Your Guide to Roof Replacement Financing Options

A new roof is one of the biggest investments you'll make in your home, but figuring out how to pay for it doesn't have to mean draining your savings. The most common roof replacement financing options are personal loans, home equity financing (which includes both loans and lines of credit), and specialized in-house contractor programs. The right path for you really comes down to your credit, how quickly you need the work done, and whether you're prioritizing a low interest rate or just getting it done fast.

Why Financing Your New Roof Is Now a Common Strategy

Let's be honest—facing a roof replacement, especially in storm-prone areas like Dallas-Fort Worth and East Texas, can feel overwhelming. It’s a huge expense. The days when most homeowners could simply write a check from their savings are quickly disappearing, which is why financing has become a go-to strategy.

The roofing industry has exploded, growing from $10.84 billion in 2023 to a projected $15 billion by 2030, largely because of aging homes and an uptick in climate-related storm damage. On top of that, material costs have shot up by 35% since 2020 due to inflation and supply chain headaches. With a typical roof replacement running anywhere from $9,000 to $28,000, paying out-of-pocket is a tough pill to swallow.

Key Reasons to Consider Financing

Financing isn't just about covering a large bill; it's a smart way to protect your home's most important asset without putting yourself in a financial bind. It allows you to act now, preventing a small problem from turning into a catastrophic one.

- Immediate Protection: You can address urgent storm damage or age-related failures right away, stopping leaks before they cause serious structural issues.

- Preserve Savings: Keep your emergency fund right where it is. You never know what other unexpected life events are around the corner.

- Access to Better Materials: Financing can give you the budget to upgrade to superior materials, like impact-resistant shingles, which offer much better long-term protection and might even earn you a discount on your homeowner's insurance.

- Budget-Friendly Payments: A large, scary number becomes a series of predictable monthly payments that you can actually plan for.

When you finance, you're not just buying a roof. You're making a calculated investment in your home's future safety and value without sacrificing your current financial stability. It transforms a massive, stressful expense into a manageable upgrade.

Getting familiar with the different roof replacement financing options is your first step. Each one—a quick personal loan, a low-interest home equity loan, or a convenient contractor program—is designed for a different situation. We’ll break down these choices to help you see which one makes the most sense for you. For a closer look at what a new roof might cost in our area, check out our guide on the cost of a new roof in Texas.

Comparing Your Top Roof Financing Options

Deciding how to pay for a new roof comes down to a classic trade-off: cost versus speed and convenience. The three main paths homeowners take are personal loans, home equity financing (like HELOANs and HELOCs), and financing directly through their roofing contractor.

Let's break down what each one really means for your wallet and your project timeline. Seeing them side-by-side helps clarify which route is the best fit for your specific circumstances.

