Class 4 Shingles Insurance Discount: Your 2026 Guide

If you live in Dallas-Fort Worth or anywhere in East Texas, you know that hail isn't a possibility—it's an inevitability. Every year, storms roll through and leave a trail of damaged roofs in their wake. But what if you could turn your home's biggest vulnerability into one of its smartest financial assets?

That’s exactly what an upgrade to Class 4 impact-resistant shingles can do. Beyond just protecting your home, this investment is your ticket to a significant class 4 shingles insurance discount.

How a Stronger Roof Unlocks Lower Insurance Premiums

Homeowners insurance in Texas can be painfully expensive, and for a simple reason: risk. From an insurer's point of view, a standard asphalt roof is a massive liability, especially in a region nicknamed "Hail Alley." They know that after a major hailstorm, they're going to be flooded with expensive roof replacement claims.

This is where you can take control. By installing Class 4 shingles, you fundamentally change your home's risk profile. These shingles are specially engineered and rigorously tested to withstand serious impacts, which dramatically lowers the chance you'll need to file a claim.

Why Insurers Are Eager to Give You a Discount

For an insurance company, it all comes down to the numbers. A roof that shrugs off hail means fewer payouts for them. It’s a classic win-win situation.

- You get a tougher, more reliable roof and enjoy paying less for insurance every single year.

- Your insurer minimizes its financial exposure the next time a supercell parks itself over your neighborhood.

This is why they offer such compelling discounts. In Texas, homeowners who make the switch to Class 4 shingles often see their premiums drop by 20% to 35%. These shingles are certified under the UL 2218 standard, a brutal test that involves dropping a 2-inch steel ball onto the shingle to simulate large hail. The result? A roof that's built to last.

At Hail King Professionals, we've been helping homeowners across DFW and East Texas since 1991. We’ve seen it time and time again: a client invests in a Class 4 roof and immediately sees their insurance bill shrink. It’s about more than just repairs; it’s a proactive step toward making your home more resilient and financially sound.

Let's Look at the Real-World Savings

It’s one thing to talk about percentages, but what does that look like in actual dollars? A new roof is a significant investment, so understanding its direct financial payback is key.

The following table breaks down the potential savings for a Texas homeowner with a typical insurance policy. We're assuming an average annual premium and a 25% discount for upgrading to a Class 4 roof.

Potential Annual Insurance Savings with Class 4 Shingles

| Annual Homeowners Premium | Dwelling Coverage Portion (70%) | Potential Discount Rate (25%) | Annual Savings | 10-Year Accumulated Savings |

|---|---|---|---|---|

| $4,500 | $3,150 | $787.50 | $787.50 | $7,875 |

| $5,500 | $3,850 | $962.50 | $962.50 | $9,625 |

| $6,500 | $4,550 | $1,137.50 | $1,137.50 | $11,375 |

Note: These figures are estimates. Your actual savings will depend on your specific policy, carrier, and home value.

As you can see, the savings add up fast. Over a decade, that discount can easily put $10,000 or more back into your pocket—money that helps the new roof pay for itself.

Understanding this discount is a big piece of the puzzle, but it’s also important to know what happens when you do need to file a claim. You can learn more about how homeowners insurance covers storm damage to get the full picture.

In the next sections, we'll walk you through the exact steps to claim your discount. With an experienced partner like Hail King Professionals guiding you, the process is straightforward, putting these powerful savings within reach.

What Makes Class 4 Shingles a Smarter Investment

So, what's the big deal with "Class 4" shingles, and why are insurance companies in Texas so eager to give you a discount for them? It all comes down to a brutal test and some serious material science that saves everyone a ton of money in the long run. This isn't just marketing—it's about proven performance that protects your home from the wild weather we get here.

