Roof Repair with Financing: Your 2026 Guide

A Texas storm usually doesn't hit at a convenient time. You hear hail on the roof in Arlington or Fort Worth, the rain passes, and then the serious stress begins. You notice water staining a ceiling, shingles in the yard, or a leak that wasn't there yesterday. The next question isn't just “How bad is it?” It's also “How am I supposed to pay for this right now?”

That's where roof repair with financing becomes practical. It isn't only for full replacements or major remodels. It helps when the roof needs attention now, but the insurance process is still moving, the deductible is sitting in front of you, or you don't want to deplete savings to stop a leak.

Texas homeowners deal with a few extra layers that generic finance articles miss. Hail claims can drag. Wind damage can look minor from the ground but turn into decking or flashing problems once the roof is opened up. More homes in places like Frisco, Plano, and Austin also have solar panels, which can change the scope of a reroof. If you don't line up the estimate, claim strategy, and financing plan in the right order, the project gets harder than it needs to be.

If you're sorting through claim paperwork at the same time, it also helps to understand how policy shopping and coverage comparisons work in other markets. A resource like find California home insurance quotes can be useful for seeing how homeowners think through coverage options and cost trade-offs, even though your roof decision here in Texas still needs a contractor-led inspection and a claim-specific plan.

Your Guide to Navigating an Urgent Roof Repair

When a roof starts leaking after a storm, most homeowners don't need a lecture. They need a clear path.

In Dallas, Garland, Mesquite, and Tyler, the pattern is usually the same. The storm passes, the damage looks manageable from the driveway, and then the inside of the house tells a different story. A ceiling stain spreads. Drip pans come out. Someone gets online and searches for roof repair near me, then realizes the hard part isn't just finding a contractor. It's making a decision fast enough to protect the house without making the wrong financial move.

A damaged roof rarely waits for a convenient month in your budget.

Roof financing works best when you treat it as a timing tool. It gives you room to move on urgent repairs while preserving cash for your deductible, interior repairs, or the next surprise that often follows a severe Texas storm. That matters even more when insurance is involved, because claim timelines and actual roof conditions don't always line up.

What urgency really looks like after a Texas storm

A roof can be compromised without looking dramatic from the street. Hail can bruise shingles. Wind can break seals. Heavy rain can find openings around flashing, vents, or valleys. On older systems, one storm can expose weaknesses that were already close to failing.

For homeowners, that creates three immediate concerns:

- Protecting the home: Active leaks can affect insulation, drywall, and framing.

- Preserving claim support: Early documentation helps if insurance is part of the plan.

- Keeping options open: Financing can bridge the gap while you sort out scope and payment responsibility.

What usually works and what usually doesn't

Some approaches solve problems quickly. Others create a second round of stress.

| Approach | What tends to happen |

|---|---|

| Get the roof inspected first | You get a real scope, not a guess |

| Wait too long to address leaks | Water intrusion often spreads beyond the roof covering |

| Use financing after scope is clear | The payment plan matches the actual job better |

| Pick a loan before the roof is verified | You risk coming up short when hidden damage appears |

Homeowners usually feel better once the process is broken into order: inspect, document, estimate, compare funding, then schedule work. That order matters more than the specific financing product you choose.

Start with a Professional Roof Inspection and Estimate

Before you compare loans, payment plans, or monthly payments, get the roof inspected by a professional. This is the step that keeps the whole project grounded in facts.

A quick driveway quote isn't enough after hail, wind, or heavy rain. A proper inspection looks at the visible roof surface and the parts that often cause trouble after Texas storms, including flashing details, ventilation areas, and signs that moisture may have reached underlying components. If the roof has aged shingles, prior repairs, or impact points from hail, the estimate needs to account for that.

NerdWallet reports that the average homeowner pays about $9,500 for a roof replacement, and that cost can exceed $45,000 when premium materials are used, which is why financing has become a practical tool for many homeowners handling roof work (NerdWallet roof financing guidance).

What a useful estimate should include

A real estimate should do more than name a price. It should help you and the lender understand the project.

Look for these basics:

- Defined scope of work: Repair versus replacement, affected roof areas, and whether related components are included.

- Material details: Shingle type, underlayment, flashing items, and any upgrades being proposed.

- Known storm issues: Hail hits, lifted shingles, leak entry points, and visible wear.

- Possible hidden conditions: Notes about what may only be confirmed after tear-off.

