Does Insurance Cover Hail Damage to Roof? a Texas Guide

Yes, homeowners insurance usually covers hail damage to a roof, but the payout often shrinks because of your deductible, your policy type, and the age of your roof. Hail is a big enough issue that U.S. insurers handle more than 500,000 hail-related property damage claims each year, and hail makes up 45.5% of all homeowners claims nationwide with an average cost of $11,695 per claim.

If you're in Dallas-Fort Worth or East Texas, you already know the drill. The storm blows through fast, the noise on the roof gets your attention, and then you start wondering whether you just took a minor hit or whether you're staring at a full insurance claim. That's the right question, because roof claims in Texas aren't usually denied because hail never happened. They get reduced because homeowners don't know what their policy says, what damage matters, or how to handle the inspection.

People often get tripped up. They assume "storm damage" automatically means "new roof." That's not how the insurance game works. In North Texas, the details decide everything.

Your Roof After the Storm What Insurance Actually Covers

A typical DFW storm night goes like this. The hail starts, your gutters sound like a drum line, and the next morning you see granules in the downspouts, a dinged metal vent, and maybe a water spot that wasn't there before. Your first thought is simple: is this covered?

Usually, yes. But "covered" doesn't mean "paid the way you expect."

The reason insurers look so hard at these claims is simple. Hail claims aren't rare edge cases. They're a huge part of the property insurance business. CAPE Analytics says insurers in the U.S. receive more than 500,000 hail-related property damage claims each year, and hail accounts for 45.5% of all homeowners claims nationwide at an average cost of $11,695 per claim in its analysis of hail risk for property insurers.

That scale matters for you because carriers have systems for this. Adjusters know what they're looking for. Their inspectors know the policy language. If you show up with weak documentation or no independent roof assessment, you lose your advantage before the claim even gets moving.

What usually gets covered

Standard homeowners coverage generally responds when hail causes sudden roof damage. That can mean repair or replacement costs tied to direct storm impact.

What matters is whether the roof suffered real loss, not whether the storm looked dramatic from your driveway.

- Shingle impacts: Bruising, cracking, or broken tabs can support a claim.

- Penetration points: Damaged flashing, vents, and roof accessories often matter because they can lead to leaks.

- Water entry: If hail damage creates an opening and water gets in, the roof issue gets more serious fast.

The storm itself doesn't win the claim. The proof does.

There's also the life disruption side of this that people forget. If the house becomes hard to live in while you're dealing with repairs, logistics can get messy fast. For practical planning beyond the roof itself, MCHA's guide on disaster recovery is a useful read for sorting out what comes next after a major property event.

