Does Homeowners Insurance Cover Storm Damage in Texas

When a storm tears through your neighborhood, one of the first questions that races through your mind is, "Am I covered?" The simple answer is yes, your homeowners insurance policy is designed to be your first line of defense against storm damage. But—and this is a big but—it all comes down to what kind of storm damage you have.

A standard Texas policy is built to handle sudden and accidental events. Think of a violent hailstorm or destructive straight-line winds. What it almost never covers is flooding from rising water. That’s a completely different ballgame.

The Short Answer To Your Storm Damage Questions

Whether or not your claim gets approved hinges on the specific "perils" listed in your policy. A peril is just insurance-speak for an event—like wind, hail, or a lightning strike—that your contract agrees to protect you against. Getting a handle on this concept is the single most important step you can take after a storm hits.

Think of your policy as a rulebook for a game. It clearly outlines what plays are covered. That’s why damage from a sudden hailstorm is a classic covered event, while damage from a slow, pre-existing roof leak often isn't. The policy is there to protect you from the unexpected, not from gradual wear and tear.

Covered Perils Versus Exclusions

Most standard homeowner policies in Texas are written to cover the things we worry about most during storm season. However, it's the fine print—the exclusions—that can catch you by surprise.

The most critical exclusion for any Texas homeowner to understand is flooding. If your home is damaged because water from a nearby creek, lake, or street rises up and gets inside, that's a flood. This type of damage requires a separate, dedicated flood insurance policy, which is often managed through the National Flood Insurance Program (NFIP).

Your policy is a specific agreement about cause and effect. It will pay for roof damage from a tree that a windstorm knocked over, but it won't pay if that same tree falls simply because it was old and rotten. The cause of the damage changes everything.

When you're looking at the damage, knowing what’s covered and what isn’t is everything. For instance, a standard policy will cover damage from a tornado's high winds, but not from the storm surge a hurricane might push ashore. For a closer look at what to expect from different types of severe weather damage, it's always a good idea to pull out your policy declarations page.

To make things a bit easier, here’s a quick breakdown of what a typical policy handles.

Quick Guide to Storm Damage Coverage

This table gives you a general idea of what to expect from a standard Texas homeowners policy when it comes to common storm damage.

| Type of Storm Damage | Typically Covered? | What You Need to Know |

|---|---|---|

| Wind & Hail Damage | Yes | This is the heart of storm coverage, but always check for a separate—and often higher—wind/hail deductible. |

| Lightning Strikes | Yes | Covers damage from a direct strike, including fires and power surges that can fry your electronics and appliances. |

| Falling Objects | Yes | This includes trees, limbs, or other debris that a storm blows onto your home. |

| Flood Damage | No | Damage from rising surface water is a major exclusion. You need a separate flood insurance policy for this. |

Understanding these basics puts you in a much stronger position when it's time to talk to your insurance company and begin the recovery process.

What Your Policy Is Designed to Cover After a Storm

Think of your homeowners insurance policy as a specialized shield. It isn’t built to stop every little thing, but it’s exceptionally good at protecting you from specific, sudden attacks. When a Texas storm rolls through, your policy is your first line of defense against the most common types of damage it leaves behind.

The key principle here is that the damage must be sudden and accidental. Your insurance is there for when a violent squall line tears shingles off your roof, not for the slow, predictable wear and tear that happens over decades. Insurers are in the business of covering disasters, not funding routine home maintenance.

Wind Damage Your Policy Addresses

Here in Texas, high winds are a given, whether from a spring thunderstorm or the outer bands of a hurricane. The good news is that standard homeowners policies are written specifically to cover damage caused directly by wind.

This coverage is actually quite broad and kicks in for a lot of common scenarios:

- Missing or Damaged Shingles: This is the most frequent kind of wind damage we see. Gusts can get under the shingles, creasing them, lifting them, or ripping them right off the roof.

- Fallen Trees and Debris: If the wind knocks a tree onto your house, garage, or even your fence, your policy should cover the repairs to the structure. It may also provide a limited amount to help with the tree removal itself.

- Structural Damage: In a worst-case scenario, severe winds can cause catastrophic failures. We're talking about damaged walls or even the roof deck being lifted. This is exactly the kind of major event your policy is meant to handle.

How Hail Damage Is Covered

After wind, hail is the other major headache for Texas homeowners and a top cause for claims. Hail damage is sneaky. It doesn't always cause an immediate leak, but it critically weakens your roof's ability to protect you from the next storm.

When an adjuster gets on your roof, they aren't just looking for holes. They're trained to spot functional damage—the bruising, pitting, and granule loss on shingles that effectively strips away its protective layer and drastically shortens the roof's life.