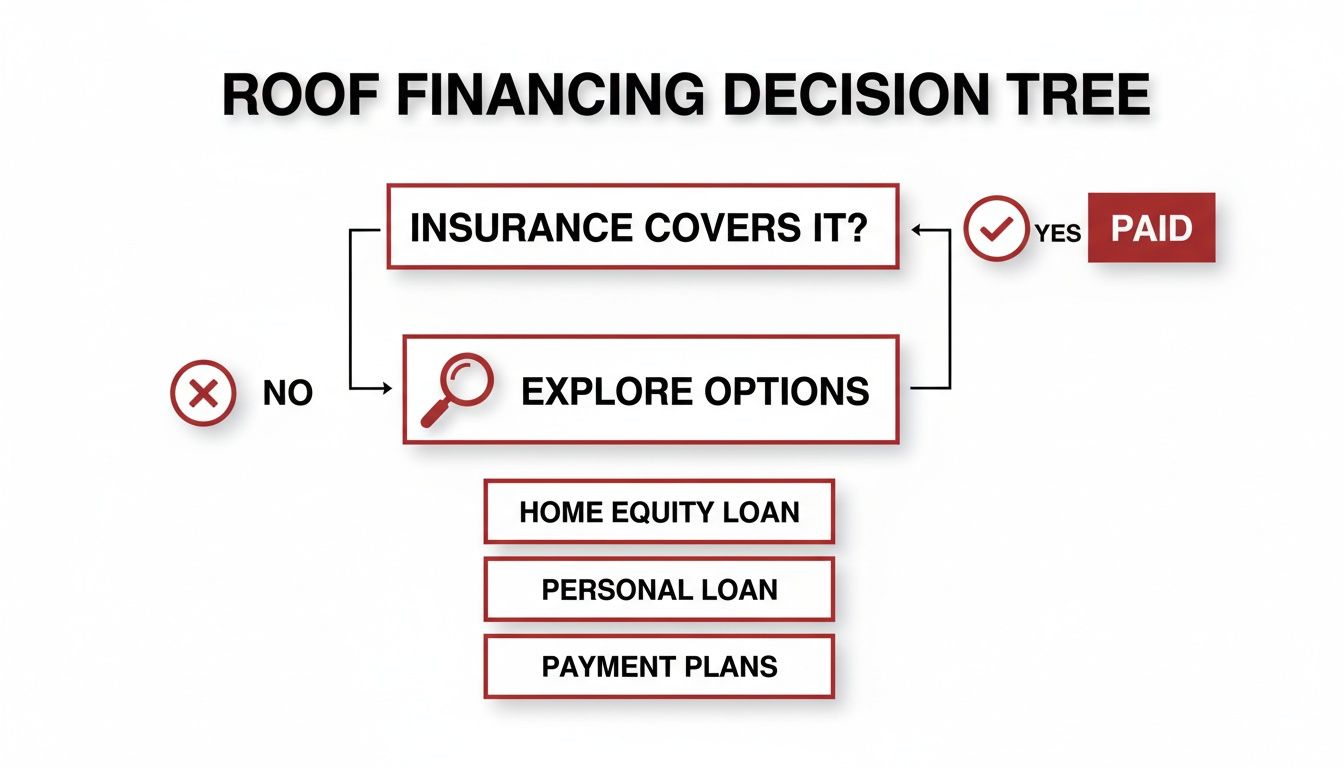

Before diving into loans, your first question should always be about insurance. This decision tree shows how financing only enters the picture after you know what your policy will—or won't—cover.

As you can see, when insurance pays for only part of the roof or none at all, financing becomes your next logical step. And that’s a very common scenario for homeowners.

Personal Loans vs. Home Equity vs. Contractor Financing

To make a smart choice, you have to look past the marketing and focus on the details that actually matter during a big home project. We're talking about the interest rate you'll lock in, how long you have to pay it back, and what it takes to even get approved in the first place.

Here’s how these three popular methods really stack up.

The biggest differentiator is often collateral. Personal loans and most contractor financing are unsecured, which means your home isn't on the line. Home equity loans and HELOCs, on the other hand, are secured by your house, which is a risk you need to be comfortable with.

To make this even clearer, the table below gives you a quick side-by-side view of these options. Use it to zero in on the best choice based on your financial situation and how quickly you need to get the work done.

At-a-Glance Comparison of Roof Financing Options

| Financing Type | Typical APR Range | Loan Term | Credit Score Impact | Collateral Required | Best For |

|---|---|---|---|---|---|

| Personal Loan | 8% – 36% | 2-7 years | Moderate (hard inquiry) | No | Homeowners with good credit who need fast, unsecured funds for urgent repairs. |

| Home Equity | 6% – 12% | 5-30 years | Moderate (hard inquiry) | Yes (Your Home) | Homeowners with significant equity seeking the lowest possible interest rate for a large project. |

| Contractor Financing | 0% – 29% | 1-15 years | Low (soft pull initially) | No | Homeowners prioritizing convenience, speed, and a simple application process integrated with their project. |

So, Which One Should You Choose?

Honestly, there's no single "best" option—it all depends on your situation. Your credit score, how much equity you have, and the urgency of the repair will point you in the right direction.

Here are some real-world guidelines to help you decide:

Go with a Personal Loan if: You have a solid credit score (think 670 or higher) and need money fast, like within a few business days. It’s perfect for an urgent fix when you don’t want to put a lien on your home.

Go with a Home Equity Loan/HELOC if: Your main goal is the absolute lowest long-term cost, and you have plenty of equity built up in your home. This is the right move for a planned replacement, not an emergency, because the approval process can take 30-45 days.

Go with Contractor Financing if: You value convenience and speed above all else. This is the path for homeowners who want a one-stop-shop experience. Many programs, including the one we offer at Hail King Professionals, start with a soft credit check that won't ding your score while you explore your options.

Think of it this way: a homeowner in Dallas with fresh hail damage needs their roof fixed now to stop leaks. A personal loan or quick contractor financing makes the most sense. But someone planning a roof upgrade in six months to improve their home’s look can afford to wait for a HELOC and its lower interest rate. It's all about matching the financing to the reality of your situation.

