Roof Damage Insurance Coverage: A Texas Homeowner’s Guide

The storm has moved on, but your nerves probably haven't. You hear dripping in the attic, notice shingles in the yard, or spot dents on the metal vents after a hard Texas hailstorm. Then the questions start fast. Is this covered? Should you call insurance first? Should you get a roofer out before anyone else? What if the damage looks minor now but turns into a leak later?

That uncertainty is normal. Roof damage insurance coverage can feel confusing because the roof is visible, but the policy language usually turns on a less visible issue, the cause of the damage, the age of the roof, and the timing of your claim.

Texas property owners deal with this every storm season. In U.S. homeowners insurance, wind and hail are the single largest source of property claims, and during the 2019 to 2023 period, about 1 in 36 insured homes had a wind-or-hail loss each year, according to the Insurance Information Institute's homeowners insurance facts. That matters because roof insurance is usually built around sudden storm events, not old age or deferred maintenance.

After the Storm Navigating Your First Steps

A homeowner in Arlington might walk outside after a night storm and see nothing dramatic from the driveway. No tree through the roof. No giant hole. But up close, the signs can be easy to miss. Granules washed into the gutter. Creased shingles along the ridge. A chimney cap bent by wind. A water stain that wasn't there yesterday.

That first hour matters because decisions made right after the storm can help or hurt a claim later.

Start with safety and a ground-level check

Don't climb onto the roof right after hail, heavy rain, or high wind. Wet shingles, slick metal panels, and hidden soft spots can turn a simple inspection into an injury.

From the ground, look for:

- Shingles in the yard: Loose or missing pieces often point to wind lift.

- Fresh dents on metal items: Check roof vents, gutters, downspouts, and mailbox tops for hail impact clues.

- Debris around the home: Broken branches can indicate impact or wind pressure on the roof.

- Interior warning signs: New ceiling stains, damp insulation, or a musty attic smell can signal active water entry.

If you want a visual idea of what inspectors look for after severe weather, this overview of a storm damage roof inspection is a useful reference.

Don't assume “no leak” means “no claim”

A lot of homeowners wait because they think insurance only applies once water starts pouring inside. That's one of the most common misunderstandings. Storm damage can weaken shingles, flashing, ridge caps, vents, and fasteners before an interior leak shows up.

Practical rule: Treat a major hailstorm or wind event as a reason to inspect, not a reason to wait.

A prompt inspection helps you separate recent storm damage from older wear. That distinction becomes important when an adjuster reviews the claim.

For a more detailed local walkthrough on what to do after severe weather, this guide on roof inspection after storm damage is worth reading.

What Your Homeowners Policy Actually Covers

Most homeowners think the question is, “Is roof damage covered?” Insurance usually asks a different question. What caused the roof damage?

That's the heart of roof damage insurance coverage. Under standard homeowners policies, roof damage is typically covered only when it results from a covered peril such as wind, hail, or fire, while insurers generally exclude damage from normal wear and tear, aging, or poor maintenance, as explained in Liberty Mutual's guide to roofs and home insurance.

Covered peril versus excluded condition

A simple way to think about it is this:

| Situation | How insurers usually view it |

|---|---|

| Hail cracks shingles during a thunderstorm in Plano | Often treated as a covered peril |

| Wind lifts shingles off during a storm in San Antonio | Often treated as a covered peril |

| Texas heat dries and ages shingles over time | Usually treated as wear and tear |

| An old leak gets worse because flashing was never repaired | Usually treated as maintenance-related |

| Floodwater damages the roof system from below | Often excluded under standard homeowners coverage |

The same roof can produce two very different claim outcomes depending on the cause. If a storm caused sudden damage, the claim may fit the policy. If the roof reached the end of its life, the insurer may deny payment even if the damage now looks serious.

The roof is usually part of the dwelling

Another point that confuses people is where the roof sits in the policy. In most cases, the roof is part of your home's main structure, often handled under dwelling coverage rather than as a separate roof-only benefit. That means the claim is usually tied to your policy limits and deductible for the house itself.

A damaged roof doesn't automatically create coverage. A covered cause of loss does.

Common examples homeowners mix up

People often bundle all roof problems together, but insurers usually split them apart:

- Storm-created damage: Wind-torn shingles, hail bruising, impact from a falling limb.

- Age-related decline: Brittle shingles, granule loss from years of sun exposure, general deterioration.

- Maintenance issues: Failed sealant, neglected flashing, known leaks left unaddressed.

If you want another consumer-friendly explanation of how roof claims usually work, this homeowner's guide to roof insurance gives a helpful overview.