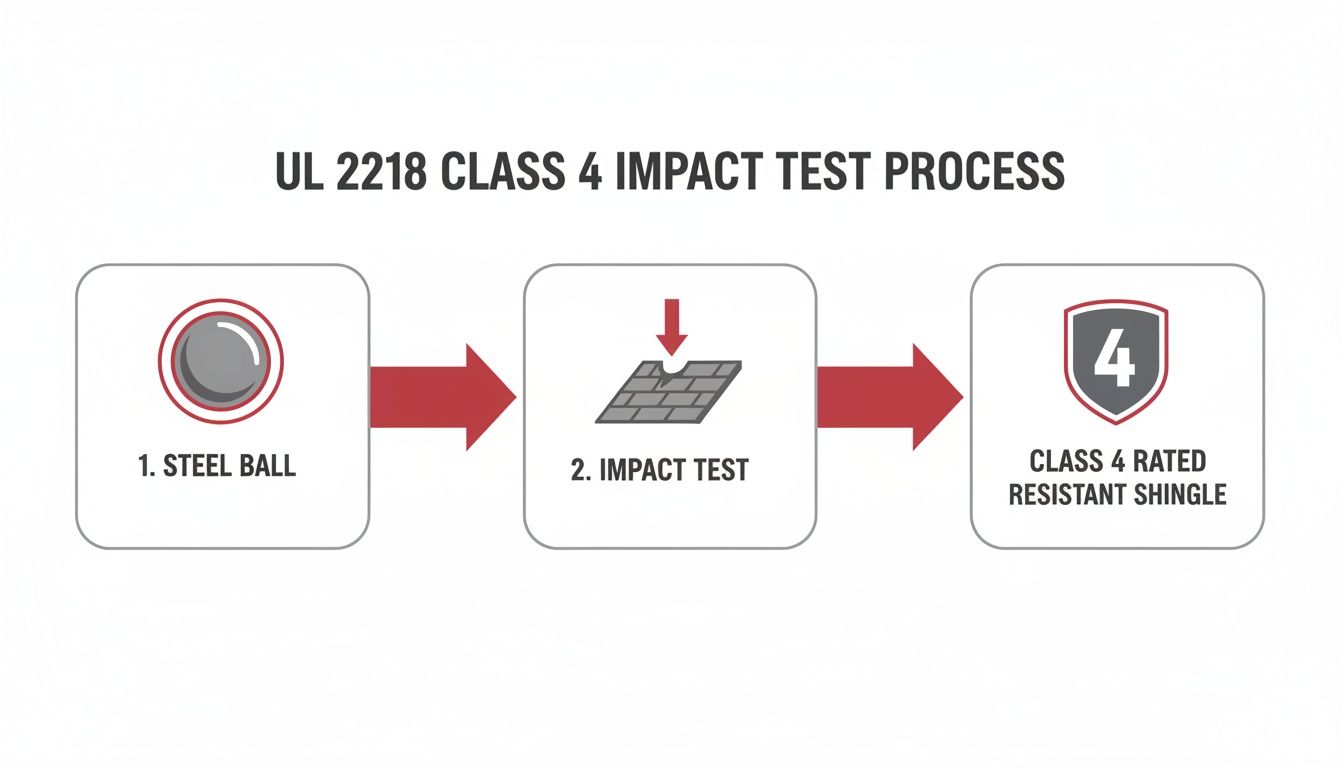

The key to unlocking that class 4 shingles insurance discount is a test called UL 2218. This is the industry-standard gauntlet run by Underwriters Laboratories to certify impact resistance. To pass, a shingle has to withstand a two-inch solid steel ball being dropped on it from 20 feet high. And it has to endure this not once, but twice in the exact same spot, all without cracking or splitting.

Think about that for a second. That test is designed to mimic the violent force of the large, destructive hail that can tear through Dallas–Fort Worth and East Texas, shredding standard roofs and causing billions in damage.

The Science of a Tougher Shingle

How can a shingle possibly take that kind of beating? The secret is in the recipe. Most Class 4 shingles are manufactured with polymer-modified asphalt, which is a fancy way of saying they blend in rubberizing polymers like Styrene-Butadiene-Styrene (SBS).