Using Personal Loans for Roofing Projects

When your roof needs immediate attention, a personal loan is often the most direct path to getting the cash you need. Think of it as a straightforward loan based on you, not your house. Lenders look at your credit profile—your score, income, and history—to decide on your loan. Because it’s an unsecured loan, your home isn't on the line as collateral.

This is a huge plus for many homeowners. You get the full loan amount in one lump sum and then pay it back with fixed monthly payments. These payment plans, or terms, usually run anywhere from two to seven years. The beauty of this is predictability; your payment is the same every single month, making it easy to budget for.

What really sets a personal loan apart is its speed. While a home equity loan can get bogged down in appraisals and paperwork for weeks, you can often get approved and funded for a personal loan in just a few business days. This makes it perfect for those urgent repairs, like when a hailstorm leaves you with a damaged roof and you simply can’t afford to wait.

The Personal Loan Application Process

Getting a personal loan isn't as intimidating as it might sound. Most of the process happens online and is designed to be quick. Here’s a rundown of what to expect.

Check Your Rates (Pre-Qualification): The best first move is to get pre-qualified with a few different lenders. This is a quick check-up where you provide some basic financial details. It relies on a soft credit pull, which does not impact your credit score, and gives you a sneak peek at the rates and terms you could get.

Compare Your Offers: With a few offers in hand, you can lay them out and compare. Look closely at the Annual Percentage Rate (APR), the length of the loan (term), and any hidden fees. Your goal is to find the right balance—a lower APR and a shorter term will always save you the most money in the long run.

Lock it in (Formal Application): Once you’ve picked your winner, you’ll submit the official application. This step does involve a hard credit inquiry, which might ding your score by a few points temporarily. You'll also need to upload documents to prove who you are and what you earn, like recent pay stubs or a utility bill.

Get Your Funds: After you’re approved and you’ve signed the final loan agreement, the money usually lands in your bank account within 1-3 business days. From there, it’s cash in hand to pay your roofer and get the project started.

Real-World Cost Example

So, what does this look like for your wallet? Let’s say you’ve been quoted $15,000 for a full roof replacement. The interest rate and the loan term you choose will make a big difference in your monthly payment.

Here’s a quick breakdown:

| Loan Amount | APR | Term | Estimated Monthly Payment |

|---|---|---|---|

| $15,000 | 9% | 5 Years | $311 |

| $15,000 | 12% | 5 Years | $334 |

| $15,000 | 15% | 7 Years | $298 |

Notice how a longer term can lower your monthly payment, but you'll end up paying more in total interest over the life of the loan. It's a trade-off between monthly affordability and overall cost.

A key takeaway is that personal loans offer simplicity and speed. For homeowners who value quick access to funds without putting their house on the line, the potentially higher interest rate is often a worthwhile trade-off for the peace of mind and immediate protection it provides.

In the end, a personal loan is a fantastic option if you have a solid credit score (generally 670 or higher) and need to fix your roof now, not later. It lets you tackle a critical home repair without delay, all while keeping your payments predictable and your home’s equity safely on the sidelines.

If you've built up some value in your property over the years, you might be sitting on one of the best ways to pay for a new roof. Using your home equity can unlock some of the most attractive financing options out there. Unlike a personal loan that hinges entirely on your credit score, home equity financing uses your house as collateral, which makes lenders feel a lot more secure.

For you, that lower risk for the lender usually means two big wins: a lower interest rate and a longer repayment period. These benefits can make a major expense feel much more manageable. When you go to tap that equity, you'll generally find two main paths: a home equity loan (HELOAN) or a home equity line of credit (HELOC).

HELOAN vs. HELOC: What's the Difference?

While both options leverage your home's equity, they work in completely different ways. The right choice really comes down to what your project looks like and how you want to handle the money.

Home Equity Loan (HELOAN): Think of this as a traditional loan. You get the entire amount in one lump sum and pay it back with fixed, predictable monthly payments. It’s perfect when you have a firm quote and know the exact cost of your new roof.

Home Equity Line of Credit (HELOC): This operates more like a credit card. A lender approves you for a maximum credit limit, and you can draw money as you need it, paying interest only on what you've actually used. This makes it a great fit for larger renovations with moving parts and uncertain final costs.

