Asphalt Shingle Roof Replacement Cost: Texas 2026

For a standard 2,000-square-foot home, an asphalt shingle roof replacement typically falls between $8,000 and $17,000. In practical Texas budgeting terms, many homeowners also see a working range of $7,000 to $15,000 depending on material choice, labor, tear-off scope, and how complex the roof is.

If you're reading this after a hailstorm, a ceiling stain, or a contractor just told you your roof is at the end of its life, the first question is usually simple: how bad is this going to hit the budget? That question matters even more in Dallas-Fort Worth and East Texas, where a roof often isn't a cosmetic project. It's a weather-driven replacement that can't wait long.

The good news is that asphalt shingle roof replacement cost is usually manageable once you break it into real line items and monthly planning instead of treating it like one giant mystery invoice. A roof is still a major expense, but it doesn't have to feel like a financial ambush.

Your Asphalt Roof Replacement Cost First Look

A lot of homeowners call right after the same moment. They find shingle granules in the gutter, see a water spot in a bedroom, or notice the neighbor's roof getting replaced after a storm and start wondering if they're next.

The first baseline to know is this: in 2025, the national average cost to replace an asphalt shingle roof for a typical single-family home ranges from $6,800 to $14,500, with most homeowners paying between $10,000 and $11,000. For a standard 2,000-square-foot home, costs typically fall between $8,000 and $17,000, according to this asphalt shingle roof cost breakdown.

What that range means in real life

That spread is wide because not all roofs are built, accessed, or replaced the same way. A basic walkable roof with standard asphalt shingles lands very differently than a steep, cut-up roof with multiple valleys, chimney flashing, and decking issues discovered during tear-off.

In North Texas, storms also distort timing. After a hail event, demand goes up fast. That affects scheduling, crew availability, disposal logistics, and sometimes pricing.

Practical rule: Don't judge a roof bid by the total alone. Judge it by what work is actually included.

Why homeowners get stuck

Few homeowners set aside funds for a roof on a monthly basis. The requirement often arises unexpectedly, yet the expense only feels abrupt because contractors frequently fail to provide clear explanations. Property owners receive a single-page estimate with a significant figure at the bottom and lack a distinct understanding of what causes that price to increase or decrease.

That's where the budgeting side matters. If you understand what belongs in the estimate, what upgrades are worth paying for, and how to spread the project across monthly payments, the decision gets much clearer.