Decoding Your Policy Financial Terms

The hardest part of a roof claim often isn't proving there was damage. It's understanding why two homeowners with similar storm damage can receive very different payouts.

Three terms drive most of that confusion: deductible, replacement cost value, and actual cash value.

Deductible means your share first

Your deductible is the amount you pay out of pocket before insurance starts paying its portion of a covered loss. Homeowners sometimes think the deductible is a vague adjustment somewhere in the paperwork. It isn't. It's your direct financial responsibility on the claim.

If your roof damage is covered, your carrier still subtracts the deductible according to the policy terms. That's why it helps to review your declarations page before a storm season instead of during a stressful claim.

RCV and ACV are not the same thing

Replacement Cost Value (RCV) generally means the policy pays based on the cost to replace damaged materials with new materials of similar kind and quality, subject to policy terms.

Actual Cash Value (ACV) generally means depreciation gets deducted. In plain language, the insurer values the damaged roof as an older roof, not a brand-new one.

Consider a vehicle. If someone totals a used truck, the insurer doesn't usually hand over the price of a new one on the lot. Roofs can work the same way under ACV settlement.

Why roof age matters so much now

A major shift in the market is the growing use of ACV for older roofs. Some insurers deny full replacement-cost protection once a roof is over 15 years old, and one consumer guide notes the difference between ACV and RCV can be $10,000 to $15,000 on an older home, as explained in this article on roof insurance payouts and older roofs.

That's why two questions matter before you file:

- How old is the roof?

- Does the policy settle roof losses on RCV or ACV?

If your roof is older, the claim may still be covered for hail or wind. But the payout math may change sharply.

Older roofs often create the biggest surprise in roof damage insurance coverage. The dispute isn't always about whether damage exists. It's about how the policy values that damage.

A quick comparison

| Term | What it usually means for you |

|---|---|

| Deductible | You pay this amount first |

| RCV | Coverage is based on replacement with new, similar materials |

| ACV | Coverage is reduced for age and depreciation |

If you're dealing specifically with a storm event, this related guide on whether insurance covers hail damage to a roof can help you connect policy language to real hail-loss scenarios.