A HELOAN offers certainty. You get a fixed payment for a known cost. A HELOC, on the other hand, delivers flexibility. It lets you draw funds as needed, which is ideal if you’re bundling projects like a new roof, siding, and gutters all at once.

The Trade-Offs of Using Home Equity

Those low interest rates are tempting, but it’s not all upside. The single biggest thing to remember is that your home is the collateral. If you can't make the payments for any reason, the lender can foreclose on your property. It's a serious risk to weigh.

The application process is also a heavier lift than getting a personal loan. You'll need a home appraisal to confirm how much equity you have, and the paperwork is more extensive. Be prepared for the process to take anywhere from 30-45 days. You might also face closing costs, much like you did with your original mortgage.

When you're ready to explore this path, checking out top-rated Cash Out Refinance Lenders is a smart move to ensure you're getting the best terms possible.

When to Choose Home Equity Financing

So, when does tapping your home equity make the most sense? This approach really shines in specific situations where the benefits outweigh the longer timeline and inherent risks.

Scenario: Imagine a Dallas homeowner who needs a new roof quoted at $18,000. They're also thinking about tackling their old siding ($12,000) and rusty gutters ($3,000) at the same time but aren't 100% sure on the final, all-in cost.

Here, a HELOC is the clear winner. They could open a line of credit for around $35,000 to cover the whole project. As each phase gets underway—roofing, then siding, then gutters—they can draw the exact funds needed. This way, they only pay interest on the money they actually spend, avoiding the stress of borrowing too much or not enough and creating a cushion for any surprises.

Understanding In-House Contractor Financing

Juggling bank applications and loan officers can feel like a full-time job on its own. That's precisely where in-house contractor financing comes in, offering one of the most direct and convenient ways to pay for a new roof. Many established roofing companies, including Hail King Professionals, work directly with lenders to build financing programs just for home improvement projects.

Instead of you having to shop for loans yourself, the financing process is woven directly into your roofing project. It creates a one-stop-shop experience where the same team replacing your roof also helps you line up the money to pay for it. The whole point is to cut through the financial red tape and get your project moving without delay.

How Contractor Financing Works

The process is refreshingly simple. When you get an estimate for your roof, your contractor will also walk you through the financing options they offer through their lending partners. The application itself is usually a quick digital form you can fill out in just a few minutes.

A huge advantage here is the use of a soft credit check to get started. Unlike the "hard inquiry" you'd face with a personal loan or home equity line, a soft pull lets you see what rates and terms you might qualify for without dinging your credit score. It's a no-risk way to see your options.

Once you’re pre-approved and ready to go, the final approval often comes back in a few hours, not days or weeks. That speed is a game-changer, especially if you're dealing with urgent storm damage and can't afford to wait around.

The true value of contractor financing is how it syncs up the project and the payment. You're not stuck playing telephone between a bank and your roofer; everyone is on the same page, making the entire process smoother from start to finish. That peace of mind is one of its biggest draws.

Key Advantages of This Approach

Opting for a contractor's financing program comes with some unique perks you won't always find with traditional bank loans. These features are specifically built for homeowners taking on a major project.

- No Home Equity Required: These are typically unsecured loans, meaning your home isn't used as collateral. For many homeowners, this removes a major source of stress and risk.

- No Prepayment Penalties: Most solid programs let you pay off the loan ahead of schedule without any extra fees. This gives you flexibility—if your insurance check comes in or you get a bonus at work, you can wipe out the debt and stop paying interest.

- Built for Home Improvement: The loan terms are often designed with projects like roofing in mind. You might find promotional offers like deferred payments or interest-free periods that you wouldn’t get with a standard personal loan.

For homeowners in Dallas-Fort Worth and East Texas, these programs are an essential tool for managing the budget. We know that regional factors can make a big difference in cost. For instance, roof replacement costs in 2026 can swing wildly by location; a project that runs $15,000 in a smaller town could easily hit $25,000 or more in a market like DFW where labor and demand are higher.

When to Choose Contractor Financing

So, is this the best route for you? Contractor financing really shines when your top priorities are speed, simplicity, and convenience.

Picture this: a hailstorm wrecks your roof. Your insurance is covering most of it, but you have a $4,000 deductible to meet and you want to spend an extra $5,000 to upgrade to impact-resistant shingles. You need to get this done fast to prevent leaks.