This functional damage is precisely what your policy is there for. A roof that's been battered by hail is considered a damaged asset, even if it’s not leaking yet. Your insurance gives you the ability to restore its integrity before the next rainstorm sends water pouring into your attic.

Lightning and Electrical Surges

While not as common as wind or hail damage, a lightning strike is incredibly destructive. A direct hit can easily start a fire, shatter brick or masonry, or completely obliterate a tree. Thankfully, lightning is considered a standard "covered peril" in virtually every homeowners policy.

The protection often goes beyond the physical strike, too. A nearby lightning strike can send a massive power surge through your home’s electrical grid. This can instantly fry your expensive electronics, kitchen appliances, and HVAC system. Your policy is designed to help you repair or replace these critical items, making it a crucial safeguard against this powerful and unpredictable threat.

Understanding Your Policy’s Critical Exclusions

Think of your homeowners insurance policy as a powerful tool, but like any tool, it has specific jobs it's designed for—and jobs it's not. The policy's fine print details these limitations, known as exclusions. These are the specific situations your insurance company simply won't cover.

Ignoring these exclusions is one of the fastest ways to get a claim denied and end up with a massive, unexpected bill. It's just as important to know what your policy doesn't cover as what it does.

The Critical Difference Between Rain and Flood Water

Here's the one that trips up more homeowners than any other: flood damage. Most people assume that if a storm causes water to get in their house, they're covered. Unfortunately, it's not that simple. Your policy makes a sharp distinction between water from the sky and water from the ground.

Let's use an analogy. If a hailstorm shatters a window or high winds rip shingles off your roof, any rainwater that gets inside is typically covered. The damage was a direct result of a covered event, like wind.

But what if a massive downpour saturates the ground, causing a nearby creek to spill its banks and send water seeping into your foundation and through your doors? That’s considered a flood. Standard homeowners insurance policies do not cover damage from rising surface water.

To protect your home from rising water, you have to buy a separate policy, usually from the National Flood Insurance Program (NFIP) or a private insurer. Without it, you’re on your own financially when a flood hits.

This single distinction is a tough lesson for many to learn. You can find more on weather-related claim trends from resources like the Insurance Information Institute, but the bottom line is that flooding is a common disaster that leaves many homeowners unprotected.

Other Common Policy Exclusions to Know

Beyond flooding, a few other common exclusions can derail a storm damage claim. Keep an eye out for these in your policy documents.

- Earth Movement: Storms can trigger more than just wind and rain. However, damage from landslides, mudslides, or sinkholes is almost always excluded, even if a hurricane’s rainfall was the catalyst. The insurer points to ground instability as the cause, not the storm itself.

- Gradual Damage: Your policy is built for sudden, accidental events. It’s not a maintenance plan. A slow leak that leads to mold, a pipe that corrodes over a decade, or a roof that's simply worn out won't be covered.

- Wear and Tear: This is a big one, especially for roofs in areas like DFW and East Texas. If an adjuster believes your roof failed during a storm because it was already old, brittle, and past its prime, they’ll likely deny the claim. They'll argue the storm wasn't the true cause; the roof's poor condition was. Being aware of the top reasons an insurance claim might be denied can help you navigate this.

Knowing these exclusions ahead of time isn't about being pessimistic; it's about being prepared. It allows you to set realistic expectations and, more importantly, take steps to get the right coverage in place before the next storm arrives.