- Payment structure: Deposit terms, insurance coordination if applicable, and financing compatibility.

If you want a starting point before an on-site visit, an Online roofing estimate tool can help you think through project inputs and prepare better questions. It shouldn't replace an inspection, but it can help you organize the conversation.

Why this step protects your financing decision

The biggest mistake I see is homeowners trying to solve the money question before they've solved the scope question. That feels efficient in the moment, but it often creates trouble later. If the roof is opened up and the crew finds additional work that should have been part of the original project, the budget can shift.

Practical rule: Don't finance a guess. Finance a verified scope with room for normal roofing surprises.

This matters in places like McKinney, Longview, and San Marcos where storm damage can combine with older roof age. A professional inspection gives you a number you can use for a claim discussion, a financing application, and a work schedule. Without that, everything else is built on assumptions.

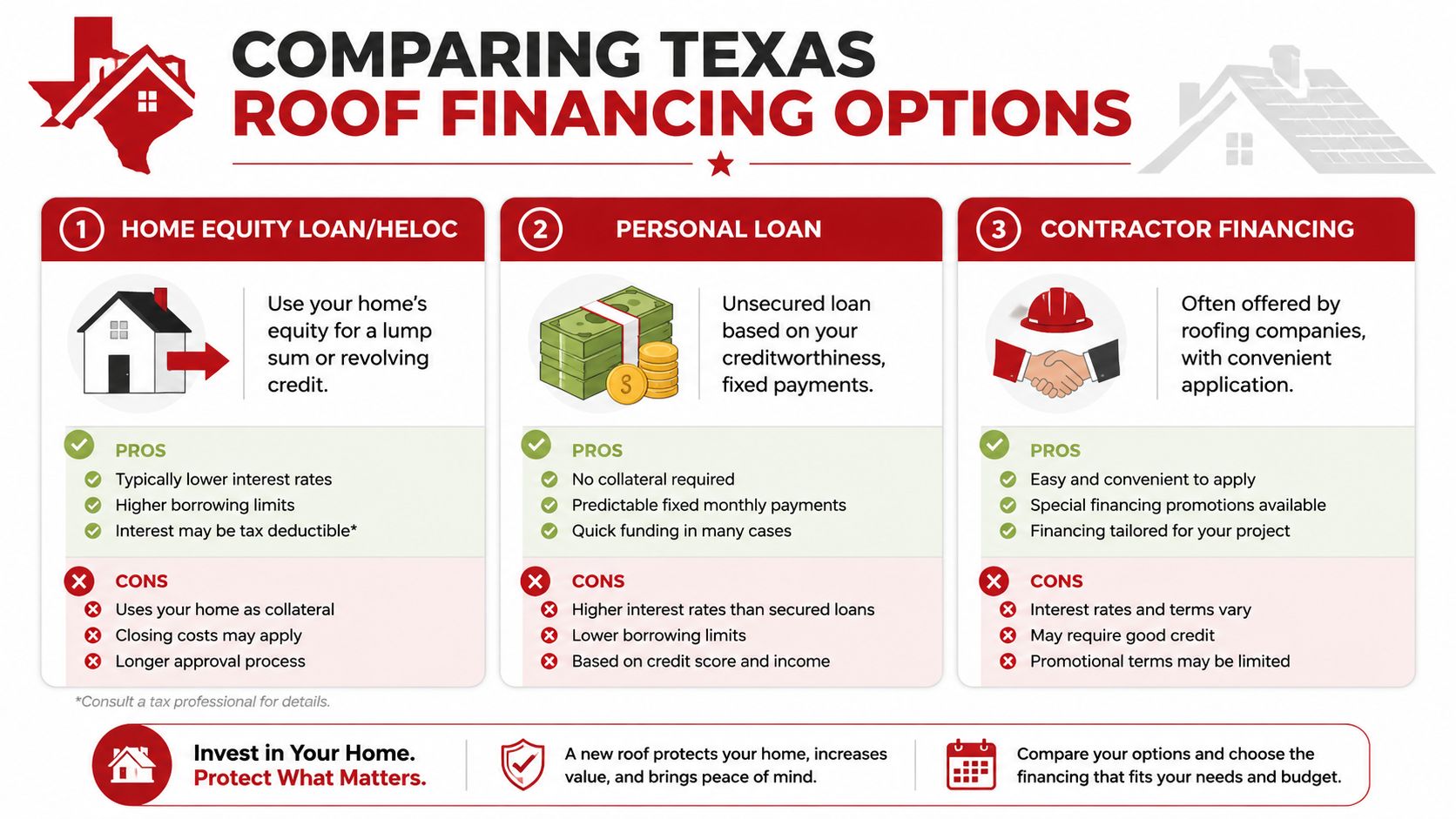

Comparing Your Roof Financing Options in Texas

A common Texas storm scenario goes like this. The adjuster is scheduled, a tarp is already on the roof, and the homeowner needs to decide whether to wait for insurance funds or approve work now and cover the gap with financing. That choice gets more complicated if the roof has solar panels, code-related upgrades, or damage that may not be fully paid the first time through the claim.

In practice, the right option depends on two things. How fast the roof work needs to start, and whether insurance is paying all, part, or none of the bill. Texas hail claims often leave homeowners bridging a deductible, paying for upgrades insurance will not cover, or handling solar detach and reset work that needs careful scheduling.

How the common options stack up

| Option | Usually works best for | Main trade-off |

|---|---|---|

| Personal loan | Storm-driven repairs or replacements that need quick approval | Borrowing cost is often higher than equity-based products |

| Home equity loan or HELOC | Larger planned projects with time for lender review | Approval can take longer, and the loan is tied to the home |

| Contractor financing | Roofing projects where timing, scope, and install coordination need to stay aligned | Terms vary by lender partner, so you still need to compare offers |

| Credit card | Small repairs, emergency dry-in work, or a very short-term gap | Carrying the balance can get expensive fast |

Government-backed renovation loans can also come up, especially if the roof issue is part of a larger home rehab. Those products usually make more sense for planned renovations than post-storm urgency because contractor approval, lender review, and closing timelines can slow the job.

A video overview can also help if you're deciding which path feels most practical for your situation.

Personal loans for urgent roof work

Personal loans are often the cleanest fit when the claim is still being worked out and the roof cannot sit exposed. I recommend homeowners look at this option when speed matters more than getting the lowest possible rate.

