off in several ways:

- Higher Durability: Class 4 impact-resistant shingles, for instance, are engineered to withstand hail up to 2 inches in diameter. This drastically cuts down the odds of you having any damage to begin with.

- Insurance Discounts: Most insurance companies love these roofs so much they’ll give you a hefty premium discount for installing one—often between 15% and 30%. The roof can literally start paying for itself on day one.

- Stronger Claim Position: If a monster storm does manage to damage these tougher materials, your claim becomes almost undeniable. It's tough for an adjuster to argue that the damage wasn't caused by a severe, covered event when your roof was built to handle almost anything.

Taking these steps is an investment in your home’s durability and your own peace of mind. When you take control of your roof's condition now, you’re always ready for the next storm and prepared to shut down an unfair denial.

Common Questions After a Roof Claim Denial

Getting that denial letter from your insurance company can be frustrating and frankly, a little confusing. It's easy to feel stuck. Let's walk through some of the most pressing questions homeowners like you have when facing a denied roof claim.

How Long Do I Have to Fight a Denied Claim?

Time is of the essence. As soon as you get that denial notice, the clock starts ticking, so you really can't afford to wait. While the exact window to appeal will be spelled out in your policy and varies by state, it’s important to act with urgency.

You generally have at least 180 days to formally dispute the decision. That said, I always tell homeowners to start the process within 30 days. Moving quickly signals to the insurance company that you’re serious. It also means all the evidence—from your photos to your neighbors' recollections of the storm—is still fresh and compelling. Waiting too long can make it much harder to gather the proof you need to build a strong case.

Will My Insurance Company Drop Me for Appealing?

This is a huge fear for many homeowners, but let me put your mind at ease. It is flat-out illegal for an insurer to cancel your policy or jack up your rates just because you filed a legitimate claim or appealed a denial.

These protections are even stronger when the damage comes from a natural disaster, what they often call an "Act of God." If you even suspect your insurer is penalizing you for pushing back on one of their insurance claim denial reasons, don't hesitate. Contact your state's department of insurance right away and file a formal complaint.

Is It Worth Hiring a Public Adjuster?

A public adjuster can be a real game-changer, especially for very large, complicated claims, or if your own appeal has already been shot down. These are state-licensed pros who work for you, the policyholder, not the insurance company. Their entire job is to go to bat for you and secure a fair settlement.

But before you sign a contract and agree to their fee (which is typically a percentage of your final payout), take this crucial first step: Get an in-depth inspection from a reputable roofing contractor who specializes in storm damage.

More often than not, a detailed report from a seasoned roofer who knows how to document damage is all it takes to get that denial overturned. Start with a contractor, and only escalate to a public adjuster if you're still getting nowhere. This two-step approach could easily save you thousands.

Don't let a denial dictate the fate of your roof. The expert team at Hail King Professionals provides free, same-day inspections to arm you with the clear evidence needed to challenge the insurance company and win your claim. Get your complimentary, no-obligation assessment today.