Restoration Companies Dallas: Your 2026 Expert Guide

The storm has passed, but the hard part usually starts when the noise stops. You step outside, see shingles in the yard, hear neighbors comparing notes, and notice that slow drip in the hallway that wasn’t there yesterday. Your phone fills up with texts, your insurer’s app wants documentation, and within hours somebody’s already knocking on the door offering to “handle everything.”

That’s when Dallas homeowners get into trouble.

I’ve watched this market for a long time, and the biggest mistake isn’t waiting too long. It’s moving too fast with the wrong contractor. In storm-heavy regions, 70 to 80 percent of restoration companies fail to track their true lead conversion rates, which sounds like an internal business problem until it lands on your property as sloppy intake, poor communication, pricing mistakes, and a crew structure that falls apart once the job starts, according to this close-rate analysis of restoration operators. The company may look organized from the outside and still be improvising behind the scenes.

If your home is wet, exposed, or unsafe, stabilize your living situation first. For families who can’t stay put after flood or major water intrusion, this guide on flood displacement relief via corporate housing is a practical place to start.

The rest is about control. Good restoration companies dallas homeowners can rely on don’t push panic. They create order. They document first, protect the property second, coordinate with insurance third, and only then start repairs with a clear scope.

After the Storm Your DFW Homeowner's First Steps

The first hour after a North Texas storm is when emotions drive bad decisions. You want the leak stopped, the blue tarp up, the claim filed, and somebody trustworthy on site. All of that matters. But if you skip documentation or let the wrong company take over too early, you can create problems that follow the job from inspection to final payment.

Start with safety, not the roof

Stay on the ground. Don’t climb a wet roof, don’t step into standing water near electrical hazards, and don’t let a stranger you met five minutes ago start tearing off damaged materials before the property is documented. If there’s active leaking, move belongings, use containers to catch water, and take broad photos before you start cleanup.

The first pass should answer three questions:

- Is anyone in immediate danger from structural collapse, electricity, broken glass, or contaminated water?

- Is the home still weather-tight enough to remain occupied for the night?

- What needs temporary protection now versus full repair later?

A rushed signature solves the contractor’s problem first. A documented property solves the homeowner’s problem first.

Slow down enough to create a record

Walk the exterior at ground level and the interior room by room. Use your phone to capture wide shots, closeups, and short videos with audio. Say the date, time, and what you’re looking at. That helps later when you’re sorting photos for an adjuster.

Make notes while it’s fresh:

- Where you first saw damage. Front slope, patio cover, garage ceiling, dining room window trim.

- What changed after the storm. New stains, popping sounds, loss of power, leaks around vents, fence movement.

- Anything with time sensitivity. Active leak, saturated drywall, pooled attic water, detached gutter, exposed underlayment.

The industry side of restoration is messier than most homeowners realize. The same operational blind spots that hurt a contractor’s close-rate tracking often show up as missed appointments, vague scopes, and crews that don’t know what sales promised. If a company can’t manage its own process, it won’t manage your claim cleanly either.

Call for help, but listen closely to how they respond

The right first call is to a local contractor or restoration firm that can inspect quickly and explain what they’re seeing without pushing you into a contract on the spot. A solid intake call feels calm and specific. They’ll ask where the water is entering, whether the home is safe, whether you’ve documented damage, and whether any emergency protection is needed before a full inspection.

What doesn’t work:

- Pressure to sign immediately before inspection details are discussed

- Cash-only language or vague promises to “waive” obligations without explaining how billing works

- No interest in documentation for insurance

- No clear plan for temporary dry-in, mitigation, or next steps

The best first step after a storm isn’t speed by itself. It’s organized speed.

The First 24 Hours Recognizing Damage and Getting Help

The first day is about separating what’s obvious from what’s easy to miss. A lot of storm damage in DFW isn’t dramatic from the curb. You may not see a tree through the roof. What you’ll often find instead is a chain of smaller failures: bruised shingles, lifted flashing, dented gutters, displaced ridge components, wet insulation, window screen damage, and staining that shows up inside long before the roof leak becomes visible from the street.

What to look for from the ground

Start outside. Walk the full perimeter slowly and look up at the roofline, not just the roof surface.

Check for these signs:

- Gutters and downspouts. Dents, fresh granules collecting in troughs, loose straps, disconnected downspouts.

- Metal components. Impacts on vents, soft metals, flashing, chimney caps, and valley metal often show hail clearly.

- Siding and paint. Cracks, chips, lifted panels, impact marks, or moisture behind seams.

- Windows and screens. Bent screens, cracked glazing, damaged bead lines, water at interior trim.