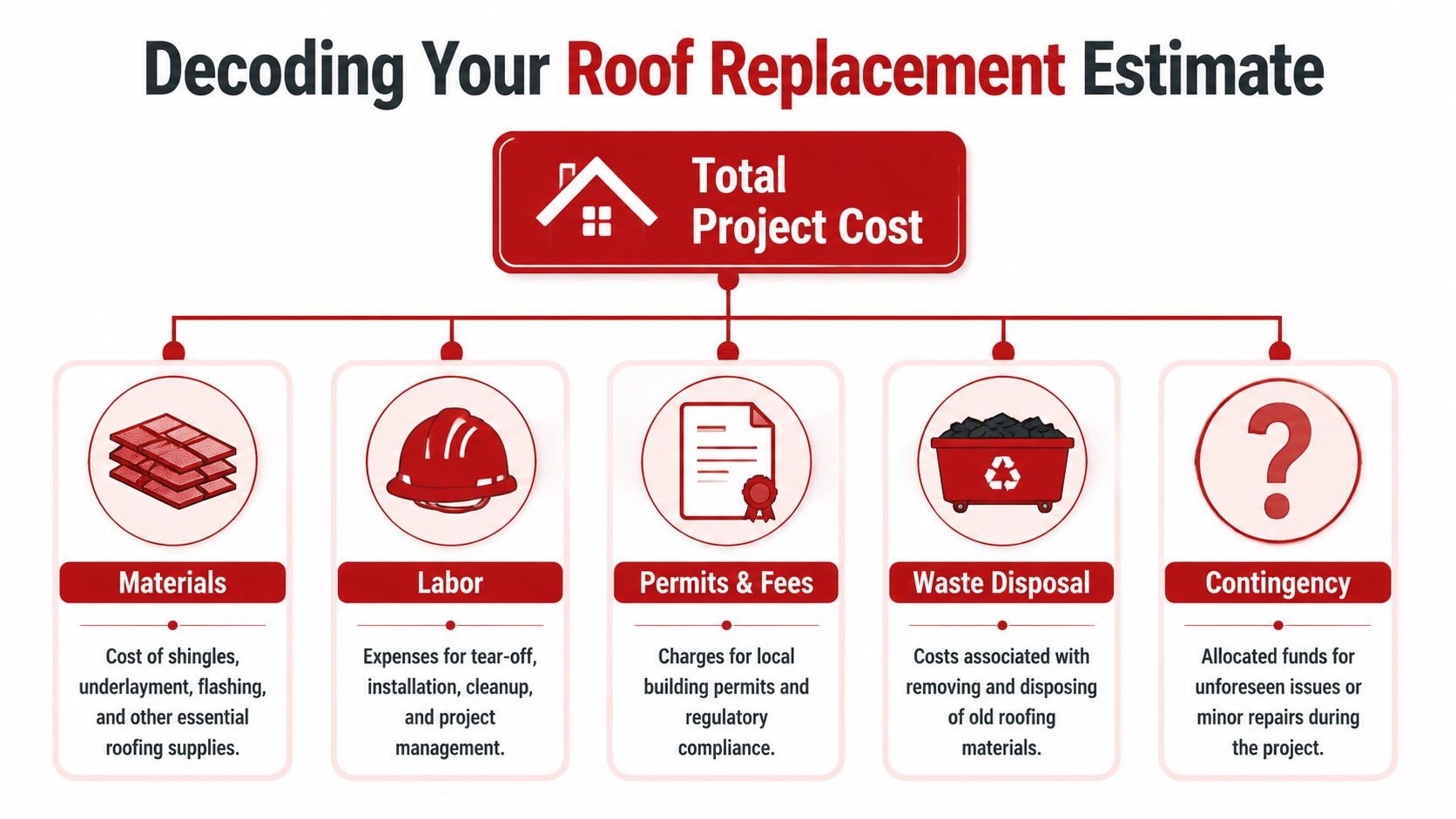

Decoding Your Roof Replacement Estimate Line by Line

A roof estimate shouldn't read like a parts list from another industry. It should tell you what is being removed, what is being installed, what code-related items are included, and what could still change if the crew opens the roof and finds hidden damage.

The installed cost of asphalt shingle roof replacement is typically benchmarked between $3.50 and $12.50 per square foot, with material at $1.50 to $4.50 per square foot and labor and overhead making up roughly 55% to 70% of total cost. For a common 2,000-square-foot roof in Texas, that translates to a practical budget of $7,000 to $15,000, based on roofing replacement cost benchmarks.

First, understand square foot versus square

Roofers use two units all the time:

- Square foot means exactly what you think it means.

- Square means 100 square feet of roof area.

If a roofer says your home has 20 squares of roofing, that means about 2,000 square feet of roof surface. That number can differ from your home's interior square footage because roof geometry, pitch, overhangs, and design complexity all change the actual area being covered.

What a roof estimate usually includes

A proper estimate for asphalt shingle roof replacement cost usually includes these categories:

| Cost Component | Average Cost Range | Percentage of Total |

|---|---|---|

| Materials | $1.50 to $4.50 per sq ft | Varies |

| Labor and overhead | Qualitatively the largest cost category | Roughly 55% to 70% |

| Tear-off and removal | Included in total installed range | Varies |

| Permits and fees | Included in total installed range | Varies |

| Waste disposal | Included in total installed range | Varies |

That table matters for one reason: it helps you compare bids on scope, not just on price.

The line items that deserve the closest look

Some items sound minor on paper but drive long-term performance.

- Shingles: Entry-level products cost less upfront, but they aren't the same roof as an upgraded architectural shingle system.