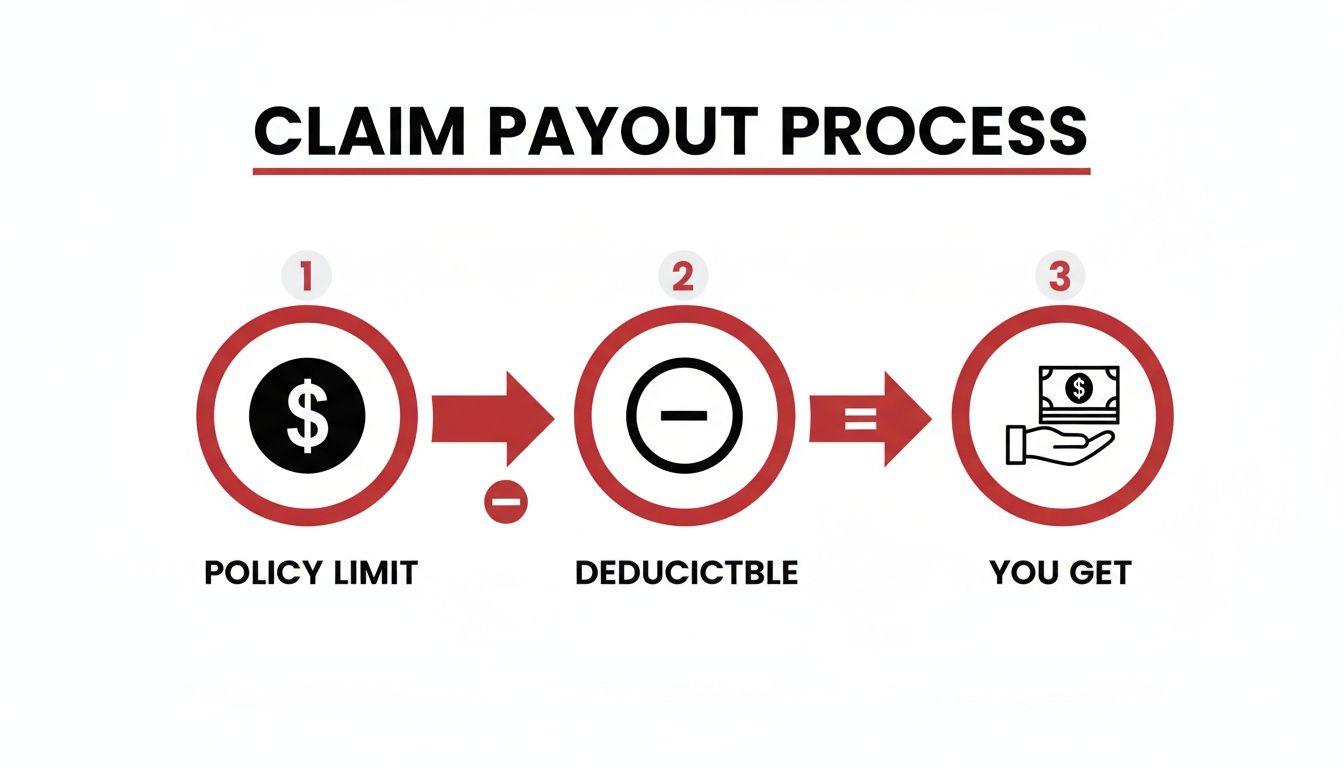

How Deductibles and Limits Affect Your Claim Check

It’s great that your policy covers storm damage, but don’t assume that means you get a blank check for repairs. Your insurance policy is a detailed contract, and understanding a few key financial terms is the only way to know how much money you’ll actually see when you file a claim.

Think of your deductible as your skin in the game. It’s the amount you have to pay out-of-pocket before your insurance company chips in a single dollar. If a hailstorm causes $10,000 in damage to your roof and you have a $2,000 deductible, your insurer’s check will be for, at most, $8,000.

The Two Types of Deductibles You Will Face

Here in Texas, policies often have two different kinds of deductibles. It's crucial to know which one applies to storm damage, because one can be a lot more expensive than the other.

- Flat Deductible: This is a simple, fixed dollar amount—say, $1,000 or $2,500. It typically applies to claims like fire or theft.

- Percentage Deductible: This is the one you’ll usually see for wind and hail damage. Instead of a flat number, it’s a percentage of your home's total insured value (Coverage A), often between 1% and 5%.

Here's where it gets real. If your home is insured for $400,000 and you have a 2% wind and hail deductible, that’s an $8,000 out-of-pocket cost for a new roof ($400,000 x 0.02). That number can be a real shock if you’re not ready for it. Pull out your policy's declarations page and check which deductible applies to you.

Replacement Cost Value vs. Actual Cash Value

After you’ve met your deductible, the next big question is how your insurance company values your damaged property. This almost always boils down to two settlement types: Replacement Cost Value (RCV) and Actual Cash Value (ACV).

An Actual Cash Value (ACV) policy pays you for what your property was worth the moment before it was damaged. It's the replacement cost minus depreciation for age and wear. If your 15-year-old roof gets wrecked, an ACV policy will only give you a fraction of what a brand-new roof costs.

A Replacement Cost Value (RCV) policy is what you really want. It covers the full cost to replace what was damaged with new, similar materials, without factoring in depreciation. This is the gold standard for roofing coverage.

Even with a solid RCV policy, the process has a twist. Insurers usually pay in two chunks. First, you get a check for the actual cash value (ACV). Once you’ve hired a contractor and the work is finished, you submit the final invoice to get the rest of the money, called the recoverable depreciation. You can learn more about making sure your roof replacement is fully covered by insurance in our other guide.