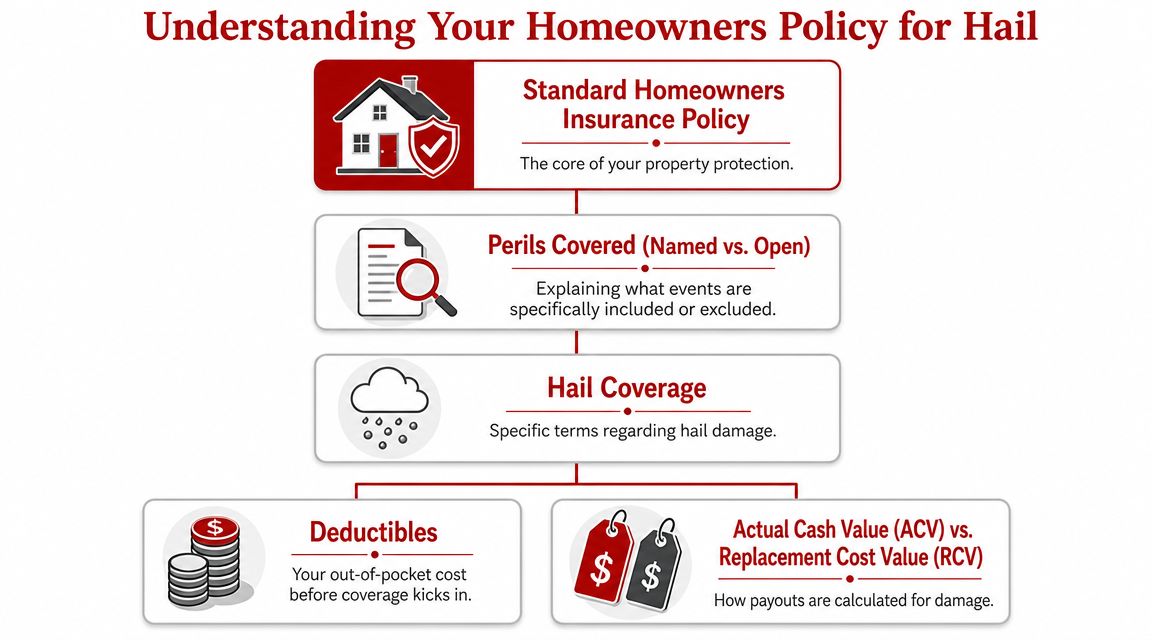

Understanding Your Homeowners Policy for Hail

Your policy is a contract, not a promise to buy you a brand-new roof every time ice hits shingles. Most standard homeowners policies cover hail damage to the roof under dwelling coverage because hail is treated as a covered peril, but payouts get reduced by the deductible and can be limited by cosmetic-damage exclusions or special hail deductibles in high-risk markets, as explained in Policygenius' review of roof hail coverage.

Covered peril doesn't mean unlimited payout

Think of hail coverage like collision coverage on a vehicle. If a specific event causes damage, the policy may respond. But the insurer still asks three questions:

- Did a covered event cause the damage?

- Is the damage functional or just cosmetic?

- How does the policy calculate payment?

That's why the answer to "does insurance cover hail damage to roof" is usually yes, but only after those questions get answered in the carrier's favor or yours.

Functional damage beats cosmetic damage

This is the distinction that matters most on real roofs in Texas.

Functional damage is damage that affects how the roof performs. Cracked shingles, punctures, broken seals, compromised flashing, and leak points fall in this bucket. This kind of damage is the core of a strong claim.

Cosmetic damage is damage the insurer can argue doesn't change performance. Dents on metal vents, marks on gutters, or surface marring that doesn't affect water shedding often trigger pushback.

Practical rule: If the damage changes how the roof protects the home, you've got a stronger insurance argument than if it only changes how the roof looks.

A lot of homeowners miss this and spend the whole inspection talking about dented gutters when the better evidence is on the roof slope, the ridge, the flashing, and any soft metals that help show impact direction and storm severity.

Read the storm language before you file

Before you call in a claim, review the parts of your policy that deal with wind and hail, cosmetic exclusions, and roof valuation. If you want a plain-English primer on broader storm damage coverage, this homeowners insurance and storm damage guide is a helpful starting point.

RCV vs ACV and Why Your Deductible Matters

Homeowners either protect themselves or get blindsided.

You can have a valid hail claim and still end up disappointed by the check. Why? Because coverage and payout are not the same thing. Many policies for older roofs pay actual cash value (ACV) instead of replacement cost value (RCV), and that changes the amount paid in a big way, as explained in Progressive's overview of hail damage and home insurance.

The simple version

RCV means the policy is built to pay what it costs to replace the damaged roof with a new one of similar kind and quality, subject to the deductible and policy terms.

ACV means the insurer subtracts depreciation first. Older roof, smaller payment.

If you want a non-insurance analogy, RCV buys the new version. ACV gives you the value of the used version you had before the storm.

RCV vs ACV side by side

| Feature | Replacement Cost Value (RCV) | Actual Cash Value (ACV) |

|---|---|---|

| How payment is calculated | Pays based on replacement cost, subject to policy terms | Pays depreciated value after age and wear are considered |

| Effect on older roofs | Usually more favorable to the homeowner | Usually less favorable to the homeowner |

| Out-of-pocket burden | Lower if the claim is approved and scoped correctly | Higher because depreciation reduces the check |

| Best way to think about it | New equivalent roof cost | Used roof value at time of loss |

Older roofs are where claims get ugly

A lot of East Texas and DFW homeowners don't realize their roof aged into a different claim outcome. They assume the same policy logic from years ago still applies. Sometimes it doesn't.