- Underlayment: This is your secondary water barrier under the shingles. It matters most when wind lifts shingles or water backs up in vulnerable areas.

- Flashing: Chimneys, wall transitions, valleys, vent pipes, and step flashing details are where shortcuts show up first.

- Labor: This isn't just nail-gun time. It includes tear-off, staging, cleanup, safety setup, supervision, and warranty responsibility.

- Disposal: Old shingles are heavy. Dump fees and haul-off aren't glamorous, but they belong in the bid.

A cheap estimate often isn't cheaper roofing. It's usually less scope, weaker details, or important work shifted out of the written contract.

Red flags in a bid

If you want an apples-to-apples comparison, look for what isn't said.

- Missing tear-off language: If the bid doesn't clearly say the old roof is being removed, ask.

- No mention of flashings: That can mean reusing worn metal where replacement would be smarter.

- No permit reference: In many cities, that isn't something to gloss over.

- No decking discussion: A contractor can't promise exact deck replacement before tear-off, but they should explain how it would be handled if damaged wood is found.

A solid estimate doesn't have to be long. It just has to be specific.

Key Factors That Influence Your Final Price

Two houses can sit on the same street, use the same shingle brand, and still get very different roof replacement numbers. That isn't a pricing trick. It's usually roof design, access, and condition.

One of the biggest mistakes homeowners make is assuming the roof is just "the size of the house." It isn't. A simple ranch-style roof is straightforward to tear off, load, dry in, and shingle. A steep roof with multiple ridges, hips, valleys, and penetrations takes more labor, more time, and tighter detail work.

Roof shape changes labor fast

Think about the difference between laying flooring in a plain rectangular room and laying flooring in a house full of corners, angles, closets, and transitions. Roofing works the same way.

More cuts mean more labor. More valleys mean more waterproofing detail. More penetrations mean more flashing work. Steeper pitch means slower movement, more safety setup, and harder material handling.

Common price drivers

- Pitch and walkability: A steeper roof takes longer and requires more caution.

- Cut-up design: Dormers, gables, valleys, skylights, and chimneys all add detail.

- Access: Tight driveways, landscaping, fences, and limited dump trailer access affect crew efficiency.

- Tear-off condition: Multiple old layers or brittle material can slow removal.

- Decking repairs: Rotten or delaminated wood discovered after tear-off has to be addressed before new roofing goes on.

Tear-off is usually the right move

Homeowners sometimes ask if a new layer can just go over the old one. In practice, a full tear-off is the cleaner long-term solution because it lets the contractor inspect the deck, replace damaged components, and build the system correctly from the base up.

Overlay jobs can hide problems. They don't show you wet decking, failed flashing, or ventilation issues. They also make future tear-offs heavier and messier.

If a roof already has age, hail wear, or leak history, covering it up usually postpones the real problem instead of solving it.

Some upgrades are protection, not upsells

Ventilation, flashing replacement, and underlayment upgrades often get treated like optional add-ons in conversations, but they affect whether the new roof performs under Texas weather. A good contractor should explain why each item is included and where it matters most.

Insurance and liability also matter more than many homeowners realize. If you want to understand what proper contractor coverage looks like before anyone climbs on your roof, this overview of roofing contractor insurance is a useful reference.

Resale value is part of the decision

A roof isn't just a repair expense. It also affects marketability, inspection results, and how buyers view the house. Asphalt shingle roof replacement shows a national cost recovery of 60% to 70% upon resale, and in the East South Central region the average reaches 81%, according to Fixr's ROI analysis for asphalt shingle roofing.

That doesn't mean every upgrade pays back equally. It does mean that replacing a worn-out roof usually supports both protection and property value. In plain terms, a good roof keeps becoming someone else's problem off the listing sheet.

Upgrading for Texas Weather With Class 4 Shingles

In DFW and East Texas, "standard roof" and "smart roof" are not always the same thing. If your home sits in a hail corridor, shingle choice matters far beyond curb appeal.