Understanding Your Coverage Limits

Lastly, don't forget about your coverage limit. This is the absolute maximum your insurer will pay for a claim. For your home’s structure (your Coverage A limit), this number needs to be high enough to rebuild your entire house from the ground up if a catastrophe hits.

With storms getting stronger and more frequent, this is more critical than ever. In fact, insured losses from severe storms have soared past $42 billion for three years running, pushing premiums up for everyone. You can read about recent storm loss data and see the trends for yourself. Knowing your limits is the only way to be sure you aren't left underinsured when you need that coverage the most.

A Step-By-Step Guide to Filing Your Storm Damage Claim

Once a big storm rolls through, the clock starts ticking. What you do in the hours and days that follow can make or break your insurance claim. Having a clear plan of attack takes the panic out of the equation and puts you back in the driver's seat, ready to navigate the process and get a fair settlement.

Think of it like a fender bender. You wouldn't just drive off. You'd secure the scene, take pictures, and gather all the info you could before ever calling your insurance. The same exact logic applies to your home—it’s just on a much bigger scale.

Step 1: Prioritize Safety and Prevent Further Damage

First things first: safety. Before you even glance at the roof, check on your family and make sure everyone is alright. If you see downed power lines, smell gas, or have any other immediate safety concerns, get everyone out and call 911 immediately.

Once you know it's safe, your job is to play defense. Your policy actually has a clause requiring you to take "reasonable steps" to prevent more damage from happening. This is called mitigation. It might mean throwing a tarp over a hole in your roof to keep the rain out or boarding up a shattered window. Hang on to every single receipt for these temporary fixes; they’re almost always reimbursable.

Step 2: Document Everything Meticulously

Alright, now it’s time to put on your detective hat. Before moving or cleaning up anything (other than what was necessary for safety), you need to document the scene like a pro. This evidence is the single most powerful tool you have for proving your claim.

Here’s what your documentation checklist should look like:

- Photos and Videos: Take way more than you think you need. Start with wide shots of your entire property, then zoom in for close-ups of every dented gutter, bruised shingle, and cracked window. A video walkthrough where you talk through what you’re seeing is also incredibly compelling.

- Date and Time Stamps: Check your phone's camera settings to ensure every photo is time-stamped. This helps tie the damage directly to the specific storm.

- Create an Inventory: For any personal belongings that got ruined, make a list. Note the item, brand, model, and roughly how old it was. In fact, creating a detailed home inventory for insurance before a storm ever hits can make this part of the process a thousand times easier.

Step 3: Get an Independent Professional Inspection

This is the one step most homeowners skip, and it can cost them dearly. Before you call your insurance provider, call a trusted, local roofing contractor—like us at Hail King Professionals—for a free, no-obligation inspection. Remember, the insurance adjuster works for the insurance company. A professional contractor works for you.

Getting an expert opinion first gives you a massive advantage. An experienced roofer knows exactly what to look for and can spot subtle damage an adjuster might miss. We'll give you a detailed report and a repair estimate that becomes your baseline—a powerful piece of evidence to have in hand when the adjuster shows up. It completely changes the dynamic and puts you on a level playing field.

This is critical because of how the final payout is calculated.

As you can see, your deductible comes right off the top of the approved claim amount. That’s why it’s so important to make sure that initial total includes every single bit of damage.

Step 4: File the Claim and Meet the Adjuster

Now you're ready. With your photos, notes, and independent report in hand, it's time to contact your insurance company. Have your policy number ready and give them a general overview of what happened. They'll give you a claim number—write it down and keep it somewhere safe.

Be Prepared for the Adjuster's Visit: When the insurance adjuster schedules their inspection, make sure you or your contractor can be there. Walk the property with them, point out the damage you documented, and give them a copy of your contractor's report. Be friendly and professional, but be firm in presenting what you've found.

Following this game plan helps ensure the whole claims process goes much more smoothly. For an even deeper look into what comes next, check out our complete guide to the storm damage insurance claim process. By taking these steps, you stop being a victim of the storm and become the manager of your own recovery.

Navigating Special Roofing Challenges in Texas

Texas weather is no joke, and that means a run-of-the-mill roof often just won't cut it. When you're filing an insurance claim after a storm, it’s about more than just getting what you had before. It's about getting your home properly fortified for the next one.

The brutal hail we see in Dallas-Fort Worth and across East Texas has completely changed the game. It's not enough to ask, "does homeowners insurance cover storm damage?" The real question is whether your policy will pay for the right kind of roof to survive what’s coming next.