This gives the shingle a flexible, almost rubbery quality. It’s the difference between dropping a ceramic plate and a tough rubber mat. The plate shatters. The mat absorbs the blow and bounces right back. That’s exactly what these shingles do when hail hits, and it’s why they hold up so much better to our region's punishing freeze-thaw cycles and high winds.

A Win-Win for You and Your Insurer

The practical result of all this engineering is simple: fewer insurance claims. After a big hailstorm rolls through, homes with Class 4 roofs are far less likely to need major repairs. This predictable drop in risk is precisely why insurance carriers are willing to reward you.

Class 4 shingles offer insurance premium reductions of 10-35% across major U.S. markets. These polymer-modified asphalt shingles result in 70-80% fewer claims, prompting carriers to reward proactive homeowners. To learn more about this national trend, you can explore detailed findings about how roof materials lower insurance premiums.

By installing a Class 4 roof, you’re actively reducing the insurance company's financial exposure, and they share a piece of those savings back with you. When you start looking at specific products, you’ll see trusted brand names like Owens Corning, Malarkey, and popular options like GAF Timberline HDZ shingles that are known for their durability.

This upgrade isn't just another home expense; it turns your roof into a genuine asset that protects your investment. You can dive deeper into the different options in our guide on hail-resistant roofing materials. It’s one of the smartest financial decisions a Texas homeowner can make.

How to Secure Your Insurance Discount

Your new Class 4 roof is on, and it looks fantastic. But the job isn't quite finished. Now comes the best part: turning that upgrade into real, recurring savings on your homeowner's insurance.

Claiming your class 4 shingles insurance discount is a pretty straightforward process, but the devil is in the details. You have to be organized and give your insurance company exactly what they need to see. This is where an experienced contractor like Hail King Professionals really shines—we handle this paperwork day in and day out for homeowners across Dallas-Fort Worth and East Texas, so we know the drill.

Getting Your Paperwork in Order

Your insurance agent needs proof, not just a promise. Before you even think about calling them, you’ll want to build a small, organized "evidence file" that proves you've installed a qualifying impact-resistant roof.

Here are the three must-have items for your file:

- Your Final, Detailed Invoice: This is critical. The invoice must specifically list the brand and model of the Class 4 shingles used. A generic receipt that just says "new roof" won't be enough.

- The Manufacturer's Installation Certificate: This is the golden ticket. It's the official document confirming your new roof meets the rigorous UL 2218 Class 4 impact-resistance standard.

- A Few Before-and-After Photos: While not always required, clear photos showing your old roof and the brand-new installation can really help paint a picture for the adjuster and smooth the process.

This simple diagram shows the tough-as-nails test a shingle has to pass to earn that Class 4 rating.

That steel ball test is precisely why insurers are happy to give you a discount. You've actively lowered their risk of paying out a massive claim after the next hailstorm.

Making the Call to Your Insurer

Once you have your documents ready to go, it's time to get in touch with your insurance agent. Don’t be shy about it. You’ve just spent your hard-earned money to make your home safer and more resilient, and you absolutely deserve to be rewarded for it.

When you call or email, be direct and confident. You’re not asking for a favor; you're informing them of a policy-changing upgrade.

Here’s a simple, effective script we've seen work time and time again:

"Hi [Agent's Name], I'm calling to provide an update for my homeowner's policy. We just had a Class 4 impact-resistant roof installed, and I have the invoice and the UL 2218 certificate ready to send over. Could you tell me the best way to submit these documents so we can get the premium discount applied?"

This approach works because it shows you're prepared and you know what you're talking about. It moves the conversation straight to action.

Pro Tip: Time your call wisely. We recommend reaching out 30-45 days before your policy is set to renew. This gives the carrier plenty of time to process your documents and ensure the discount is applied to your next bill, so you don’t miss out on a full year of savings.

Having a roofer who understands this final step is a huge advantage, especially if you're juggling the roof replacement as part of a larger insurance claim. For more on that, take a look at our detailed guide to the storm damage insurance claim process.