Class 4 shingles cost more upfront, but in a storm market they often make more financial sense than the cheapest option on the board.

What you're actually paying for

Upgrading to Class 4 impact-resistant shingles adds an estimated $1.50 to $4.50 per square foot, or about $5,000 to $10,000 for a 2,000-square-foot roof. The tradeoff is stronger impact performance, extended warranties, and possible insurance discount eligibility, with a potential payback period of 10 to 15 years in active hail corridors like North Texas, based on Fixr's asphalt shingle installation cost analysis.

That upgrade isn't for everyone. If you're planning to sell very soon, you may prefer to keep the system basic and code-compliant. But if you're staying in the home and your neighborhood gets hit often, the upgrade deserves a serious look.

Where Class 4 makes the most sense

Class 4 usually pencils out better for homeowners who fit one or more of these situations:

- Storm repeat zones: Your area sees frequent hail events and repeated insurance claims.

- Long-term ownership: You're planning to stay long enough to benefit from the durability.

- Insurance-conscious budgeting: You're trying to reduce future claim headaches and improve resilience.

- Higher exposure roofs: Large open roof planes with little tree cover tend to take direct weather more aggressively.

A lot of the value isn't visible on installation day. It shows up later when the next storm hits and the roof has a better chance of holding its line.

Installation details still matter

A premium shingle on a sloppy install is still a risky roof. Better performance depends on the full system being handled correctly, including underlayment choices, flashing details, and fastening patterns.

This short video gives helpful context on how impact-resistant roofing is discussed in the field:

For homeowners weighing the insurance side of the decision, this guide on Class 4 shingles and insurance discounts is worth reviewing before you finalize material selection.

Better shingles don't eliminate storm risk. They improve your odds of avoiding the same expensive conversation again too soon.

Navigating Insurance Claims for Hail and Storm Damage

Most Texas roof replacements don't start with a remodeling dream. They start with weather. Once hail or wind gets involved, the roof decision becomes half construction project and half paperwork exercise.

The first step is documentation. Take photos from the ground if you can do it safely, note any interior leaks, and write down the date of the storm if you know it. Then call your insurance company and get the claim started.

The terms that confuse most homeowners

Insurance language tends to slow people down more than the damage itself.

- Deductible: This is the portion you're responsible for under your policy.

- ACV: Actual Cash Value. This usually reflects depreciated value.

- RCV: Replacement Cost Value. This relates to the cost to restore the roof with covered materials and scope under the policy terms.

What matters in practice is understanding which payment stage you're in, what your carrier approved, and whether the written scope matches what the roof needs.

Where claims get off track

The biggest disconnect usually happens between the adjuster summary and the actual code-compliant work required on site. The paperwork may not fully reflect flashing needs, accessory replacement, steep charges, ventilation updates, or items discovered during tear-off.

That's why homeowners need a contractor who can document conditions clearly and communicate supplements when the approved scope falls short. This walkthrough of the storm damage insurance claim process gives a practical view of how that usually unfolds.

Keep every document. Scope sheet, estimate, photos, claim correspondence, mortgage notices if applicable, and any supplement approvals. Roof projects go smoother when the paperwork stays organized.

What helps the process go cleaner

A smoother insurance-backed roof replacement usually comes from process discipline, not luck.

- Report the claim promptly. Delays can create avoidable friction.

- Get a detailed roof inspection. You need jobsite reality, not guesswork.

- Compare scope to damage. Line items matter.

- Ask questions about exclusions. Don't assume every roof component is covered the same way.

- Review final payment timing. Some claims pay in stages.

Homeowners also need to know what not to do. Don't sign vague contingency paperwork you don't understand. Don't assume every contractor reads insurance scope the same way. And don't treat the adjuster summary as the final word if obvious code-required items are missing.

The cleanest claim is the one where everyone is working from the same roof, the same photos, and the same written scope.

Financing Your Roof and Managing the Project Budget

The budget conversation changes once you stop thinking of a roof as one painful check and start treating it like a controlled monthly obligation. For many homeowners, that's the difference between replacing the roof now and putting it off until the leak gets worse.