- Fence and accessory structures. Leaning sections, torn stain finish, displaced caps, punctures on metal surfaces.

Then move indoors. Ceiling stains matter, but so do subtler signs. Look for bubbling paint, swollen baseboards, damp insulation smell in closets, and changes around light fixtures, attic accesses, and vent boots.

Document before anyone touches the property

Homeowners often put themselves at a disadvantage by letting emergency work start before they’ve built a basic file. Temporary protection is fine. Undocumented removal is not.

Use a simple documentation routine:

- Create one album per area on your phone. Roofline, bedrooms, garage, attic, exterior elevations.

- Take one wide shot first, then medium shots, then closeups.

- Photograph personal property separately from building damage.

- Keep notes on weather timing and when you first noticed each issue.

- Save any contractor handouts or business cards from the first day.

Practical rule: If a contractor wants to remove materials, ask what will be documented first, what must be preserved, and who will share those records with you.

What a same-day inspection should actually include

A proper inspection isn’t a guy glancing from the driveway and saying, “Yep, you need a roof.” It should include exterior review, interior leak tracing when relevant, photos, and a discussion about immediate stabilization. If the house has attic access, that should be part of the visit when it’s safe.

A no-pressure inspection should cover:

- Visible storm-related damage on roofing, gutters, siding, screens, soft metals, and related components

- Interior moisture indicators and likely entry paths

- Temporary protection needs such as tarp placement or sealing exposed areas

- Insurance-readiness through photos and a written summary

- Next steps that make sense whether you file a claim or not

One local option among restoration companies dallas homeowners often consider is Hail King Professionals’ guide on choosing a roofing contractor, especially if the damage is primarily on the roof and exterior envelope rather than a full interior mitigation event.

Red flags in the first visit

A bad first visit usually tells on itself.

Watch for these problems:

- They diagnose everything instantly without inspecting enough to know.

- They won’t leave documentation unless you sign.

- They talk only about insurance money, not scope, safety, or workmanship.

- They can’t explain who handles what if the project involves roofing, drywall, painting, gutters, or solar.

- They downplay interior moisture because it’s less visible than exterior damage.

A good contractor restores order. A bad one adds noise.

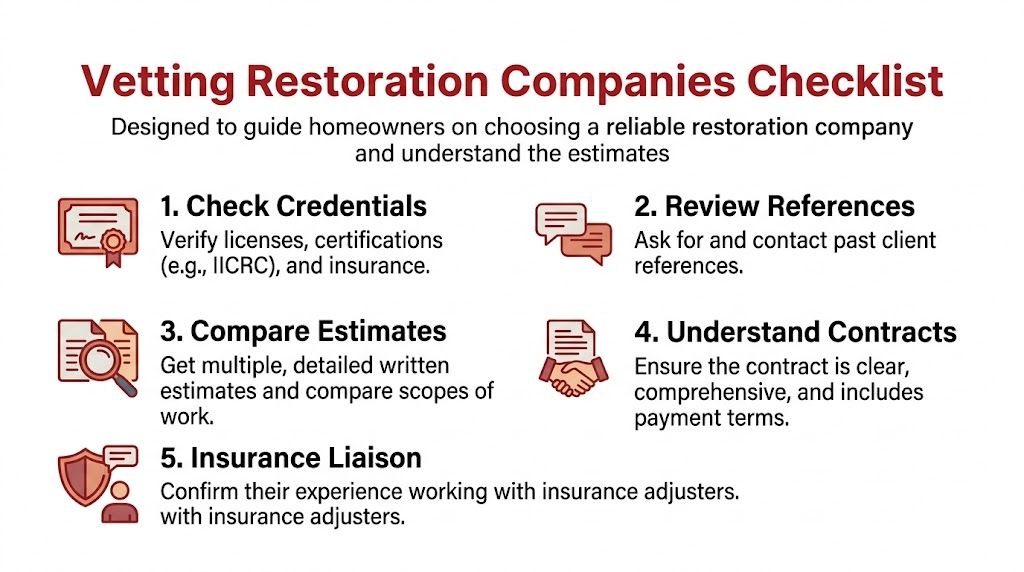

How to Vet Dallas Restoration Companies and Decode Estimates

The Dallas-Fort Worth market is crowded, but it isn’t immature. Established operators with deep local experience and round-the-clock capability already set the bar. Cotton GDS has operated in Dallas for nearly 30 years, and RMC has served the area since 1985, which tells you what real institutional depth looks like in this market, as outlined in this overview of Dallas restoration operations and coverage. If a company is presenting itself as a serious restoration partner, compare it against that standard, not against the lowest bidder.