If your roof has age on it, read up on how insurers look at that issue. This guide for homeowners on aging roofs gives a useful outside perspective on why older roof claims often get tougher.

Deductibles are the second gut punch

In Texas, a standard flat deductible isn't always the number that matters. Wind and hail deductibles are often percentage-based. That means the amount you pay out of pocket is tied to the insured value of the home, not a small fixed line item you barely noticed at renewal.

This is why so many people think insurance is "covering the roof" and still feel shocked when the numbers come back. They focused on premium. They ignored deductible structure.

Here's the practical checklist I give homeowners before they file:

- Check the loss settlement language: Look for ACV or RCV wording tied specifically to the roof.

- Find the wind and hail deductible: Don't assume it's the same as your all-perils deductible.

- Review exclusions: Cosmetic damage language can limit what gets paid.

- Look at roof endorsements: Some policies have separate terms for older roofing systems.

If you don't know whether your roof is ACV or RCV before the adjuster shows up, you're negotiating blind.

Most claim frustration isn't about whether hail happened. It's about how the policy values the roof after the hail happened.

What Insurance Adjusters Look For During an Inspection

Adjusters don't show up to admire storm damage. They show up to decide whether they can connect visible roof conditions to a covered event under the terms of your policy.

That means they care about evidence, age, condition, and scope.

Roof age changes the conversation fast

A 2023 Oklahoma Insurance Department bulletin gives a practical example homeowners should pay attention to. When a roof reaches about 10 to 15 years old, hail damage may be paid on an Actual Cash Value basis instead of Replacement Cost Value. The same bulletin notes that a 2% deductible on a $250,000 coverage limit equals $5,000, which comes straight off the claim payout, as discussed in this insurance bulletin summary on hail-damaged roofs.

That's not Oklahoma-only logic. It reflects a real pattern homeowners see across hail-prone markets, including Texas.

What the adjuster is trying to sort out

An adjuster usually wants to answer these questions:

- Was the damage caused by this storm?

- Was the roof already worn out?

- Does the observed damage affect function?

- Is the amount of damage enough to justify repair or replacement under the policy?

If your shingles are brittle, curling, poorly ventilated, or visibly aged, the carrier may argue that hail wasn't the main problem. If the roof shows neglect, that gives the insurer more room to reduce the claim.

What helps your side

You don't need to argue like a lawyer. You need to present a clean, documented story.

A strong file usually includes:

- Storm timing: The date of loss needs to make sense and match weather activity.

- Maintenance history: Basic proof that the roof wasn't ignored helps.

- Visible impact markers: Granule loss, fractured shingles, vent hits, flashing issues, and leak evidence carry more weight than general complaints.

- Independent roof findings: A contractor who has already inspected the roof can point out what the adjuster might skip.

A rushed inspection creates bad paperwork. Bad paperwork leads to bad payouts.

In DFW, this is exactly why homeowners shouldn't wait for the adjuster to tell them what happened to their own roof.