Upgrading to Class 4 Impact-Resistant Shingles

After a hailstorm wrecks your roof, your insurance company is on the hook to restore your home to its condition right before the storm hit. But here's the thing: this is the perfect moment to upgrade to a far more durable system. We're talking about Class 4 impact-resistant shingles, which are specifically built to take a beating from hail.

Think of it like this: you could put standard highway tires on your truck, or you could go for the all-terrain tires made for Texas backroads. Class 4 shingles are the all-terrain option for your roof. They're built for what our weather throws at them.

Many insurance carriers have done the math and realize how much they save by not having to pay for constant repairs. As a result, they often offer significant premium discounts for homes with certified Class 4 roofs. Over time, the upgrade can pay for itself through lower insurance bills.

When we manage your claim, we'll walk you through this option. Your insurer pays for the standard replacement cost, and you typically just cover the small difference to get a superior product that boosts your home's value and resilience.

The Challenge of Rooftop Solar Panels

Solar panels are a great way to save money, but they do complicate a roof replacement. If storm damage means you need a new roof, all those panels have to be carefully removed before we can work and then reinstalled once the new roof is complete.

This two-step process is called a "detach and reset." It’s a specialty job that requires real precision. The critical part is making sure the cost for this service is included in your insurance claim from the very beginning. It's an expensive line item that many adjusters conveniently "forget," leaving you with a surprise bill that can easily run into thousands of dollars.

A contractor who knows the insurance game will make sure the detach and reset costs are documented and approved as part of the initial claim. It’s a non-negotiable part of the process to get you back to where you were before the storm.

Building Codes and Getting Your Claim Fully Approved

Local building codes are always being updated for better safety and durability. If the codes in your city have changed since your original roof was installed, your insurance policy should pay to bring the new roof up to the current standard. This could involve anything from replacing the underlying wood decking to adding new ventilation.

This is another spot where having a code-savvy expert on your side is a game-changer. We stay on top of the specific municipal requirements across DFW and East Texas. We ensure these code-required upgrades are built into the claim from day one. An insurer is obligated to pay for them, but only if they're properly documented. Without an expert spotting this, it's money homeowners often leave on the table.

Frequently Asked Questions About Storm Damage Claims

When a big storm rolls through, it's natural to feel overwhelmed. Your head is probably spinning with questions about what to do next, especially when it comes to insurance. Let's clear up some of the most common concerns we hear from homeowners every day.

Knowing your rights and what your policy actually says can make all the difference between a smooth recovery and a frustrating, drawn-out battle.

Can My Insurer Drop Me After a Storm Damage Claim?

This is a huge source of anxiety for many, but the good news is that Texas law provides a safety net. An insurance company can't just cancel your policy or refuse to renew it because you filed a single, legitimate weather-related claim, like for hail damage.

Where you can get into trouble is with multiple claims in a short window, usually over three years. This can make you look like a higher risk to the insurer, and they might choose not to renew your policy when it's up. That’s exactly why getting a professional inspection before you call your insurance company is so critical. It helps you confirm the damage is significant enough to justify a claim, so you don't waste a "strike" on minor issues.

What Should I Do If My Claim Is Denied?

A denial letter isn't the final word. Think of it as the starting point for a negotiation. The very first thing to do is get that denial in writing. Your insurer is required to give you a specific reason and point to the exact part of your policy they're using to justify their decision.

With that in hand, it’s time to prepare your appeal.

- Build Your Case: Pull together all your evidence—the photos and videos you took, any receipts for temporary repairs, and most importantly, the detailed inspection report from a trusted contractor.

- Request a Second Look: You are entitled to ask for a different adjuster from the insurance company to re-evaluate the damage.

- Bring in a Public Adjuster: If you’re still hitting a wall, hiring a licensed public adjuster is a powerful next step. They work directly for you, not the insurance company, and their job is to fight for a fair settlement on your behalf.

More often than not, a well-organized appeal backed by professional documentation is enough to get an initial denial overturned.

How Long Do I Have to File a Storm Damage Claim?

Officially, the statute of limitations in Texas generally gives you one year from the date the damage occurred to file a claim. But you should never, ever wait that long. Your policy has a clause that requires you to report damage "promptly" or "as soon as reasonably possible."

Waiting weeks or even months to file can put your claim in serious jeopardy. The insurance company could argue that you didn't act to prevent further damage, or they might say it's impossible to prove the damage came from that specific storm. Your best move is always to report the damage right away.

Trying to manage a storm damage claim on your own can be a tough road, but you don't have to walk it alone. Hail King Professionals provides free, same-day inspections to give you a clear, honest assessment of your situation before you even pick up the phone to call your insurer. Get the expert report you need to ensure a fair and complete settlement by visiting us at https://hailkingpros.com.