Calculating the Total Value of Your Roof Upgrade

Getting an annual class 4 shingles insurance discount is a fantastic win, but that's just the beginning of the story. To really see the full financial picture, you have to look beyond that yearly premium reduction and consider the total return on your investment over the life of the roof.

Think about the last time a nasty hailstorm rolled through Dallas-Fort Worth or East Texas. Homeowners with standard shingles were likely crossing their fingers, worrying about the damage and the looming deductible. With a Class 4 roof, that anxiety is gone. You’re not just saving on your premium; you're effectively erasing the future costs of surprise deductibles and out-of-pocket repairs.

That peace of mind has a real dollar value. By preventing just one or two major storm-related repairs over its lifespan, a Class 4 roof can easily save you thousands. That's pure savings, completely separate from your insurance discount.

Beyond Premiums and Repairs

The financial upside doesn't stop with dodging repair bills. A Class 4 roof is a hard asset that adds significant value, especially when it comes time to sell in our competitive Texas real estate market.

- Increased Resale Value: A documented, high-performance roof is a huge selling point. Buyers instantly recognize the value of lower insurance costs and long-term durability, which often means homes with Class 4 shingles sell faster and for more money.

- Preventing Premature Replacement: Let's be honest—standard shingles in our region rarely make it to their advertised lifespan. The relentless Texas sun and frequent storms wear them out fast. A Class 4 roof, on the other hand, is built to last 20-30 years or more, helping you sidestep the massive expense of a premature reroof.

- Texas-Specific Durability: These shingles aren't just for hail. Their tough construction, which often uses polymer-modified asphalt, makes them exceptionally resistant to the intense UV radiation and high winds that are a fact of life here.

This durability is also crucial if you're thinking about solar. At Hail King Professionals, we do a lot of solar panel detach-and-reset services for roof replacements. A Class 4 roof provides a stable, long-lasting foundation, ensuring you won't have to pay to remove and reinstall your entire solar array just for a roofing issue a few years down the line.

"Smart homeowners in DFW look for ways to 'stack' their discounts. When you get a Class 4 roof, call your agent and ask if you qualify for other credits, like having a security system or being claims-free. Combining these can amplify your total savings far beyond what the roof discount alone provides."

The Complete Financial Picture

When you put all the pieces together, the math becomes pretty clear. Yes, the upfront cost is typically 10-25% more than standard architectural shingles. But that initial investment is quickly balanced out by a powerful combination of immediate discounts and long-term savings.

You’re not just buying tougher shingles; you're investing in a financial shield for your home. It’s a strategic decision that pays you back year after year, delivering a return that goes far beyond a simple line item on your insurance bill.

Choosing the Right Partner for Your Installation

When it comes to getting that Class 4 shingles insurance discount, the roofer you choose is just as important as the shingles themselves. A great installation by the right team ensures your roof performs as promised, but more importantly, it guarantees you’ll have the correct paperwork to actually secure your savings.

Think of it this way: your contractor is your guide through the entire process. The wrong one can leave you with a poorly installed roof and a denied discount claim. A true expert, on the other hand, handles everything from the initial inspection to the final certification, making the whole experience seamless.

The Hail King Professionals Advantage

Here in Dallas-Fort Worth and East Texas, you need a roofer who truly gets our weather. With over 30 years of experience in this specific region (we started back in 1991), Hail King Professionals has seen it all. We’ve built our business on being transparent, trustworthy, and knowing the local insurance game inside and out.

Our approach is different. We begin with a free, same-day inspection to give you a clear, honest assessment of your roof’s condition. You won’t get a high-pressure sales pitch from us—our job is to educate you on your options so you can make the best choice for your home.

This deep experience is invaluable when you're dealing with an insurance claim. We know exactly what adjusters look for and how to document storm damage properly, ensuring your claim gets a fair shake.