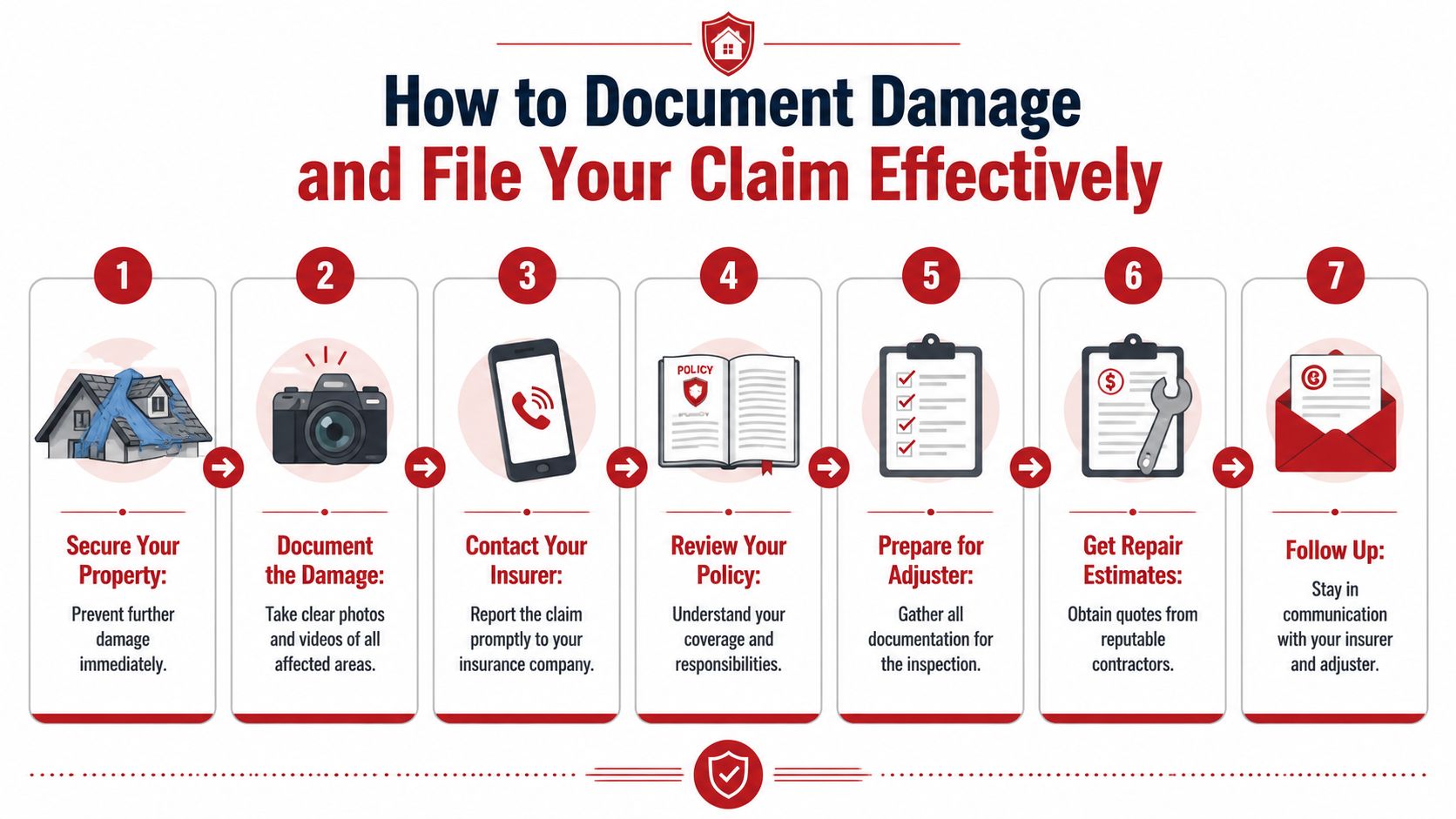

How to Document Damage and File Your Claim Effectively

Most bad hail claims start with bad sequencing. The homeowner calls insurance first, gets assigned an adjuster, and only then tries to figure out what was damaged. That's backwards.

The smart move is to secure the property, document the loss, and get an independent roofing inspection before the insurance inspection happens.

Insurers expect dated storm documentation, close-up and wide-angle photos, and a professional roof inspection to prove hail created direct loss rather than pre-existing wear. Contractor estimates also matter because they help establish scope and push back on underpayment, according to Malarkey Roofing's claims guidance for hail damage.

The order that works best

Stop active damage first

If water is getting in, tarp the affected area or take emergency mitigation steps. Insurance expects you to prevent additional damage where you reasonably can.Take broad exterior photos

Get each side of the house, rooflines visible from the ground, gutters, downspouts, fence lines, window screens, and any collateral hits. Wide shots help show the damage pattern across the property.Take detail shots

Photograph bruised shingles, displaced granules, metal vent strikes, flashing damage, interior stains, and anything else that changed after the storm. Keep the images dated and organized.

Before you move deeper into the claim process, this practical what to do after a hail storm checklist can help you keep the timeline straight.

A short visual walkthrough can also help if you haven't dealt with a storm claim before.