Credentials that matter before price

Start with the basics. Ask the company to show proof of insurance and explain who is covered on your property. If you want a plain-English primer on why this matters, this overview of General Liability Insurance for Contractors in Texas is useful before you sign anything.

Then verify how they operate:

- General liability coverage. You want current proof, not a verbal assurance.

- Workers’ compensation status. Ask directly who is responsible if a worker gets hurt.

- Scope capability. Can they handle roofing only, or mitigation, reconstruction, painting, gutters, siding, and screens too?

- Local references. Ask for addresses or neighborhoods, not generic testimonials.

- Emergency response process. Who answers after hours, and who shows up?

Online reviews can help, but they’re not enough. Read them for patterns. Do people mention the same project manager by name? Do complaints focus on communication and supplement delays? Reviews are most useful when they reveal how the company behaves after the contract is signed.

How to read the estimate without getting buried in jargon

An estimate isn’t just a price. It’s a map of what the company thinks the job is.

Look for these categories:

- Protection and prep. Tarping, interior protection, debris handling, magnetic sweep, site cleanup

- Core repair scope. Tear-off, underlayment, shingles, flashing, ventilation, decking replacement if needed

- Related trades. Gutters, siding, fascia, screens, drywall, paint

- Allowances or exclusions. Items they expect may change, or items they are not including

- Administrative line items. Overhead and profit, permit handling, dump fees, detach-and-reset items if applicable

If you see O&P, that means overhead and profit. Homeowners often get hung up on that line because they think it’s padding. Sometimes it isn’t. On complex, multi-trade storm work, it can reflect actual coordination responsibilities. What matters is whether the estimate is detailed and whether the company can explain why each category is there.

Don’t compare bids by bottom-line price alone. Compare what each company says it will actually build, replace, protect, document, and warranty.

A simple way to compare bids side by side

Use one sheet and force every bidder into the same layout. That’s how you spot who omitted work and who wrote a realistic scope.

| Line Item | Company A (Cost/Details) | Company B (Cost/Details) | Company C (Cost/Details) |

|---|---|---|---|

| Roof tear-off and replacement | |||

| Underlayment type | |||

| Flashing and vents | |||

| Gutter replacement or reset | |||

| Interior protection and cleanup | |||

| Decking replacement terms | |||

| Solar detach and reset | |||

| Warranty details | |||

| Insurance supplement support | |||

| Exclusions and allowances |

What usually jumps out in a table like this is not honesty versus dishonesty. It’s completeness versus vagueness. The low bid often leaves out code-related items, protection work, accessory trades, or realistic contingencies. That doesn’t make it cheaper. It makes it unfinished.

Questions that expose weak operators fast

Ask these in conversation, not by email only:

- Who writes the estimate and who runs the job? If those are different people, how do they hand off details?

- What happens if the adjuster misses items? Listen for a clear supplement process.

- Who coordinates specialty trades? Important on homes with solar, custom gutters, or interior water damage.

- How do you handle daily cleanup and homeowner communication?

- What isn’t included right now? A trustworthy estimator will tell you.

The best restoration companies dallas homeowners hire don’t get defensive when you ask hard questions. They’ve heard them before, and they answer cleanly.

Navigating Your DFW Homeowners Insurance Claim

Insurance is where most homeowners feel outmatched. The roof is visible. The paperwork isn’t. And that gap creates anxiety fast, because you’re trying to translate storm damage into claim language while also protecting your house and managing family life.

That’s also where a lot of online advice falls short. There’s a real content gap around insurance claim navigation for Dallas homeowners, especially around adjusters, deductibles, depreciation, and what contractors should do versus what they should never promise, as noted in this review of the gap in restoration company guidance.

The first claim call

Keep the first call simple. You’re opening a claim, not arguing the whole file.

A clean version sounds like this:

“We had storm damage at the property. I’ve documented visible exterior and interior issues, and I need to open a claim. Please confirm the claim number, the next steps, and when the field adjuster or inspector can be scheduled.”

Write down the claim number, representative name, date, and anything they ask you to provide. Don’t speculate about causes you can’t verify. Don’t minimize damage either. State what you observed.

Adjuster versus contractor

These roles are different.

The adjuster represents the carrier and evaluates the claim under the policy. The contractor evaluates what it takes to repair the property correctly. Good projects happen when both sides are looking at the same conditions, the same materials, and the same scope.