Most roofing articles don't spend enough time on this point. They give you a project total, then leave you alone with it.

Think of it as a rooftop mortgage

Most guides don't explain how to manage a $12,000 to $20,000 project through monthly payments. A more practical approach is treating the roof like a "rooftop mortgage" through contractor financing so you can install better materials now instead of delaying until failure forces the issue, as described in this roof budgeting framework for asphalt shingle projects.

That framing helps because it changes the decision from "Can I absorb this all at once?" to "What monthly payment fits my household without draining savings?"

What works better than waiting

Deferral is expensive in ways homeowners don't always price correctly. A roof leak rarely stays a roof leak. It can become drywall damage, insulation problems, staining, or interior disruption that lands at the worst possible time.

A financing plan can also let you make stronger long-term choices:

- Upgrade the shingle now instead of settling for the cheapest product.

- Bundle related exterior work while crews and materials are already mobilized.

- Preserve emergency cash for other home surprises.

If you're comparing payment paths, this guide to roof replacement financing options covers the kinds of structures many homeowners review before signing a contract.

Bundling projects can reduce friction

When a roof is already being replaced, it can be smart to evaluate gutters, siding touchups, exterior paint, or screen repairs at the same time. That doesn't mean bundling always saves money in every case, but it often reduces scheduling headaches and prevents repeated disruption around the house.

If resale is part of your timing, this Prime Gutterworks guide to ROI projects is a good planning resource for deciding which exterior upgrades belong in the same investment window.

Don't forget solar and detached components

If your home has solar panels, satellite equipment, or mounted accessories, reroof planning gets more complicated. The roof replacement itself may be straightforward, but coordinating detach-and-reset work takes scheduling and communication.

That doesn't automatically mean the project becomes unmanageable. It just means the budget should account for more than shingles. The smartest approach is to identify those items before contract signing so there aren't surprises when the crew is ready to tear off.

Homeowners usually feel more comfortable with roof financing when they also get a clear project calendar, not just a payment option. Cost stress drops when the scope and timing both make sense.

The biggest budgeting mistake is trying to solve a long-life exterior system with a short-term panic decision. A roof protects the house every day. It makes sense to pay for it in a way that matches how long you'll use it.

How to Get an Accurate Estimate from Hail King Professionals

A trustworthy roof estimate isn't the cheapest number and it isn't the longest proposal. It's the one that matches the actual roof, the existing code requirements, and the true condition of the house.

Start by looking for four basics:

- Local experience: Storm regions demand storm-specific judgment.

- Insurance and documentation: Paperwork accuracy matters when claims are involved.

- Transparent scope: The estimate should describe what is included and how hidden damage would be handled.

- Clear communication: If the contractor is vague before the sale, the project usually won't get clearer later.

What a serious inspection should include

An accurate estimate should come from an actual roof assessment, not a drive-by price. Good inspection workflows often include photo documentation, slope review, accessory review, and a written breakdown of recommended work. For homeowners interested in how modern aerial and visual documentation tools support better inspections, this overview of Dronedesk's roofing inspection platform is helpful context.

Hail King Professionals serves Dallas-Fort Worth and East Texas with free, same-day inspections, detailed proposals, financing pathways, and coordination for related exterior items such as gutters, siding, and solar panel detach-and-reset. For homeowners comparing contractors, that kind of scope transparency is what makes bids easier to evaluate.

What to ask before you sign

Ask the contractor to walk you through the estimate in plain language. Ask what happens if damaged decking is found. Ask who handles supplements on an insurance job. Ask how cleanup is managed and whether the proposal clearly identifies material choices and accessory work.

If a contractor gets irritated by those questions, keep looking. A roof replacement is too expensive to hand over on trust alone.

If you need a roof assessment in Dallas-Fort Worth or East Texas, Hail King Professionals offers same-day inspections, clear replacement scopes, and practical help with insurance and financing so you can make a decision with real numbers instead of guesswork.