They usually work well in situations like these:

- Insurance is coming, but not yet: You need to start the roof and expect claim funds later.

- The deductible and upgrades create a gap: The claim may cover the base scope, but not everything you want done.

- Solar or accessory work adds cost: Detach and reset, upgraded flashing, or added ventilation may fall outside the carrier's payment.

- You want fixed payments: A set monthly amount is easier to plan around while the rest of the property is still being repaired.

Home equity loans and HELOCs for larger scopes

Home equity products can be a reasonable choice if the roof project is part of a bigger property plan and there is time to wait on underwriting. They are often considered by homeowners who are not dealing with an active leak and want to spread out a larger cost at a lower borrowing rate than many unsecured options.

The trade-off is timing. After a hail event in DFW or East Texas, lenders do not speed up just because the ridge got hit or the flashing around the chimney is letting in water. If your insurance carrier is also reviewing supplements, code items, or solar-related line items, a slower loan process can create another delay.

If you're trying to understand how a second-position borrowing structure works in plain language, EHF Mortgages second charge advice offers a useful explanation of the concept.

Contractor financing for roofing-specific projects

Contractor financing often works well because the funding path is tied directly to the roofing schedule. That matters when the claim, material order, permit timing, and installation window all have to line up.

At Hail King Professionals, contractor financing is available with soft credit checks, no prepayment penalties, and no home-equity requirement. For a Texas homeowner, the practical advantage is simple. You can approve the roof work, keep the claim process moving, and avoid opening a separate equity loan just to cover timing gaps or non-covered items.

For a broader look at lender-backed and contractor-based payment paths, review these roof replacement financing options.

This option is especially useful on roofs with solar panels. Panel removal and reinstallation has to be coordinated with the roofing schedule, and delays between trades can leave the project sitting longer than it should.

When credit cards are the wrong tool

Credit cards have a place. Small service calls, emergency patching, or a deductible you can clear quickly are common examples.

They are usually a poor fit for a full replacement or a major storm restoration. I have seen homeowners put a roof deposit on a card while waiting on insurance, then end up carrying that balance longer than expected because supplements, depreciation release, or solar scheduling took more time than anyone wanted. The roof got fixed, but the payment method created a second problem.

The better choice is the one that fits the claim timeline, the roof scope, and your actual cash flow. In Texas, that usually matters more than chasing the lowest advertised payment.