That’s why I prefer the contractor to be present at the adjuster visit when possible. Not to “fight” the adjuster. To identify missed items in real time, point out collateral damage, and walk through trade-specific issues before the estimate hardens into something incomplete.

For a deeper homeowner-facing explanation of that process, this walkthrough of the storm damage insurance claim process is a useful companion.

Terms that matter when the paperwork arrives

Three terms cause the most confusion:

- ACV. Actual Cash Value. This is typically the depreciated value the carrier assigns before final recoverable amounts are released, subject to policy terms.

- RCV. Replacement Cost Value. This reflects the cost to replace with like kind and quality, again subject to policy language and scope approval.

- Depreciation. The amount withheld until qualifying work is completed and documented, depending on how your policy is written.

You don’t need to become an insurance professional. You do need to know that the first number you see is not always the final amount tied to the completed scope.

When the insurance scope is lower than the contractor scope

This happens all the time. It doesn’t automatically mean bad faith, and it doesn’t automatically mean your contractor is inflating the job. It usually means someone missed something, interpreted the scope differently, or priced a necessary item outside the first pass.

Common friction points include:

- Accessory items omitted such as gutters, screens, flashing, or paint-related tie-ins

- Code-related requirements not included in the initial estimate

- Interior items that became visible after drying, removal, or closer inspection

- Solar coordination when detach-and-reset wasn’t accounted for

- Material mismatch issues where partial replacement doesn’t restore a uniform result

Supplements are relevant. A legitimate supplement is documented support for work the first estimate didn’t include or didn’t price correctly. It should be tied to photos, measurements, line items, and a clear explanation.

Take a minute to watch this overview if you want a visual on how homeowners should think about claims and restoration coordination.

Deductibles, depreciation, and homeowner responsibility

No honest contractor should treat your deductible like a technicality. It’s part of your policy obligation. What you need from the contractor is transparency about where insurance funding ends and where your direct responsibility starts.

Ask for this in writing:

- What insurance has approved so far

- What the contractor expects to supplement

- What upgrades are elective and out of pocket

- What documentation is needed to recover withheld amounts

- When final invoicing happens

If you keep the claim organized, attend the adjuster meeting when you can, and work with a contractor who can document scope cleanly, the process becomes a lot less mysterious.

Managing the Restoration Project From Start to Finish

Once the contract is signed, the quality of project management matters as much as the quality of materials. Homeowners usually focus on the roof system, which makes sense. But jobs go sideways because of scheduling gaps, poor trade coordination, and weak communication long before a shingle is nailed down wrong.

What should happen before materials arrive

You should have a pre-construction conversation, whether it’s formal or not. That’s where the project manager confirms scope, staging, access, protection needs, and sequencing.

Cover these points before work starts:

- Where crews will park and stage materials

- How landscaping, pool equipment, and fences will be protected

- Which elevations or rooms are affected

- What the daily communication plan looks like

- Who has authority to approve changes

If a homeowner asks me one practical question before the start date, it should be this: “What does a normal workday on my house look like?” A good company answers that without fumbling.

What a well-run workday looks like

You should expect noise, debris movement, and steady foot traffic. You should not expect confusion about the scope, workers asking you what was sold, or leftover debris every evening.

A professional day usually includes:

- Arrival and setup with site protection in place before tear-off or interior work

- Active production with a supervisor or lead checking progress

- Material control so bundles, accessories, and removed debris aren’t scattered carelessly

- End-of-day cleanup with magnet sweep and property review

- Status communication so you know what was completed and what’s next

On a multi-trade storm job, the homeowner shouldn’t have to serve as the general contractor. If you’re coordinating roofers, painters, gutter crews, and drywall crews yourself, the job isn’t being managed.

The solar panel issue most contractors underestimate

DFW has a lot more solar-equipped homes than it did a few years ago, and that changes reroofing. Solar arrays can’t be treated like patio furniture. On a house with rooftop panels, the project needs a real detach-and-reset plan.

That means sorting out:

- Who disconnects and removes the panels

- Who stores hardware and documents layout

- How roof work and reinstall timing line up

- Who checks penetrations and flashing after reset

- Who handles responsibility if damaged components are found

Weak operators become evident. Some roofers bid the roof and “figure out solar later.” That’s how delays happen, warranties get muddied, and finger-pointing starts. The right approach is coordinated scheduling and written responsibility before the first panel comes off.

Your role during the project

You don’t need to hover, but you do need to stay reachable. Approve changes in writing. Walk the site when invited. Report concerns early, not after final payment.