A True One-Stop Shop for Restoration

After a big hailstorm, the damage is rarely limited to just your roof. That’s why we manage the entire exterior restoration. Instead of you having to juggle multiple contractors, we handle it all.

Our restoration services cover:

- Roofing: Expert installation of asphalt, metal, and of course, Class 4 impact-resistant shingles.

- Gutters and Siding: We’ll repair or replace damaged sections to protect your home’s siding and foundation.

- Fencing: Complete restoration for wood or metal fencing that’s been hit by hail or high winds.

- Window Screens: We can quickly replace any screens that were torn or dented in the storm.

We stand behind our work with a 100% satisfaction guarantee. Your peace of mind is what matters most. We’re not done with the job until you are completely happy with the outcome.

Making Your Upgrade Accessible

We know a new roof is a major investment. To help make this critical home upgrade more manageable for Texas families, we offer flexible financing options. Our plans include soft credit checks, which won't ding your credit score, so you can explore your budget without any pressure.

When you work with Hail King Professionals, you’re not just hiring a roofer. You’re getting a dedicated partner committed to protecting your home for the long haul. We’ll take care of the complexities so you can sit back and enjoy the savings and security that come with a properly installed Class 4 roof.

Answering Your Questions About Class 4 Shingle Discounts

Even when you know a Class 4 roof is the right move, it's normal to have a few lingering questions. We get it. This is a big decision, and you want to be sure you're looking at it from every angle. Let's dig into the common questions we hear from homeowners across Dallas-Fort Worth and East Texas every day.

How Much More Does a Class 4 Roof Really Cost Upfront?

This is the big one, right? Let's not beat around the bush: you can generally expect a Class 4 roof to cost about 10% to 25% more than a standard architectural shingle roof. On an average home, that could be a few thousand dollars extra.

But looking at that number as just a "cost" is the wrong way to think about it. It’s an investment. That extra money starts working for you from day one with lower insurance premiums, and it really pays off by helping you sidestep those massive, out-of-pocket repair bills after the next big hailstorm.

What Should I Do If My Insurer Denies the Discount?

First off, don't get discouraged. We've seen this happen before. A homeowner does everything right, and the initial request gets denied, often because of a simple clerical error or a misunderstanding.

If you get a "no," calmly ask for the specific reason in writing. This is crucial. Once you have that, here’s what to check:

- Go Over Your Paperwork: Did you send the final, paid-in-full invoice? Did you include the official UL 2218 certificate for the shingles? Sometimes it’s as simple as a missing document.

- Check the Product List: Make sure the exact shingle you had installed is on your insurer's approved list of impact-resistant products.

- Politely Escalate: If the paperwork is perfect and the product is eligible, it's time to ask for a supervisor. The first person you talk to might not be an expert on underwriting or these specific discounts. A little persistence goes a long way.

Can I Upgrade My Roof Even If It Isn't Damaged?

Absolutely! In fact, it’s one of the smartest moves a homeowner in our area can make. You don't have to wait for a storm to force your hand. Many people choose to proactively replace an older roof, especially if it's a basic builder-grade product, to start cashing in on insurance savings and get some peace of mind.

Think of it like this: You wouldn't wait for a blowout on the highway to buy better tires for your car. Upgrading your roof on your own terms gives you control over the timing, your choice of contractor, and your home’s ultimate protection.

What If I Just Had a New Standard Roof Installed?

This is a tough spot to be in, and we get this question more often than you'd think. If you’ve just put a brand-new standard roof on your home, tearing it off for an immediate upgrade probably doesn't make financial sense—unless, of course, it’s already been hit by another storm.

The best approach here is to play the long game. Keep all the documents for your current roof, and make a plan to upgrade to Class 4 when this one reaches the end of its natural life or gets damaged in a future storm. You won't get the discount today, but you'll be perfectly positioned to make the right call when the time comes.

Ready to lock in those insurance savings and put a Texas-tough roof over your head? Hail King Professionals is here to make the process simple and clear. Get your free, no-obligation roof inspection and find out how much you could be saving.