Instead of waiting weeks to get a home equity loan approved, you can use your contractor's financing to cover that $9,000 gap. The application gets done right when you sign the project contract, you get approved the same day, and work can start right away. You’ve protected your home and invested in a better roof without draining your savings or going through a drawn-out loan process. This unified approach makes funding your project just as straightforward as figuring out how to choose a roofing contractor in the first place.

Managing Insurance Claims and Financing Gaps

When a storm hits, most homeowners I talk to assume their insurance will simply cut a check for a brand-new roof, covering 100% of the cost. But in my experience, that's rarely how it plays out. More often than not, there’s a gap between what the insurance company pays and the final project total.

So, where does this gap come from? First, you always have your deductible, which can be anywhere from a few hundred to several thousand dollars out-of-pocket. The bigger issue, though, is that many policies only cover the Actual Cash Value (ACV)—what your old, worn-out roof was worth—not the full replacement cost of a new one. This is exactly where financing becomes a smart financial tool.

Bridging the Financial Gap Strategically

Smart financing isn't about taking on debt; it's about strategically managing cash flow to get the best possible outcome for your home without draining your savings. Whether you use a small personal loan or a contractor's financing plan, you can put those funds to work in a few key ways.

- Cover Your Deductible: Instead of pulling a large chunk of cash from your emergency fund, you can finance the deductible and break it down into predictable monthly payments.

- Pay for Upgrades: Insurance is designed to replace what you lost. If you want to seize the opportunity to upgrade to better materials, like durable Class 4 impact-resistant shingles, financing can cover that difference. It turns a necessary repair into a long-term investment.

- Bridge the ACV vs. Replacement Cost Gap: This is the big one. If your policy only pays out the depreciated value, financing can make up the difference to ensure you get a full, quality roof replacement without cutting corners.

Don’t think of financing as just a last resort. View it as a bridge that gets a high-quality roof over your head now, protecting your home from further damage while you sort out the insurance details.

If your insurance payout feels frustratingly low, it's so important to know your options. Understanding how to go about disputing a denied or underpaid roof insurance claim can make a huge difference in your final out-of-pocket cost. Once you have a clear picture of what insurance will really cover, you can figure out the exact amount you need to finance.

The insurance world is complicated, but getting a handle on it is part of the process. For a deeper dive, check out our guide on the storm damage insurance claim process. By pairing a successful claim with the right financing option, you set yourself up for a smooth, worry-free project.

Frequently Asked Questions About Roof Financing

Thinking through how to pay for a new roof brings up plenty of questions. It's a big investment, after all. We've heard just about all of them from homeowners here in Texas, so we've put together some straightforward answers to the most common concerns we run into.

Can I Get Roof Financing with a Low Credit Score?

Yes, you absolutely can. Don't let a less-than-perfect credit score stop you from looking into your options. While it’s true that traditional banks and lenders often look for a score of 670+ for unsecured personal loans, financing programs offered by contractors are a different ballgame.

These programs are built with home improvement projects in mind and can be more flexible. They often look beyond a single number. A great starting point is to go through a contractor's soft credit check. It won’t ding your credit, and it gives you a real-world look at what you can get approved for without any commitment.

Should I Use Financing to Pay My Insurance Deductible?

This is a smart and very common move. When a hailstorm hits, you suddenly have a new roof to deal with, and you might not have a few thousand dollars for the deductible just sitting around. Using a small loan or a contractor's financing plan is the perfect way to bridge that gap.

Financing your deductible means you can get the roof replaced right away. That's the most important thing—it stops leaks in their tracks and prevents small problems from turning into major structural damage. You protect your home without having to drain your emergency fund.

Is a Bank Loan Better Than a Roofer's Financing?

Honestly, the "better" option really boils down to what you value most. If you have an excellent credit score and a long-standing relationship with your local bank or credit union, you might be able to secure a slightly lower interest rate. The trade-off? Their process is almost always slower and packed with more paperwork.

On the other hand, a roofer's financing is designed for one thing: getting your project done. The application is woven directly into the roofing process, approvals can happen in minutes, and the terms are tailored for this exact type of work. If you're looking for speed, simplicity, and a process that just works, contractor financing is hard to beat.

Ready to see what your financing options look like without the guesswork? The team at Hail King Professionals can walk you through our simple, transparent financing solutions. We start with a no-impact soft credit check to see where you stand. Learn more and get your free inspection by visiting us at https://hailkingpros.com.