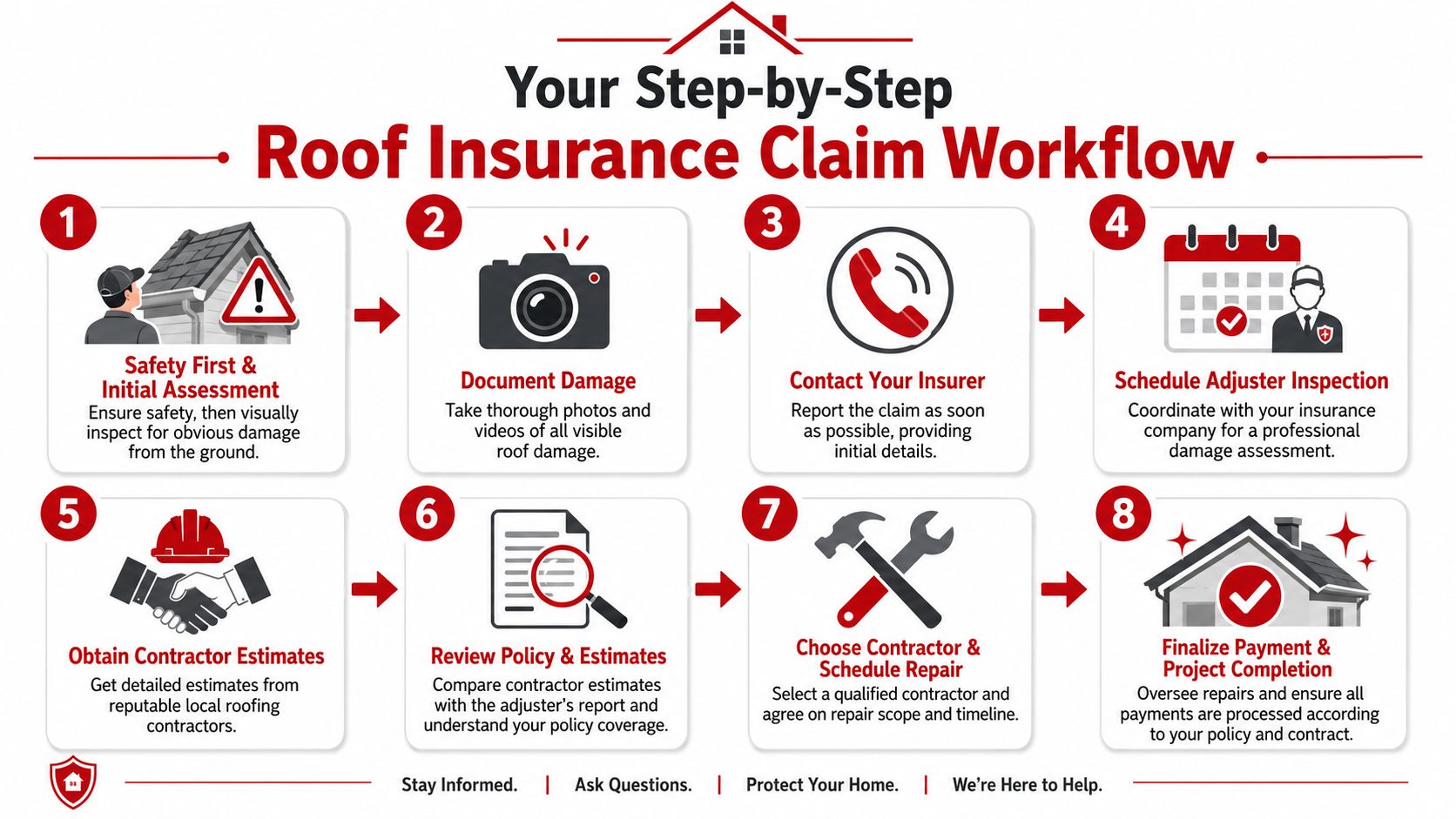

The Step by Step Roof Insurance Claim Workflow

A roof claim goes smoother when you treat it like a process, not a panic reaction. The order matters. The paperwork matters. The timing matters.

This visual gives a quick overview before the details.

Safety first, then protect the property

If a storm has opened the roof, your first responsibility is to prevent additional damage if it's safe to do so. That might mean moving belongings away from an active leak, placing containers under drips, or arranging temporary tarping.

Don't throw damaged materials away too quickly if they help show what happened. And don't make permanent repairs before the insurer has a fair chance to inspect, unless emergency conditions require immediate action.

Document before things change

Take clear photos and video from safe locations. Get wide shots and close-ups. Capture:

- Roof-related exterior signs: Missing shingles, bent flashing, dented vents, displaced ridge caps.

- Interior evidence: Ceiling stains, bubbling paint, wet insulation, attic moisture.

- Storm context: Fallen limbs, scattered debris, fence or gutter damage that supports a wind or hail event.

Write down the date you noticed the problem and what happened around that time. Details fade faster than people expect.

Report the claim promptly

Many policies require roof damage to be reported quickly, and delays can jeopardize coverage because the insurer needs to evaluate whether the loss was sudden and accidental rather than the result of wear or gradual deterioration, according to this guide on insurance claims for roof damage.

That doesn't mean you need every answer before calling. It means you shouldn't sit on obvious storm damage for too long while hoping it resolves itself.

Report early, document carefully, and keep copies of every email, photo, and claim note.

Prepare for the adjuster inspection

Once the claim is opened, the insurer will usually schedule an inspection. Before that visit:

- Gather your storm photos.

- Note every area of concern, inside and outside.

- Keep records of temporary mitigation work.

- Have any prior roof records available, if you have them.

A lot of frustration happens here because homeowners assume the adjuster will automatically spot every issue. Sometimes they do. Sometimes they don't. Visibility, weather, roof access, and even surface type can affect what gets noted.

To compare your own experience with a broader claim sequence, these Eagle Restoration's claims process insights offer a practical outside perspective.

A short video can also help make the workflow easier to picture:

Review the scope of loss, not just the check amount

After inspection, the insurer usually issues paperwork that describes what they believe was damaged and what they're paying for. This document matters more than many people realize.

Look closely at:

- Line items: Are vents, flashing, underlayment, ridge materials, starter shingles, and disposal included where appropriate?

- Measurements: Does the quantity appear to match the roof?

- Settlement basis: Is the claim valued on ACV or RCV?

- Code-related items: Are required components reflected if local requirements apply?

The first insurance number isn't always the final word. The written scope is what tells you whether the claim was evaluated fully.

Choosing a Contractor and Understanding Estimates

After a major storm, neighborhoods from McKinney to Tyler often see a wave of trucks, door knockers, and “today only” promises. Some contractors are legitimate. Some are not. The difference matters because your contractor's estimate often becomes the document used to compare against the insurer's scope.