Decoding Financing Terms and Avoiding Pitfalls

A financing offer can look simple on the surface and still cost more than you expected. The numbers that matter most are usually not the ones in the biggest font.

The terms that actually matter

APR is the clearest starting point. It gives you a fuller picture of borrowing cost than the interest rate alone. If two offers have similar monthly payments but one has a meaningfully higher APR, that's a sign to slow down and read the details.

Loan term means how long you'll be paying. A longer term can lower the monthly payment, which helps cash flow. It can also increase the total amount you pay over time. That doesn't make a longer term bad. It just means you should choose it on purpose.

Fees deserve attention. Some products include charges that don't feel obvious during the sales conversation. If a lender or financing partner can't explain the fee structure clearly, keep looking.

A simple way to compare offers

When homeowners compare roof repair with financing options, I recommend using three questions:

- What is the monthly payment? This tells you whether it fits your real budget.

- What is the total borrowing cost? This keeps a low payment from hiding an expensive loan.

- Can you pay early without a penalty? Flexibility matters if insurance funds arrive later or your budget changes.

Watch for this: A low monthly payment can be perfectly fine, but it shouldn't distract you from the total cost and the repayment timeline.

If you're dealing with storm damage, this matters even more because insurance can change the timing. Some homeowners finance the work immediately, then want to pay down the balance once claim funds are finalized. That's much easier when there's no prepayment penalty.

Pitfalls that show up on roofing jobs

Roof projects have a few financing traps that are different from other home improvements.

One is borrowing too little because the estimate was rushed. Another is locking into a product before you understand how insurance will interact with the final cost. A third is focusing only on approval speed and skipping the contract review.

A safer approach looks like this:

- Confirm the scope first so the financed amount reflects the actual job.

- Review how funds are disbursed so you know whether money goes to you, the contractor, or in stages.

- Ask about early payoff if insurance reimbursement or reserve funds may reduce the balance later.

- Read the promotional terms carefully so deferred payments don't become an unpleasant surprise.

Most financing problems on roofing jobs aren't caused by complicated math. They come from decisions made too early, with incomplete information.

The Financing Application and Approval Process

The application process feels a lot easier when you know what lenders are looking for and what order to handle things in. For most homeowners, the cleanest path is to prepare documents, review pre-qualification, then move into a full application only after the roof scope is settled.

What to gather before you apply

Roofing finance applications usually move faster when the paperwork is ready up front. Premier Roofing notes that contractor-led financing or third-party loan programs commonly require items such as proof of income, identification, and sometimes an appraisal before funds are released, and it recommends soft-pull pre-approval before a full application because the formal application can trigger a hard credit inquiry (Premier Roofing roof financing process).

Have these ready:

- Identification: Government-issued ID and basic personal information.

- Income documentation: Pay stubs or other proof of income that supports repayment ability.

- Project estimate: The contractor's written scope and cost breakdown.

- Property information: Basic address and ownership details.

- Insurance paperwork if relevant: Especially if claim proceeds may offset part of the project.

Soft pull first, full application second

A soft-pull pre-approval is useful because it lets you check whether a product is likely to fit without jumping straight into the full credit process. That doesn't replace final approval, but it gives you a cleaner decision path.

Once you move to a formal application, the lender may perform a hard inquiry. That's normal. What matters is not doing that too early, before the project amount is well established.

Get the estimate right before you let the lender finalize the file.

Why scope changes cause financing trouble

A common pitfall is choosing a financing product before the repair scope is verified. Roof projects often reveal hidden deck or flashing issues after tear-off, which can force a change order or require a second loan if the initial amount is insufficient.

That's not rare in Texas. Hail damage, previous patchwork, and moisture around penetrations can all stay hidden until the old material comes off. If the original financed amount is too tight, the project can stall at the worst possible time.

A cleaner approval sequence

The strongest application process usually follows this order:

- Inspection and written estimate

- Reserve for possible hidden conditions

- Soft-pull pre-qualification

- Full application

- Final approval and scheduling

In places like Garland, Mesquite, and Marshall, where storm damage often combines with aging roofs, this order keeps the project from getting sideways after materials are already off the house.

Coordinating Your Financed Roof Project

Once the loan is approved, the key work is keeping the money, the claim, and the build schedule lined up. After a Texas hail storm, those pieces can drift fast. Insurance may be slow to release funds, materials can move in price, and a roof with solar panels adds another trade partner to the calendar.