Why you should call a local roofer before the adjuster

This is the part I feel strongest about for North Texas homeowners. Call a local roofing contractor first.

Not because the contractor controls the claim. They don't. Call first because you need an independent set of trained eyes on the roof before the insurance company creates the first official damage narrative.

A local pro can help with:

- Identifying functional damage: The claim needs roof-performance evidence, not just surface dents.

- Creating a scope of loss: A written estimate helps frame what the adjuster should inspect.

- Attending the adjuster meeting: That keeps important damage from getting missed or mislabeled.

- Spotting local code issues: DFW and East Texas reroofs can involve code-related items that matter once work starts.

One option homeowners in this market use is Hail King Professionals, a DFW and East Texas roofing contractor that handles inspections and roof repair or replacement work tied to storm damage claims.

What to say when you file

Keep it factual. Don't speculate. Don't exaggerate.

Use plain language:

- State the date of loss

- Describe what you observed after the storm

- Mention any interior leaking or visible exterior damage

- Confirm that you've documented the property

- Ask about your deductible and roof valuation terms

Say what you know. Don't guess at what you can't see from the ground.

Common mistakes that hurt claims

- Waiting too long: Delay gives the carrier room to question causation.

- Skipping photos: If it isn't documented, it gets easier to dispute.

- Throwing away damaged materials: Keep anything removed during emergency mitigation if practical.

- Meeting the adjuster alone: If possible, have your contractor present.

- Accepting the first number without review: Compare the carrier scope against a contractor estimate.

Clean documentation won't guarantee a perfect result. But weak documentation almost guarantees a harder fight.

Navigating Hail Claims in North and East Texas

North and East Texas homeowners deal with a version of the insurance process that feels harsher because carriers write policies around repeated hail exposure. That's the local reality. The storm risk is familiar, so the policy language is tighter, the deductibles hit harder, and the inspections often feel less forgiving.

This is why generic national advice falls short here.

What makes this market different

In Dallas-Fort Worth and across East Texas, percentage deductibles are common enough that homeowners need to read the declarations page before storm season, not after. A lot of people discover their wind and hail deductible only when they're already stressed and trying to decide whether filing makes sense.

Local conditions also affect repair strategy. Roof pitch, ventilation setup, neighborhood code expectations, solar detach-and-reset issues, and matching concerns all shape how a claim turns into actual work. Someone who works these storm paths regularly will usually spot issues an out-of-area inspector might treat as secondary.

Why local representation matters at the inspection

When you meet the adjuster with no contractor present, you're relying on the insurer's version of the roof. That's risky in a hail-heavy market.

A local roofing contractor can help by:

- Walking each slope before the adjuster arrives

- Pointing out functional hits instead of chasing cosmetic distractions

- Flagging code-related items that affect repair scope

- Comparing the carrier scope to what the roof needs

If you're trying to understand how the local claim path typically unfolds from inspection to supplementing to final approval, this storm damage insurance claim process overview lays out the sequence in plain English.

North Texas claims aren't impossible. They're just technical. Homeowners who treat them casually usually leave money and repair quality on the table.

Protecting Your Home with the Right Partner

So, does insurance cover hail damage to roof systems in Texas? Usually yes. But that answer means very little until you know whether your policy pays ACV or RCV, how your wind and hail deductible works, how old your roof is, and whether you can prove functional damage from a specific storm.

That's why I don't recommend making your insurance company your first call after a hailstorm. Make your first call to a roofer who knows DFW and East Texas claims, can inspect the roof independently, and can help you walk into the adjuster meeting prepared. That one move changes the whole process. It gives you facts before opinions, documentation before disputes, and a scope before a settlement number shows up.

If you wait for the carrier to define the damage for you, you're already behind. If you start with an independent inspection, you have a shot at a fair claim and a roof that gets fixed the right way.

If your roof took hail in Dallas-Fort Worth or East Texas, contact Hail King Professionals for an independent inspection before you file or meet the adjuster. A local assessment can help you understand whether the damage is functional, what your paperwork needs to show, and what questions to ask before you commit to the insurance company's first version of the claim.