Convective storm damage, including hail, reached $60 billion in 2023, according to the National Insurance Crime Bureau's report on rising roof claims. As losses rise, claims scrutiny tends to rise with them. That makes contractor accuracy and documentation more important.

What a solid contractor should provide

A reliable roofing contractor should be able to explain the estimate in plain language, line by line if needed.

Look for:

- Local presence: A contractor working regularly in Dallas, Fort Worth, Plano, or Longview is easier to reach after the job.

- Proof of insurance: You want a contractor who protects both their crew and your property.

- Detailed scope: The estimate should identify materials, labor, tear-off, disposal, and accessory items.

- Storm claim familiarity: Roof insurance paperwork has its own language. Experience helps.

Estimate versus scope of loss

A contractor's estimate and the insurer's scope of loss are related, but they are not the same document.

| Document | Who prepares it | What it does |

|---|---|---|

| Contractor estimate | Roofing contractor | Prices the work needed to repair or replace the roof properly |

| Scope of loss | Insurance carrier or adjuster | Lists what the insurer believes is covered and payable |

If the contractor estimate is higher, that doesn't automatically mean someone is acting in bad faith. The contractor may be including items the adjuster missed, code-required components, or materials needed to complete the roof system correctly.

A low number isn't always a better number. A complete number is better.

Storm chaser warning signs

Be cautious if someone:

- Demands immediate signature: Pressure is a red flag.

- Promises to “eat” your deductible: That kind of pitch can create problems.

- Avoids written detail: Vague paperwork leads to disputes later.

- Has no local track record: You need someone who'll still be reachable if warranty issues come up.

Navigating Claim Disputes and Supplements

A claim doesn't always stall because the insurer denied everything. More often, the first scope leaves something out. That's where a supplement comes in.

A supplement is a request to revise the claim amount based on additional support. Maybe the adjuster missed flashing, steep-charge items, starter materials, or code-related components. Maybe hidden damage only became visible after tear-off began. In those cases, the next step is usually documentation, not argument.

What makes a supplement stronger

The best supplement packages are specific. They usually rely on:

- Photos tied to the disputed item

- A revised contractor estimate

- Clear explanation of why the item is necessary

- Supporting code or manufacturer requirement, when relevant

Homeowners often find themselves overwhelmed. They know the insurance number looks short, but they don't know how to translate that concern into claim language the carrier can review.

When the issue is coverage, not price

Some disputes involve scope. Others involve the policy itself. Examples include older roofs limited to ACV, cosmetic-damage questions on metal roofing, or disagreement over whether the condition came from storm impact or age.

If the insurer says damage is cosmetic only, ask for clarity on what functional damage they did or did not identify. If they say wear and tear, compare that reasoning to the timing, storm evidence, and inspection findings.

Good dispute handling is orderly. Photos, notes, policy language, and line-item support carry more weight than frustration.

If a supplement doesn't resolve the issue, homeowners may need to ask about internal review or a formal appeal path under their policy. The key is to stay organized and keep every communication in writing.

Frequently Asked Questions About Roof Insurance

Can I choose my own roofing contractor

Usually, yes. The insurance company may provide guidance, but homeowners generally choose who performs the work on their property.

If my roof isn't leaking, should I still get it checked

Yes. Storm damage can exist before an interior leak appears. Hail bruising, lifted shingles, damaged flashing, and dented vents may not show inside right away.

Does homeowners insurance cover an old roof

Sometimes, but the age of the roof can affect how the claim is paid. Older roofs are more likely to face ACV settlement or other restrictions, depending on the policy.

Is a dented metal roof covered

It depends on the policy language and the nature of the damage. Some policies limit or exclude cosmetic damage, which can become an issue when hail affects appearance more than function.

Should I call a contractor or insurance company first

Either can be reasonable, but don't wait too long. A prompt inspection helps document conditions, and prompt notice to the insurer helps preserve the claim.

What should I keep after a storm

Keep photos, videos, receipts for emergency mitigation, claim emails, inspection notes, and copies of every estimate or insurance document tied to the loss.

If you're dealing with hail damage, wind-lifted shingles, or an insurance claim that feels harder than it should, Hail King Professionals can help you move from confusion to a clear plan. Homeowners across Dallas, Fort Worth, Arlington, Plano, Frisco, McKinney, Garland, Irving, Mesquite, Tyler, Longview, Marshall, San Antonio, Austin, New Braunfels, San Marcos, Boerne, Round Rock, and Georgetown can reach out for a professional roof inspection, straightforward damage assessment, and guidance on what your roof needs to be restored properly.