Keep your own file updated with:

- Material selections

- Change approvals

- Photos of progress

- Delivery receipts or completion notices

- Warranty information as it becomes available

Restoration is never just one task in Dallas. Roof, gutters, paint, fencing, screens, siding, and interior repairs often move together after a storm. The smoother those handoffs are, the better the result.

Project Financing and Final Walkthrough

Restoration costs can move from manageable to serious very quickly, especially when water is involved. In Dallas, water damage restoration averages between $3 and $7.50 per square foot, roof repairs run about $400 to $2,000, and mold removal ranges from $1,200 to $3,800, according to Angi’s Dallas water damage cost guide. Those numbers are why financing conversations shouldn’t be treated as an afterthought.

How the money usually flows

Insurance-funded projects often don’t pay out in one clean check tied neatly to one contractor invoice. There may be an initial payment, later adjustments, supplement-related revisions, and recoverable amounts tied to completed work and documentation under the policy.

That creates three distinct buckets of money:

- Insurance-approved scope

- Your deductible and any non-covered items

- Optional upgrades you choose to add

That last bucket matters more than people think. A homeowner may decide to improve ventilation, upgrade shingle type, replace additional gutters for a uniform look, or address unrelated wear while crews are already mobilized. Those aren’t always part of the covered loss.

When financing makes sense

Financing isn’t just for people who can’t pay. Sometimes it’s a cash-flow decision. If insurance is covering the core claim but you want better materials or broader exterior work, financing can keep the project moving without forcing rushed choices.

Review terms carefully and ask about:

- Whether the credit check is soft or hard

- Whether prepayment is allowed without penalty

- Whether home equity is required

- How funds are disbursed

- Who gets paid and when

For homeowners comparing payment structures for larger roof-related scopes, this overview of roof replacement financing options is a practical starting point.

Don’t rush the closeout

The final walkthrough is where you protect yourself from small unfinished details that become big annoyances later. Walk the property with the project manager in daylight. Check every elevation, every gutter run, all painted surfaces, screen replacements, interior patches, and cleanup zones.

Create a punch list if needed. It can be short, but it should be specific. Note missing touch-up paint, unsealed trim, debris in flower beds, misaligned downspouts, screen fit, or leftover material.

Before you sign completion paperwork, collect:

- Material warranty documents

- Labor warranty terms

- Paid invoice or payment summary

- Any photos or reports tied to the claim

- Instructions for future service calls

A clean finish isn’t just cosmetic. It’s proof the company can land the job as well as it started it.

Frequently Asked Questions About DFW Roof Restoration

Is it smarter to repair storm damage only, or think long term?

If the damage is isolated and the system is otherwise in solid shape, targeted repair can make sense. But in North Texas, homeowners get burned by treating every storm as a one-off event. The better mindset is asset management. You’re not just patching a roof. You’re deciding how much resilience you want the property to have the next time hail or extreme heat hits.

Do upgrades like impact-resistant shingles actually matter in Texas?

Yes, they can. A major gap in restoration content is the lack of straight talk about long-term durability and maintenance ROI in Texas, especially around Class 4 impact-resistant shingles and roof coatings. Those upgrades can reduce insurance premiums and help extend roof life, according to this discussion of storm damage restoration gaps and preventive strategy. That shifts the decision from “How cheaply can I get through this claim?” to “What will hold up better over time?”

If you plan to stay in the house, durability usually beats the cheapest compliant option.

Are roof coatings and preventive maintenance worth discussing after a storm claim?

They are, if the roof type and condition make them relevant. Too many contractors treat maintenance as separate from restoration, when the better conversation is how today’s repair affects tomorrow’s service life. On the right system, a proactive approach can make more sense than waiting for visible failure.

Will better restoration work help resale value?

It can, especially when the project includes meaningful upgrades rather than bare-minimum replacement. In Dallas, when major restoration includes substantial improvements such as new roofing in severe damage situations, property values can increase by 10 percent to 30 percent or more, according to the Dallas cost and restoration overview cited earlier in the article. Buyers notice clean documentation, newer exterior systems, and materials chosen for local weather instead of short-term convenience.

What’s the biggest mistake homeowners make after a DFW storm?

They choose based on speed and charisma instead of process. The company that gets your attention first isn’t automatically the company that can coordinate insurance, manage solar, protect interiors, sequence trades, and finish strong. Good restoration work is organized, documented, and boring in the best possible way.

If you need a practical next step after hail, wind, or water damage, Hail King Professionals handles roof restoration, exterior repair coordination, insurance documentation support, and solar panel detach-and-reset for DFW properties. The useful first move is a clear inspection, a written scope, and honest guidance on whether you need repair, replacement, or temporary protection first.