The financed projects that stay on track usually have one thing in common. The approved loan amount matches the actual scope of work, including items homeowners often miss at first, such as code upgrades, decking repairs, and detach-and-reset work for solar if the array sits over damaged slopes. If those costs are left out, the financing may be approved on paper and still come up short in the field.

Keep the insurance claim and project scope tied together

In storm areas like DFW and East Texas, financing often fills a timing gap rather than replacing insurance. A homeowner may have an open claim, a checked and tarped roof, and no desire to wait weeks for paperwork while another storm rolls through.

That creates a few common job setups:

- Claim approved, payment still pending: Financing can keep the roof moving before insurance funds arrive.

- Insurance scope is too narrow: Financing can cover items the carrier did not include but the roof still needs to perform properly.

- Deductible or out-of-pocket gap: Some homeowners finance only that portion so cash stays available for interior water damage, fencing, or other storm repairs.

The trade-off is simple. Starting too early without claim clarity can create paperwork friction. Waiting too long can turn a repair into interior damage.

Solar changes scheduling and budget

Solar roofs need tighter coordination. If panels must come off before tear-off and go back on after install, that should be priced and scheduled before the first shingle is ordered. We see this missed more often than homeowners expect, especially in North Texas neighborhoods where newer solar systems sit on aging roofs that have already taken hail.

A good contractor will confirm who handles detach-and-reset, whether the solar company has availability, and how that affects the financed amount. If that answer is vague, the project is not ready to schedule.

What to confirm before work starts

Before installation day, get these items settled in writing:

- Final scope: Roofing, flashing, ventilation, decking repairs, gutters if included, and solar coordination if needed

- Payment timing: When lender funds are released, what insurance has paid, and what portion remains your responsibility

- Material selection: Shingle type, color, underlayment, and any upgrades tied to insurance or code

- Schedule: Delivery date, tear-off date, expected completion window, and who updates you if weather shifts the plan

- Closeout process: Final walkthrough, photo documentation, and how punch-list items are handled

If you are still comparing companies, review this guide on how to choose a roofing contractor before signing anything.

Roof financing should support the repair schedule, not create delays because the job scope was incomplete.

From a project management standpoint, the cleanest jobs are the ones where everyone is working from the same scope. Homeowner, contractor, lender, adjuster, and solar provider if the house has panels. That is how a financed roof project stays manageable, even during a busy Texas storm season.

DFW and East Texas Roof Financing FAQs

Can I finance just my insurance deductible in Texas

Yes, in many cases homeowners use financing for only part of the project cost rather than the full roof amount. That can make sense when insurance is covering a large share of storm damage but you want to spread out the deductible or preserve savings for interior repairs and related costs.

What if insurance only approved a partial repair but the roof really needs more

That happens. The key is making sure the roof scope is documented clearly from the start. If the approved insurance amount doesn't match the full repair need, financing can be used to cover the gap so the roof is repaired correctly rather than patched in a way that leaves future problems behind.

Is roof repair with financing only for full replacements

No. It can be used for targeted repairs, leak correction, storm-related sections, or full replacement work. The right product usually depends on project size, urgency, and whether insurance is part of the picture.

Do solar panels affect financing for a roof project

They can. If your roof requires detach-and-reset coordination, that should be included in the project scope before financing is finalized. If it's left out, the budget can come up short.

Should I wait for claim money before starting the roof

That depends on leak risk, claim timing, and the roof's current condition. If active water intrusion is present, waiting can create more damage inside the home. In many Texas storm cases, financing is used as a bridge so the home is protected while the insurance side catches up.

What should I ask before signing a financing agreement

Ask about the APR, term length, total cost, early payoff rules, how funds are released, and what happens if the scope changes after tear-off. Also confirm that the estimate reflects the actual project, not a rough placeholder.

Does the contractor choice matter if I already have financing lined up

Absolutely. Financing doesn't fix poor project management. You still need a contractor who documents storm damage well, communicates clearly, and can coordinate the work without letting scope, materials, and payment timing get out of sync.

If your roof took hail or wind damage in Dallas, Fort Worth, Arlington, Plano, Tyler, Longview, or nearby Texas communities, Hail King Professionals can help you sort out the inspection, estimate, claim coordination, and financing path in the right order so you can protect the home without guessing.